EMA اوسطوں پر مبنی تجارتی حکمت عملی

جائزہ

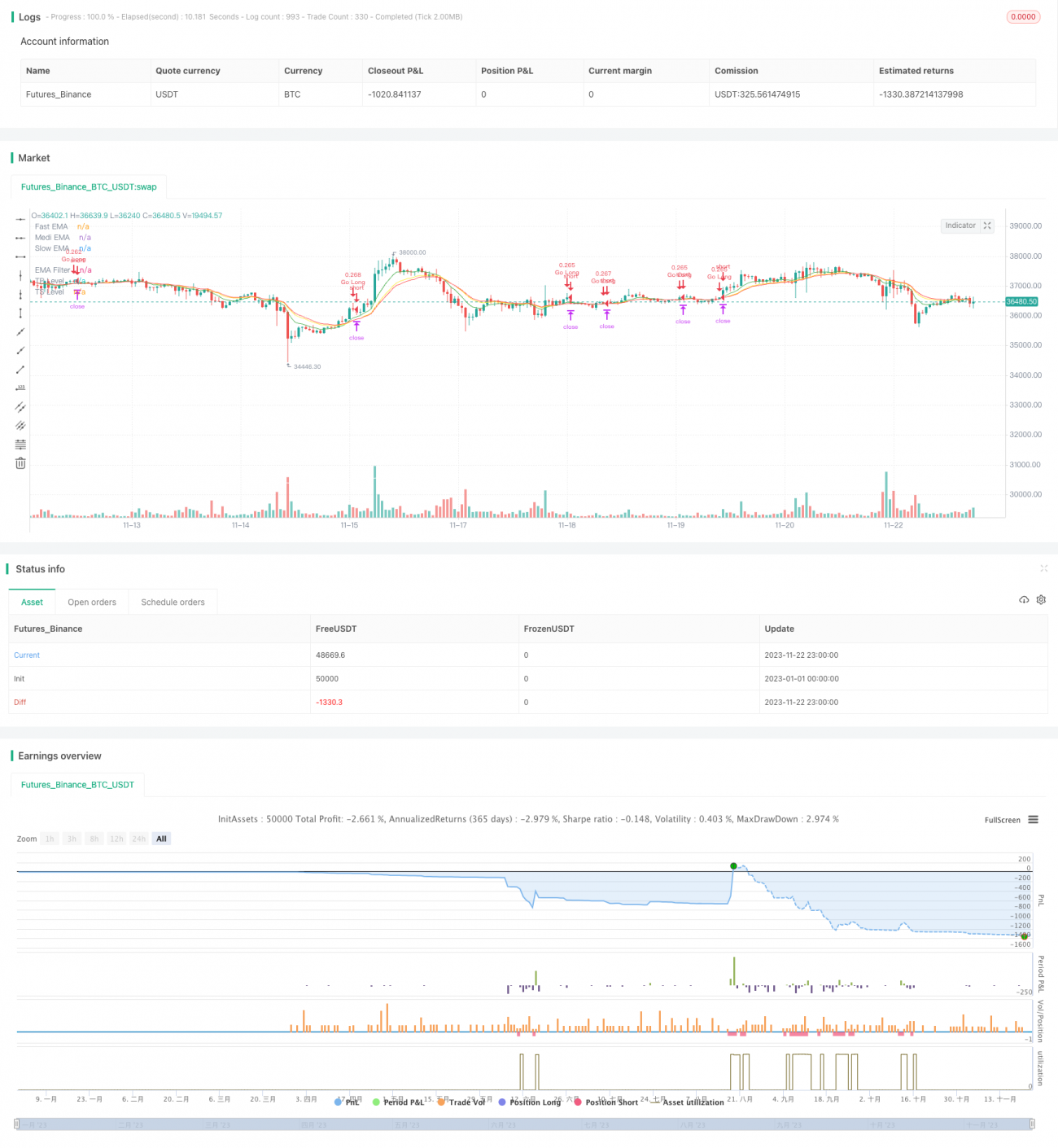

یہ حکمت عملی 4 مختلف ادوار کی EMA اوسط کا استعمال کرتی ہے، اور ان کی ترتیب کی بنیاد پر تجارتی سگنل تیار کرتی ہے، جو ٹریفک لائٹ کے سرخ، پیلے اور سبز رنگوں سے مشابہت رکھتی ہے، اسی لیے اسے "ٹریفک لائٹ ٹریڈنگ اسٹریٹیجی" کا نام دیا گیا ہے۔ یہ رجحان اور الٹ دونوں زاویوں سے مارکیٹ کا مجموعی جائزہ لیتی ہے، جس کا مقصد تجارتی فیصلوں کی درستگی کو بہتر بنانا ہے۔

حکمت عملی کا اصول

-

تیز لکیر (8 ادوار)، درمیانی لکیر (14 ادوار)، سست لکیر (16 ادوار) کی 3 EMA اوسطیں سیٹ کریں، اور ایک طویل المدت (100 ادوار) EMA اوسط بطور فلٹر شامل کریں۔

-

تینوں اوسطوں (تیز، درمیانی، سست) کی ترتیب اور فلٹر کے ساتھ ان کے کراس اوور کی بنیاد پر خرید و فروخت کے مواقع کا تعین کریں:

-

جب تیز لکیر درمیانی لکیر کو اوپر سے عبور کرے یا درمیانی لکیر سست لکیر کو اوپر سے عبور کرے تو اسے خرید سگنل سمجھا جائے گا

-

جب درمیانی لکیر تیز لکیر کو نیچے سے عبور کرے تو اسے خرید بند کرنے کا سگنل سمجھا جائے گا

-

جب تیز لکیر درمیانی لکیر کو نیچے سے عبور کرے یا درمیانی لکیر سست لکیر کو نیچے سے عبور کرے تو اسے فروخت سگنل سمجھا جائے گا

-

جب درمیانی لکیر تیز لکیر کو اوپر سے عبور کرے تو اسے فروخت بند کرنے کا سگنل سمجھا جائے گا

-

-

تیز، درمیانی اور سست تینوں اوسطوں کی ترتیب سے رجحان کی سمت اور قوت کا تعین کریں، اور اوسطوں کے فلٹر کے ساتھ کراس اوور سے الٹ کے مقامات کا تعین کریں، اس طرح رجحان کی پیروی اور الٹ کو پکڑنے کا مؤثر امتزاج حاصل ہوتا ہے۔

فوائد کا تجزیہ

یہ حکمت عملی رجحان کی پیروی اور الٹ کی ٹریڈنگ کے فوائد کو یکجا کرتی ہے، اور مارکیٹ کے مواقع کو بہتر طریقے سے حاصل کر سکتی ہے۔ اہم فوائد یہ ہیں:

- متعدد EMA اوسطوں کا استعمال، جس سے فیصلہ سازی کی طاقت بڑھ جاتی ہے اور جھوٹے سگنل کم ہو جاتے ہیں

- خرید و فروخت کی شرائط لچکدار طریقے سے سیٹ کی جا سکتی ہیں، جس سے تجارتی مواقع ضائع ہونے سے بچا جا سکتا ہے

- مختصر اور طویل المدت اوسطوں کا جامع استعمال، جس سے فیصلہ سازی مکمل ہو جاتی ہے

- منافع اور نقصان کو روکنے کی شرائط حسب مرضی سیٹ کی جا سکتی ہیں، جس سے رسک کنٹرول بہتر ہوتا ہے

پیرامیٹرز کو بہتر بنا کر، یہ حکمت عملی مزید مصنوعات کے مطابق ڈھل سکتی ہے، اور بیک ٹیسٹنگ میں مضبوط منافع کی صلاحیت اور استحکام دکھاتی ہے۔

خطرات کا تجزیہ

اس حکمت عملی کے اہم خطرات درج ذیل ہیں:

- جب متعدد EMA اوسطوں کی ترتیب میں الجھن پیدا ہو جائے تو فیصلہ سازی مشکل ہو جاتی ہے، جس سے تجارت میں تاخیر ہو سکتی ہے

- مارکیٹ میں غیر معمولی اتار چڑھاؤ کے جھوٹے سگنلز کو مؤثر طریقے سے فلٹر نہیں کیا جا سکتا، جیسے بڑے پیمانے پر اتار چڑھاؤ میں نقصان ہو سکتا ہے

- جب پیرامیٹرز درست طریقے سے سیٹ نہ کیے جائیں تو منافع اور نقصان کو روکنے کی شرائط بہت زیادہ نرم یا سخت ہو سکتی ہیں، جس سے منافع ضائع ہو سکتا ہے یا زیادہ نقصان ہو سکتا ہے

سفارش کی جاتی ہے کہ پیرامیٹرز کو بہتر بنا کر، نقصان کی سطح مقرر کر کے، اور محتاط انداز میں تجارت کر کے حکمت عملی کے استحکام کو مزید بہتر بنایا جائے اور خطرات پر قابو پایا جائے۔

بہتری کے رخ

اس حکمت عملی کی بہتری کے اہم رخ:

- EMA اوسطوں کے دورانیے کے پیرامیٹرز کو ایڈجسٹ کریں تاکہ مزید مصنوعات کے مطابق ڈھل سکے

- دیگر انڈیکیٹرز جیسے MACD، بولنگر بینڈ وغیرہ شامل کریں تاکہ فیصلہ سازی کی درستگی بہتر ہو

- منافع اور نقصان کو روکنے کے تناسب کو بہتر بنائیں تاکہ خطرے اور منافع کے درمیان بہترین توازن حاصل ہو

- خودکار نقصان روکنے کا طریقہ کار شامل کریں، جیسے ATR کی بنیاد پر نقصان روکنا، تاکہ نیچے کی طرف کے خطرے کو مزید کم کیا جا سکے

پیرامیٹرز میں متنوع ایڈجسٹمنٹ اور رسک کنٹرول کے طریقوں کو شامل کر کے حکمت عملی کے استحکام اور منافع کی صلاحیت کو مسلسل بہتر بنایا جا سکتا ہے۔

خلاصہ

یہ ٹریفک لائٹ ٹریڈنگ اسٹریٹیجی رجحان کی پیروی اور الٹ کے تعین کو یکجا کرتی ہے، 4 EMA اوسطوں کا استعمال کرتے ہوئے تجارتی سگنل تیار کرتی ہے، اور پیرامیٹرز کو بہتر بنا کر مزید مصنوعات کے مطابق ڈھلتی ہے، جو بیک ٹیسٹنگ میں مضبوط منافع کی صلاحیت دکھاتی ہے۔ مستقبل میں مزید رسک کنٹرول اور متنوع انڈیکیٹرز کو شامل کر کے یہ ایک مستحکم اور مؤثر مقداری تجارتی حکمت عملی بن سکتی ہے۔

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1