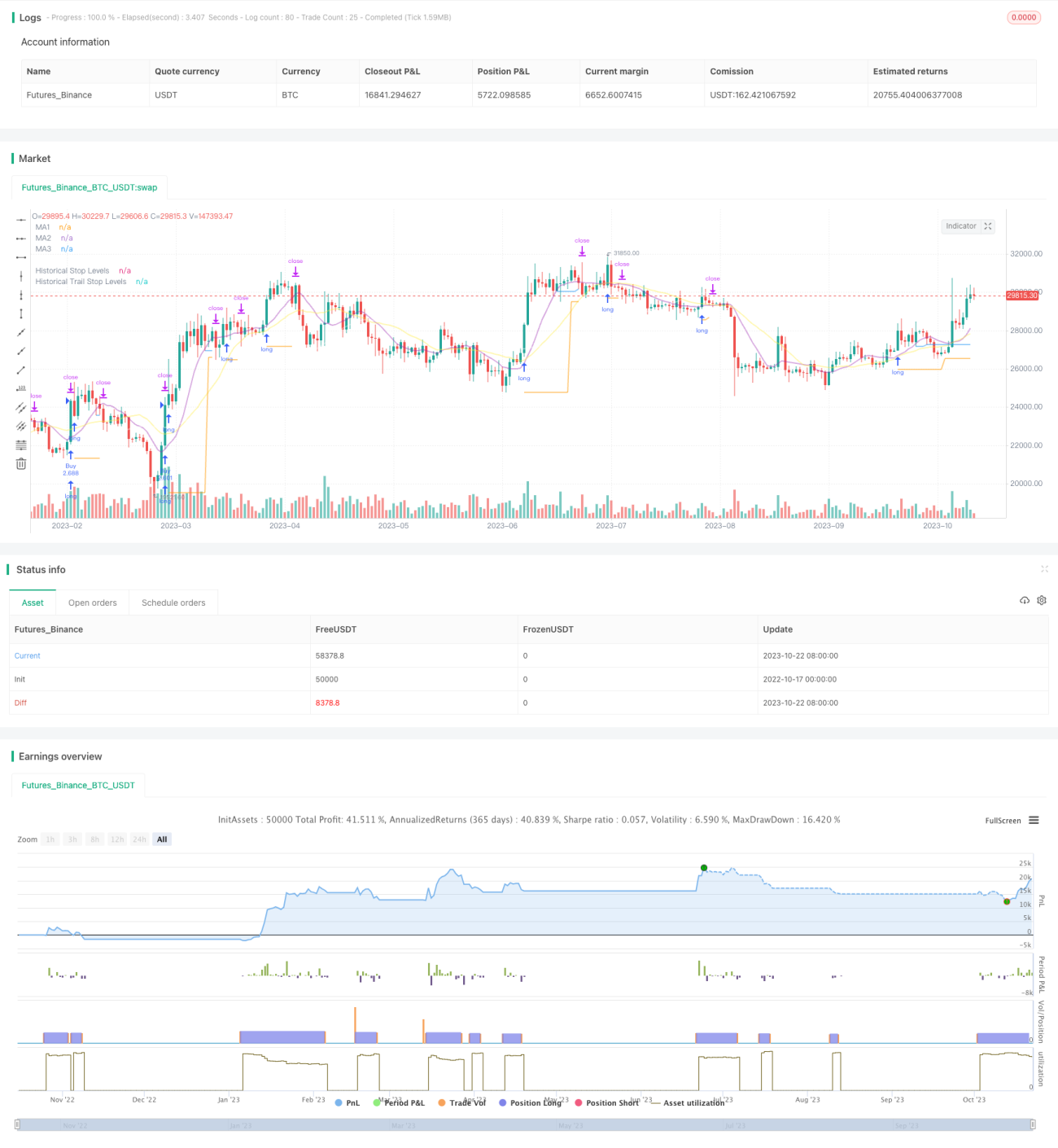

بریک آؤٹ ٹریکنگ سٹاپ لاس V2 حکمت عملی

خلاصہ

یہ حکمت عملی بریک آؤٹ حکمت عملی اور رجحان کی پیروی کرنے والے سٹاپ لاس کی حکمت عملی کے فوائد کو یکجا کرتی ہے۔ اس کا مقصد طویل مدتی چارٹس میں سپورٹ اور مزاحمت کی بریک آؤٹ سگنلز کو پکڑنا ہے، جبکہ موونگ اوسط کا استعمال کرتے ہوئے سٹاپ لاس کو ٹریک کرنا ہے تاکہ طویل مدتی رجحان کی سمت میں منافع کمایا جا سکے اور خطرے کو کنٹرول کیا جا سکے۔

حکمت عملی کا اصول

-

حکمت عملی پہلے مختلف پیرامیٹرز کے ساتھ کئی موونگ اوسطز کا حساب لگاتی ہے، جنہیں بالترتیب رجحان کی تشخیص، سپورٹ/مزاحمت، اور سٹاپ لاس ٹریکنگ کے لیے استعمال کیا جاتا ہے۔

-

پھر مخصوص مدت میں سب سے اونچے اور سب سے نچلے پوائنٹس کو تلاش کر کے انٹری کے لیے سپورٹ اور مزاحمت کے زونز بنائے جاتے ہیں۔ جب قیمت ان سپورٹ/مزاحمت کو توڑتی ہے تو سگنل پیدا ہوتا ہے۔

-

حکمت عملی سب سے اونچے پوائنٹ کے توڑنے کو خریداری کے سگنل اور سب سے نچلے پوائنٹ کے توڑنے کو فروخت کے سگنل کے طور پر استعمال کرتی ہے۔

-

انٹری کے بعد، سب سے نچلے پوائنٹ کو سٹاپ لاس کے طور پر رکھا جاتا ہے تاکہ پوزیشن برقرار رہے۔

-

جب پوزیشن منافع میں آجاتی ہے، تو سٹاپ لاس موونگ اوسط کی پیروی کرنے لگتا ہے۔ جب قیمت موونگ اوسط سے نیچے آتی ہے، تو سٹاپ لاس کو اس کندل کی سب سے کم قیمت پر مقرر کر دیا جاتا ہے۔

-

اس طرح منافع کو محفوظ کیا جا سکتا ہے جبکہ پوزیشن کو رجحان کے ساتھ چلنے کے لیے کافی جگہ ملتی ہے۔

-

حکمت عملی میں اوسط حقیقی حدود (ATR) بھی شامل کی جاتی ہے تاکہ صرف مناسب رینجز میں بریک آؤٹ پر خریدا جا سکے اور حد سے زیادہ پھیلا ہوا بریک آؤٹ سے بچا جا سکے۔

حکمت عملی کے فوائد کا تجزیہ

-

بریک آؤٹ حکمت عملی اور رجحان کی پیروی کرنے والے سٹاپ لاس دونوں کے فوائد یکجا ہیں۔

-

طویل مدتی رجحان کی بنیاد پر بریک آؤٹ خرید کر منافع کا امکان بڑھ جاتا ہے۔

-

سٹاپ لاس حکمت عملی نہ صرف پوزیشن کی حفاظت کرتی ہے بلکہ اسے کافی جگہ بھی دیتی ہے۔

-

وولیٹیٹی فلٹر شامل کرنے سے زیادہ پھیلے ہوئے نقصان دہ بریک آؤٹ سے بچا جاتا ہے۔

-

خودکار تجارت، جزوی وقت کی پیروی کے لیے موزوں۔

-

مختلف ادوار کے موونگ اوسط کو اپنی مرضی کے مطابق استعمال کیا جا سکتا ہے۔

-

سٹاپ لاس ٹریکنگ کے طریقہ کار کو لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے۔

حکمت عملی کے خطرات کا تجزیہ

-

بریک آؤٹ حکمت عملی میں جھوٹے بریک آؤٹ کا خطرہ ہوتا ہے۔ بریک آؤٹ کی تصدیق کو مناسب طور پر ڈھیلا کیا جا سکتا ہے۔

-

سگنل پیدا کرنے کے لیے کافی اتار چڑھاؤ ضروری ہے، جو پریشان کن مارکیٹ میں بے کار ہو سکتا ہے۔

-

کچھ بریک آؤٹ بہت مختصر ہو سکتے ہیں اور پکڑے نہیں جا سکتے۔ مزید مواقع کے لیے ٹائم فریم کم کیا جا سکتا ہے۔

-

ٹریکنگ سٹاپ لاس اتار چڑھاؤ والی مارکیٹ میں بار بار سٹاپ ہو سکتا ہے۔ سٹاپ کے فاصلے کو مناسب طور پر بڑھایا جا سکتا ہے۔

-

وولیٹیٹی فلٹر کچھ مواقع سے محروم کر سکتا ہے۔ فلٹر پیرامیٹر کو کم کیا جا سکتا ہے۔

حکمت عملی کی بہتری کی سمت

-

مختلف موونگ اوسط پیرامیٹرز کے امتزاج کو جانچ کر بہترین پیرامیٹر تلاش کریں۔

-

مختلف بریک آؤٹ تصدیقی میکانزم آزمائیں، جیسے چینل، کندل پیٹرن وغیرہ۔

-

مختلف سٹاپ لاس ٹریکنگ کے طریقے آزمائیں تاکہ بہترین سٹاپ لاس ملے۔

-

سرمایہ کاری کے انتظام کی حکمت عملیوں کو بہتر بنائیں، جیسے پوزیشن سکور وغیرہ۔

-

شماریاتی تکنیکی اشاریوں کو فلٹر کے طور پر شامل کر کے فلٹر کی درستگی بڑھائیں۔

-

مختلف مصنوعات پر اس حکمت عملی کے اثرات کو جانچیں۔

-

مشین لرننگ الگورتھم شامل کر کے حکمت عملی کی کارکردگی بہتر بنائیں۔

خلاصہ

یہ حکمت عملی بریک آؤٹ کے تصور اور رجحان کی پیروی کرنے والے سٹاپ لاس کو یکجا کرتی ہے۔ طویل مدتی رجحان کی درست تشخیص کی صورت میں، یہ منافع کی جگہ کو بہتر بنا سکتی ہے۔ کلید بہترین پیرامیٹرز کا امتزاج تلاش کرنا اور اچھی سرمایہ کاری کے انتظام کی حکمت عملی کے ساتھ اسے استعمال کرنا ہے تاکہ طویل مدتی مواقع کو حاصل کیا جا سکے جبکہ خطرے کو کنٹرول میں رکھا جا سکے۔ مزید بہتری کے بعد یہ حکمت عملی ایک قابل اعتماد طویل مدتی رجحان کی حکمت عملی بن سکتی ہے۔

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1