کثیر جہتی اشاریوں پر مبنی فیصلہ سازی کے ذریعے قلیل مدتی رجحان کی حکمت عملی

خلاصہ

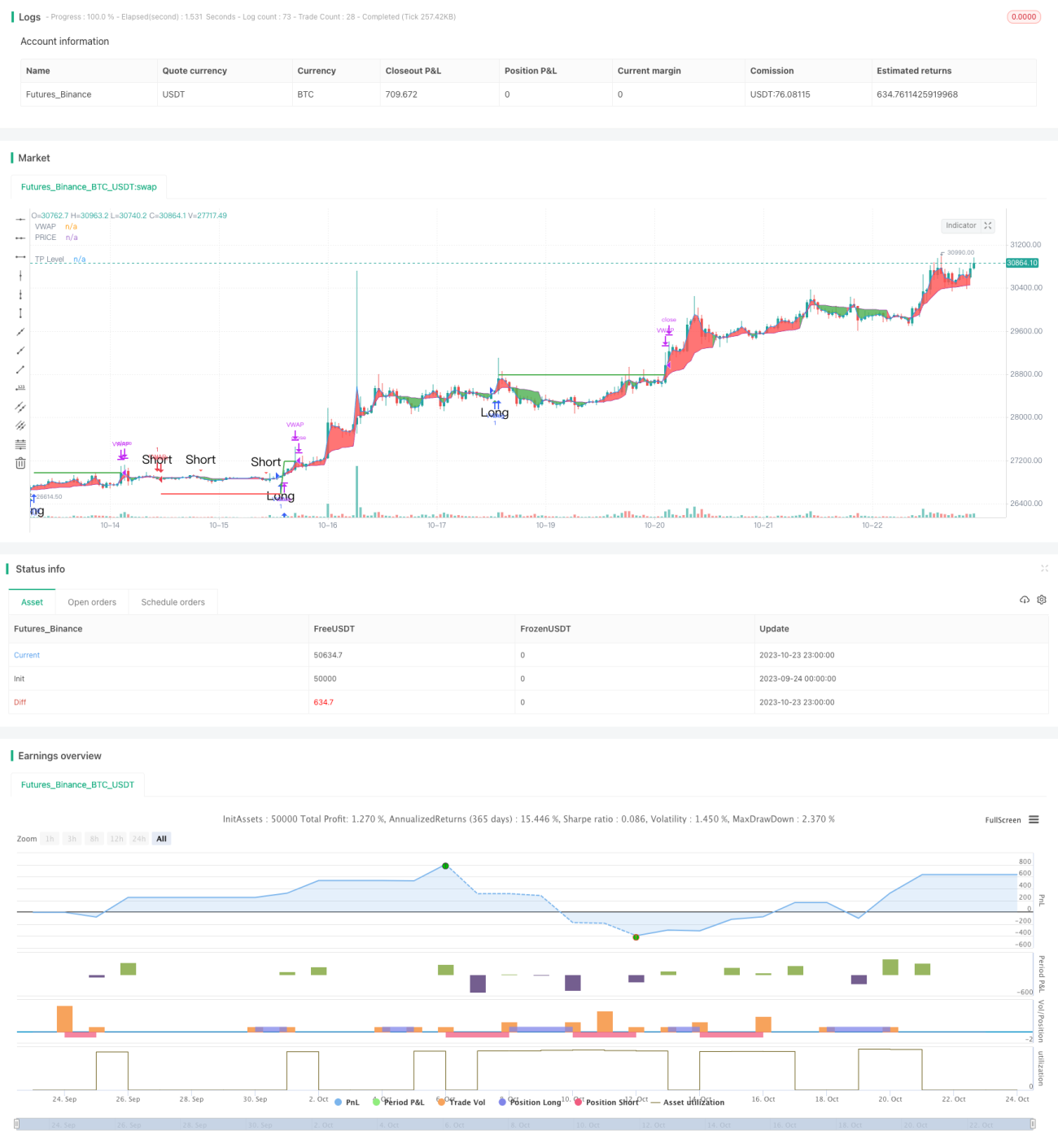

یہ حکمت عملی تین مختلف جہتوں کے تکنیکی اشارے یعنی سپورٹ اور ریزسٹنس لیولز، موونگ ایوریج سسٹم اور اوور باؤٹ/اوور سیلڈ انڈیکیٹرز کو یکجا کرتی ہے، اور ان کے مشترکہ سگنلز کی بنیاد پر قلیل مدتی رجحان کی سمت کا تعین کرتی ہے تاکہ زیادہ جیتنے کی شرح حاصل کی جا سکے۔

حکمت عملی کا اصول

کوڈ میں پہلے قیمت کے سپورٹ اور ریزسٹنس لیولز کا حساب لگایا جاتا ہے، جس میں معیاری آسیلیشن محور اور فبوناچی سپورٹ اور ریزسٹنس لیولز شامل ہیں، اور انہیں چارٹ پر کھینچا جاتا ہے۔ جب قیمت ان اہم سطحوں کو توڑتی ہے تو اسے ایک اہم رجحان کا سگنل سمجھا جاتا ہے۔

اس کے بعد وزنی موونگ ایوریج VWAP اور اوسط قیمت کا حساب لگایا جاتا ہے، اور ان کے گولڈن کراس اور ڈیتھ کراس سگنلز کا تعین کیا جاتا ہے۔ یہ درمیانی سے طویل مدتی رجحان کی تشخیص سے تعلق رکھتا ہے۔

آخر میں Stochastic RSI انڈیکیٹر کا حساب لگایا جاتا ہے، اور اس کے گولڈن کراس اور ڈیتھ کراس سگنلز کا تعین کیا جاتا ہے، جو اوور باؤٹ/اوور سیلڈ انڈیکیٹر سے تعلق رکھتا ہے۔

ان تینوں جہتوں کے اشارے کو یکجا کرتے ہوئے، اگر سپورٹ اور ریزسٹنس لیولز، VWAP موونگ ایوریج اور Stochastic RSI ایک ساتھ خریداری کا سگنل دیں تو لانگ پوزیشن کھولی جاتی ہے؛ اور اگر تینوں ایک ساتھ فروخت کا سگنل دیں تو شارٹ پوزیشن کھولی جاتی ہے۔

فوائد کا تجزیہ

اس حکمت عملی کا سب سے بڑا فائدہ یہ ہے کہ یہ تین مختلف جہتوں کے اشارے کو جوڑتی ہے، جس سے تشخیص زیادہ جامع اور درست ہوتی ہے اور جیتنے کی شرح زیادہ ہوتی ہے۔ پہلے سپورٹ اور ریزسٹنس لیولز بڑے رجحان کا تعین کرتے ہیں؛ پھر VWAP درمیانی سے طویل مدتی رجحان کا تعین کرتا ہے؛ اور آخر میں Stochastic RSI اوور باؤٹ/اوور سیلڈ کی صورت حال کا تعین کرتا ہے۔ تینوں جہتوں کے اشارے بیک وقت سگنل دیتے ہیں، جس سے جھوٹے سگنلز کو بڑی حد تک فلٹر کیا جا سکتا ہے اور داخلے کی کامیابی کی شرح میں اضافہ ہوتا ہے۔

اس کے علاوہ، حکمت عملی میں منافع بند کرنے (ٹیک پرافٹ) کی خصوصیت شامل ہے، جس سے ایک خاص تناسب کے منافع کو مقفل کیا جا سکتا ہے، جو سرمایہ کے انتظام میں مددگار ہے۔

خطرات کا تجزیہ

اس حکمت عملی کا بنیادی خطرہ یہ ہے کہ خرید و فروخت کے فیصلے اشارے کے بیک وقت سگنل دینے پر منحصر ہیں، اگر کچھ اشارے غلط سگنل دیں تو فیصلہ غلط ہو سکتا ہے۔ مثال کے طور پر، Stochastic RSI اوور باؤٹ سگنل دیتا ہے، لیکن VWAP اور سپورٹ/ریزسٹنس اب بھی تیزی کا رجحان دکھاتے ہیں، تو اس صورت میں خریداری کا موقع ضائع ہو سکتا ہے اور داخلہ نہیں ہو پاتا۔

اس کے علاوہ، اشارے کے پیرامیٹرز کا غلط تعین بھی سگنل کی غلط تشخیص کا سبب بن سکتا ہے، جس کے لیے بہترین پیرامیٹرز تلاش کرنے کے لیے بار بار بیک ٹیسٹنگ کی ضرورت ہے۔

مزید برآں، اسٹاک مارکیٹ میں مختصر مدت میں کبھی کبھار بلیک سوان واقعات رونما ہوتے ہیں، جس سے اشارے بے اثر ہو سکتے ہیں۔ اس خطرے سے بچنے کے لیے، سٹاپ لاس حکمت عملی شامل کی جا سکتی ہے تاکہ ایک ہی تجارت میں زیادہ نقصان سے بچا جا سکے۔

بہتری کے راستے

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

-

مزید اشارے شامل کرنا، جیسے والیوم انڈیکیٹر، تاکہ رجحان کی مضبوطی کا تعین کیا جا سکے اور فیصلے کی درستگی بڑھائی جا سکے۔

-

مشین لرننگ ماڈلز شامل کرنا، تاکہ کثیر جہتی اشارے پر تربیت دی جا سکے اور خود بخود بہترین تجارتی حکمت عملی تلاش کی جا سکے۔

-

مختلف مصنوعات کے پیرامیٹرز کے مطابق اصلاح کرنا، اور خود موافق پیرامیٹرز ترتیب دینا۔

-

سٹاپ لاس حکمت عملی شامل کرنا، اور ڈرا ڈاؤن کی بنیاد پر پوزیشن کے سائز کو کنٹرول کرنا، تاکہ خطرے کو بہتر طریقے سے کنٹرول کیا جا سکے۔

-

پورٹ فولیو میں اصلاح کرنا، کم ارتباط والی مصنوعات تلاش کرنا اور ان کا مجموعہ بنانا، تاکہ پورٹ فولیو کے ڈرا ڈاؤن کو کم کیا جا سکے۔

خلاصہ

یہ حکمت عملی مجموعی طور پر قلیل مدتی رجحان کی تجارت کے لیے بہت موزوں ہے۔ یہ کثیر جہتی اشارے کا استعمال کرتے ہوئے فیصلے کرتی ہے، جس سے بہت زیادہ شور کو فلٹر کیا جا سکتا ہے اور جیتنے کی شرح زیادہ ہوتی ہے۔ تاہم، اشارے کے غلط سگنل دینے کے خطرے پر توجہ دینی چاہیے۔ مزید بہتری کے ذریعے، یہ حکمت عملی ایک موثر اور مستحکم مختصر مدتی حکمت عملی بن سکتی ہے۔

- 1