دو وقتی فریم ورک اور موومنٹ انڈیکیٹر پر مبنی انکولی منافع روکنے اور نقصان روکنے کی حکمت عملی

جائزہ

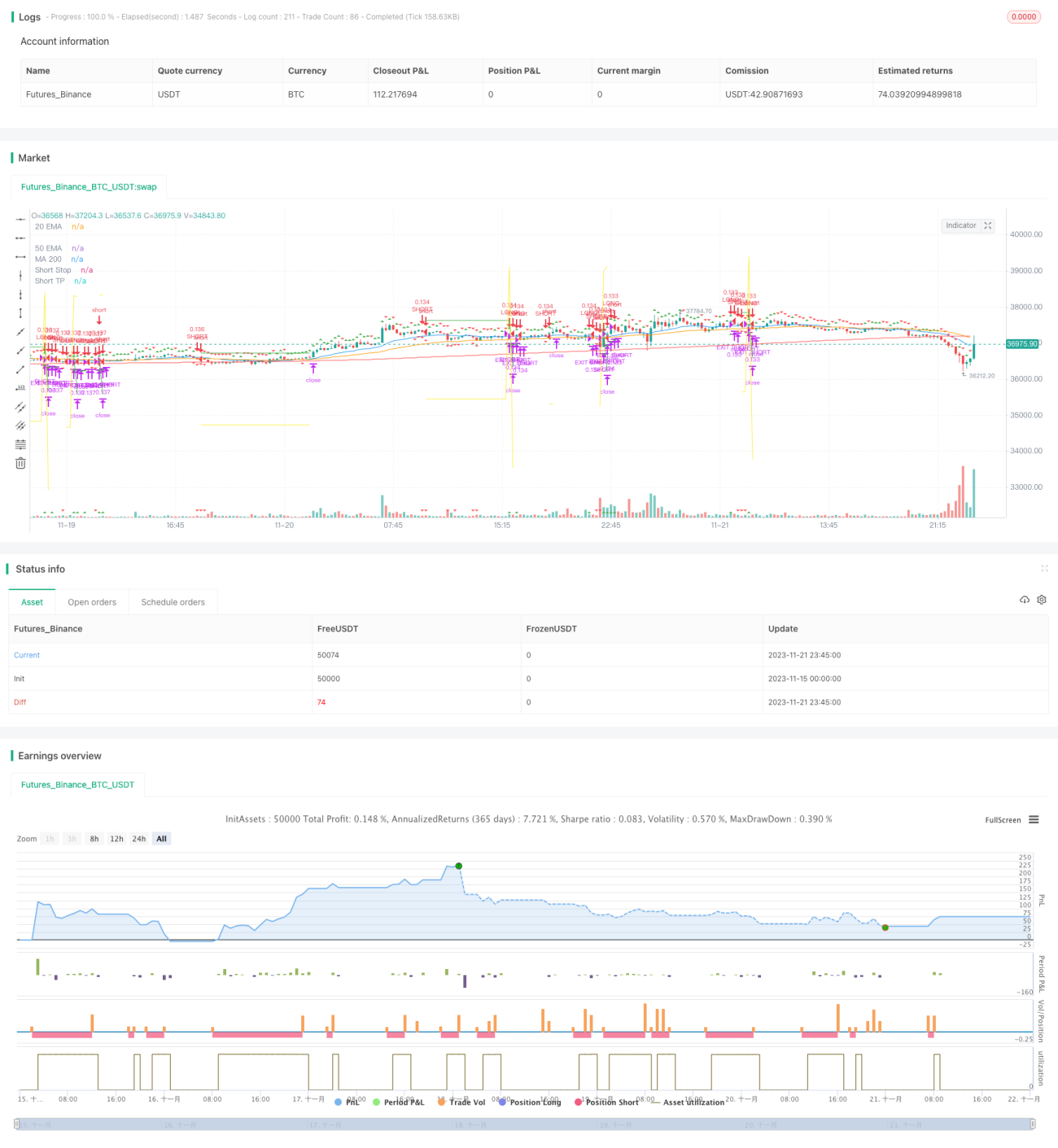

یہ حکمت عملی دو وقتی فریم اور موومنٹ انڈیکیٹر کے امتزاج کو استعمال کرتی ہے، تاکہ خودکار منافع کی حد اور نقصان کی حد کو حاصل کیا جا سکے۔ مرکزی وقتی فریم رجحان کی سمت کی نگرانی کرتا ہے، معاون وقتی فریم سگنل کی تصدیق کے لیے استعمال ہوتا ہے۔ جب دونوں کی سمت ایک جیسی ہوتی ہے تو تجارتی سگنل پیدا ہوتا ہے۔ مارکیٹ میں داخل ہونے کے بعد، ترقی پذیر منافع کی حد کے طریقے سے منافع کی حد اور نقصان کی حد کو اپ ڈیٹ کیا جاتا ہے۔

حکمت عملی کا اصول

-

مرکزی وقتی فریم لکیری رجعت انڈیکیٹر Sqqueeze Momentum (SQM) کا استعمال کرتے ہوئے رجحان کا تعین کرتا ہے، معاون وقتی فریم SQM انڈیکیٹر کے EMA امتزاج سے جعلی سگنلز کو فلٹر کرتا ہے۔

-

جب مرکزی چارٹ پر SQM اوپر کی طرف بریک آؤٹ کرتا ہے اور معاون چارٹ پر SQM بھی اوپر کی طرف ہوتا ہے تو لمبا کریں؛ جب مرکزی چارٹ پر SQM نیچے کی طرف بریک آؤٹ کرتا ہے اور معاون چارٹ پر SQM بھی نیچے کی طرف ہوتا ہے تو چھوٹا کریں۔

-

مارکیٹ میں داخل ہونے کے بعد، ان پٹ پیرامیٹرز کے مطابق ابتدائی منافع کی حد اور نقصان کی حد مقرر کی جاتی ہے۔ جب قیمت منافع کی حد تک پہنچ جاتی ہے تو منافع کی حد اور نقصان کی حد کو اپ ڈیٹ کیا جاتا ہے۔ مخصوص طریقہ یہ ہے: منافع کی حد مقررہ تناسب سے بڑھتی ہے، نقصان کی حد تناسب سے کم ہوتی ہے، اس طرح ترقی پذیر منافع کی حد حاصل ہوتی ہے۔

حکمت عملی کے فوائد

-

دو وقتی فریم جعلی سگنلز کو فلٹر کرتے ہیں، سگنل کی درستگی کو یقینی بناتے ہیں۔

-

SQM انڈیکیٹر رجحان کی سمت کا تعین کرتا ہے، مارکیٹ کے شور سے بچاتا ہے۔

-

خودکار منافع اور نقصان کے تعین کا طریقہ کار، منافع کو زیادہ سے زیادہ محفوظ کرتا ہے اور خطرے کو مؤثر طریقے سے کنٹرول کرتا ہے۔

خطرے کا تجزیہ

-

SQM انڈیکیٹر پیرامیٹرز کی غلط ترتیب سے رجحان کے موڑ سے محروم ہو سکتے ہیں، جس سے نقصان ہو سکتا ہے۔

-

معاون چارٹ کے وقتی فریم کا غلط انتخاب شور کو مؤثر طریقے سے فلٹر نہیں کر سکتا، جس سے غلط تجارت ہو سکتی ہے۔

-

نقصان کی حد کی مقدار بہت زیادہ ہونے کی صورت میں ایک تجارت میں بھاری نقصان ہو سکتا ہے۔

اصلاح کی سمت

-

SQM انڈیکیٹر پیرامیٹرز کو مختلف مارکیٹوں کے مطابق ایڈجسٹ کرنے کی ضرورت ہے تاکہ ان کی حساسیت کو یقینی بنایا جا سکے۔

-

معاون چارٹ کے وقتی فریم کو بھی مختلف ادوار میں جانچنے کی ضرورت ہے تاکہ دیکھا جا سکے کہ کون سا دور سب سے بہتر فلٹرنگ فراہم کرتا ہے۔

-

نقصان کی حد کی مقدار کو ایک متغیر رینج کے طور پر مقرر کیا جا سکتا ہے، نہ کہ ایک مقررہ قدر، تاکہ مارکیٹ کے اتار چڑھاؤ کے مطابق ایڈجسٹ کیا جا سکے۔

خلاصہ

یہ حکمت عملی مجموعی طور پر بہت عملی ہے، دو وقتی فریم موومنٹ انڈیکیٹر کے ساتھ رجحان کا تعین کرتے ہیں، اور خودکار منافع اور نقصان کی حد کے طریقے سے مستحکم منافع حاصل کرتے ہیں۔ SQM انڈیکیٹر پیرامیٹرز، معاون چارٹ کی مدت اور نقصان کی حد کی مقدار کو بہتر بنا کر حکمت عملی کو مزید بہتر بنایا جا سکتا ہے، اور یہ حقیقی تجارت میں استعمال اور بہتری کے قابل ہے۔

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1