سپر ایچیموکو رجحان کی حکمت عملی

جائزہ

چاؤ یی حکمت عملی ایک رجحان تجارتی حکمت عملی ہے جو چاؤ یی اشارے کی بنیاد پر تجارتی فیصلے کرتی ہے۔ یہ حکمت عملی چاؤ یی اشارے کی تبدیلی لائن، بنیادی لائن اور بادل کی پٹی کے تعلقات کا استعمال کرتے ہوئے موجودہ رجحان کی سمت کا تعین کرتی ہے اور قیمت کی واپسی کے ساتھ مل کر داخلی مقام کا تعین کرتی ہے۔

چاؤ یی حکمت عملی بنیادی طور پر درمیانی سے طویل مدتی رجحان کی تجارت کے لیے موزوں ہے اور بڑے رجحانات میں منافع کما سکتی ہے۔ اس حکمت عملی میں رجحان کی شناخت کی مضبوط صلاحیت بھی ہے۔

حکمت عملی کا اصول

چاؤ یی حکمت عملی تجارتی سمت کا تعین کرنے کے لیے درج ذیل عناصر کا جائزہ لیتی ہے:

-

تبدیلی لائن اور بنیادی لائن کا تعلق: جب تبدیلی لائن اوپر ہو تو تیزی کا رجحان (bullish) اور جب نیچے ہو تو مندی کا رجحان (bearish)

-

بادل کی پٹی کا رنگ: جب بادل کی پٹی سبز ہو تو تیزی کا اور جب سرخ ہو تو مندی کا رجحان

-

قیمت کی واپسی: قیمت کا تبدیلی لائن اور بنیادی لائن کے باہر واپس آنا ضروری ہے، تبھی داخلی مقام ممکن ہے

خاص طور پر، حکمت عملی کے تجارتی اشارے درج ذیل ہیں:

تیزی کے اشارے (لانگ سگنل):

- تبدیلی لائن بنیادی لائن سے اوپر ہو

- قیمت تبدیلی لائن اور بنیادی لائن سے اوپر ہو

- تبدیلی لائن اور بنیادی لائن بادل کی پٹی سے اوپر ہوں

- قیمت تبدیلی لائن اور بنیادی لائن کے نیچے واپس آئے

مندی کے اشارے (شارٹ سگنل):

- تبدیلی لائن بنیادی لائن سے نیچے ہو

- قیمت تبدیلی لائن اور بنیادی لائن سے نیچے ہو

- تبدیلی لائن اور بنیادی لائن بادل کی پٹی سے نیچے ہوں

- قیمت تبدیلی لائن اور بنیادی لائن کے اوپر واپس آئے

جب بیک وقت تیزی/مندی کے اشارے پورے ہوں تو پوزیشن کی صورت حال کے مطابق کھولنے کا عمل کیا جاتا ہے۔

فوائد کا تجزیہ

چاؤ یی حکمت عملی کے درج ذیل فوائد ہیں:

-

چاؤ یی اشارے کے امتزاج سے رجحان کی سمت کا تعین، درستگی کی شرح زیادہ

-

تبدیلی لائن اور بنیادی لائن درمیانی اور مختصر مدت کے رجحان کو واضح طور پر جانچ سکتی ہیں، جبکہ بادل کی پٹی طویل مدتی رجحان کا تعین کرتی ہے

-

شرط میں قیمت کا تبدیلی لائن پر واپس آنا ضروری ہے، جو جھوٹے بریک آؤٹ سے ہونے والے نقصان سے بچاتا ہے

-

رسک کنٹرول میں حالیہ مدت کی سب سے زیادہ اور سب سے کم قیمتوں پر اسٹاپ لاس مقرر کرنا، ہر تجارت کے نقصان کو مؤثر طریقے سے کنٹرول کرتا ہے

-

منافع اور نقصان کا تناسب معقول، مستحکم آمدنی کا ہدف

-

مختلف ٹائم فریموں پر لاگو کیا جا سکتا ہے، درمیانی سے طویل مدتی رجحان کی تجارت کے لیے موزوں

-

حکمت عملی کا تصور واضح اور سمجھنے میں آسان، پیرامیٹرز کی اصلاح کی بڑی گنجائش

-

مختلف مارکیٹ ماحول میں اچھی کارکردگی دکھا سکتی ہے

خطرات کا تجزیہ

چاؤ یی حکمت عملی میں درج ذیل خطرات بھی ہیں:

-

اتار چڑھاؤ والی مارکیٹ میں، اسٹاپ لاس بار بار چالو ہو سکتا ہے، منافع پر اثر ڈالتا ہے

-

جب رجحان تیزی سے تبدیل ہوتا ہے، پوزیشن کو بروقت ریورس نہ کرنے سے نقصان ہو سکتا ہے

-

مقرر کردہ منافع/نقصان کا تناسب تمام مصنوعات کے لیے موزوں نہیں، مختلف اہداف کے لیے پیرامیٹرز کو ایڈجسٹ کرنے کی ضرورت ہے

-

جب بادل کی پٹی کو توڑنے کے بعد اضافے کی گنجائش محدود ہو تو منافع محدود ہو سکتا ہے

-

اشارے کے پیرامیٹرز کو بار بار جانچ اور بہتر بنانے کی ضرورت ہے، ایسی اشیاء کے لیے موزوں نہیں جن میں پیرامیٹرز کی بار بار ایڈجسٹمنٹ کی ضرورت ہو

درج ذیل طریقوں سے خطرات کو کم کیا جا سکتا ہے:

-

پیرامیٹرز کو بہتر بنائیں تاکہ وہ مختلف ٹائم فریموں اور مصنوعات کی خصوصیات کے مطابق ہوں

-

دوسرے اشاروں کے ساتھ داخلی مقام کے اشاروں کو فلٹر کریں، اتار چڑھاؤ والی مارکیٹ میں جھوٹے بریک آؤٹ سے بچیں

-

اسٹاپ لاس کی پوزیشن کو متحرک طور پر ایڈجسٹ کریں، اسٹاپ لاس چالو ہونے کے امکان کو کم کریں

-

مختلف منافع/نقصان کے تناسب کی ترتیبات کی جانچ کریں

-

چارٹ پیٹرن وغیرہ استعمال کرکے رجحان کے اشارے کی طاقت کا تعین کریں

بہتری کی سمت

چاؤ یی حکمت عملی کو درج ذیل پہلوؤں سے بہتر کیا جا سکتا ہے:

-

تبدیلی لائن اور بنیادی لائن کے پیرامیٹرز کو بہتر بنائیں تاکہ وہ تجارت کردہ مصنوعات کی خصوصیات کے مطابق ہوں

-

بادل کی پٹی کے پیرامیٹرز کو بہتر بنائیں تاکہ طویل مدتی رجحان کا تعین زیادہ درست ہو

-

اسٹاپ لاس الگورتھم کو بہتر بنائیں، جیسے ATR کی بنیاد پر اسٹاپ لاس یا متحرک اسٹاپ لاس

-

دوسرے اشاروں کے ساتھ اشاروں کو فلٹر کریں، مزید فلٹر شرائط ترتیب دیں، غلط داخلی مقام کے امکان کو کم کریں

-

منافع/نقصان کے تناسب کی ترتیبات کو بہتر بنائیں تاکہ مختلف مصنوعات اور ٹائم فریموں پر حکمت عملی کی خصوصیات کے مطابق ہوں

-

مارٹنگیل طریقہ استعمال کرکے پوزیشن کا انتظام کریں، مختلف مارکیٹ اتار چڑھاؤ کی تعدد کے مطابق

-

مشین لرننگ کے طریقے استعمال کرکے پیرامیٹرز کو بہتر بنائیں، زیادہ استحکام حاصل کریں

-

مختلف تجارتی اوقات مقرر کریں، رات کے سیشن اور دن کے سیشن کے درمیان مارکیٹ کی خصوصیات کے مطابق ایڈجسٹ کریں

خلاصہ

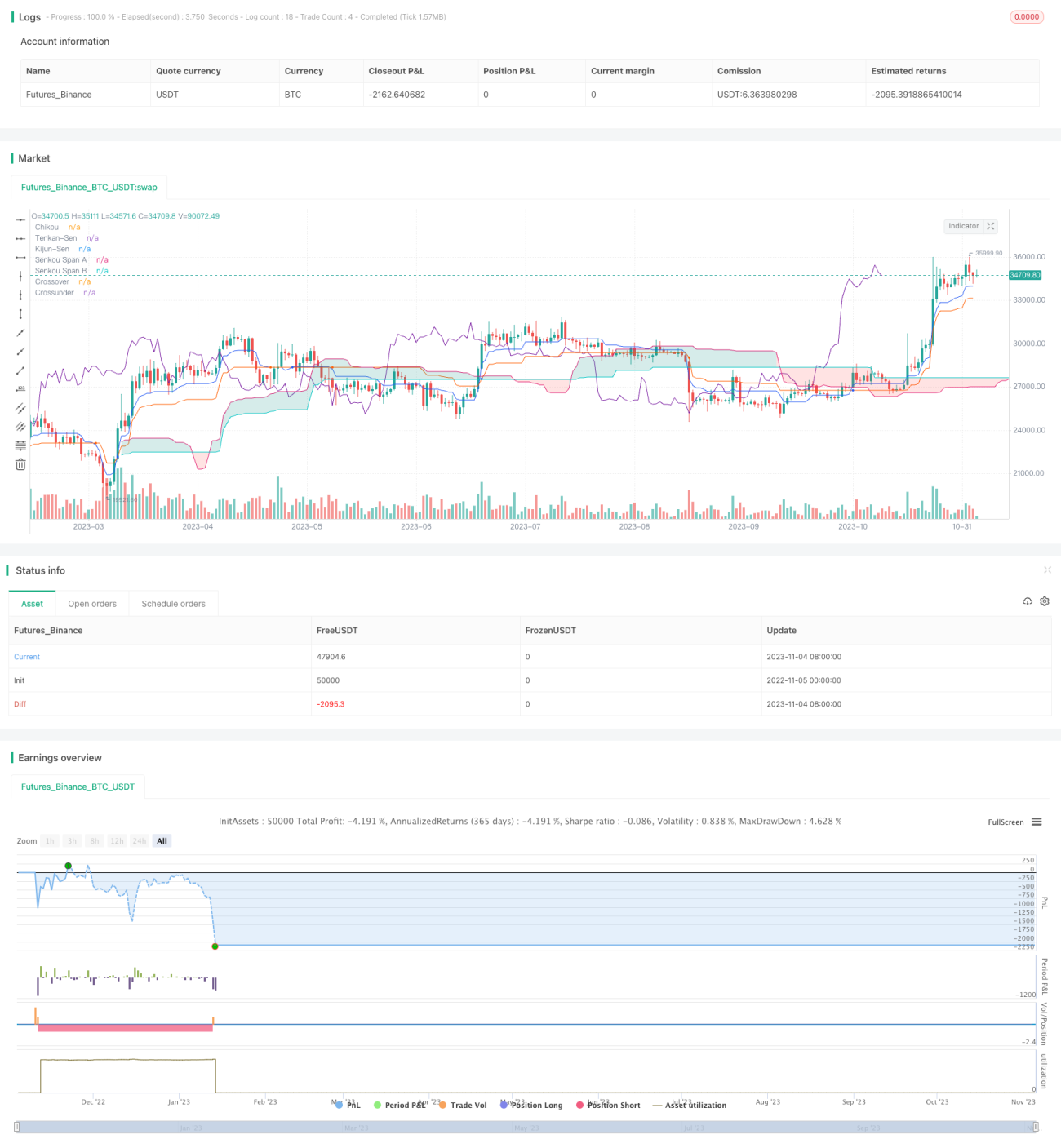

چاؤ یی حکمت عملی مجموعی طور پر درمیانی سے طویل مدتی رجحان کی تجارت کے لیے ایک بہت موزوں حکمت عملی ہے۔ اس میں چاؤ یی اشارے کے ذریعے رجحان کی سمت کا تعین کرنے کا واضح فائدہ ہے، اور قیمت کی واپسی کے ساتھ داخلی مقام غلط داخلی مقام سے بچنے میں مؤثر ہے۔ پیرامیٹرز کی ترتیبات کو بہتر بنا کر، حکمت عملی کو مزید مصنوعات اور مزید ٹائم فریموں پر مستحکم منافع حاصل کرنے کے قابل بنایا جا سکتا ہے۔ یہ حکمت عملی نہ صرف سمجھنے میں آسان ہے بلکہ اس میں بہتری کی بڑی گنجائش بھی ہے، اور یہ حکمت عملی کی تحقیق اور سیکھنے کے لیے بنیادی حکمت عملیوں میں سے ایک کے طور پر موزوں ہے۔

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1