نقطہ تبدیلی پر مبنی RSI انحراف حکمت عملی

خلاصہ

یہ حکمت عملی، جسے "Pivot-based RSI Divergence Strategy" کہا جاتا ہے، RSI انڈیکیٹر کے مختلف ادوار پر ڈائیورجنس (Divergence) کا استعمال کرتے ہوئے خرید و فروخت کے مقامات کا تعین کرتی ہے۔ اس میں طویل مدتی RSI کو فلٹر کے طور پر شامل کیا گیا ہے، جس سے حکمت عملی کی استحکام میں اضافہ ہوتا ہے۔

حکمت عملی کا اصول

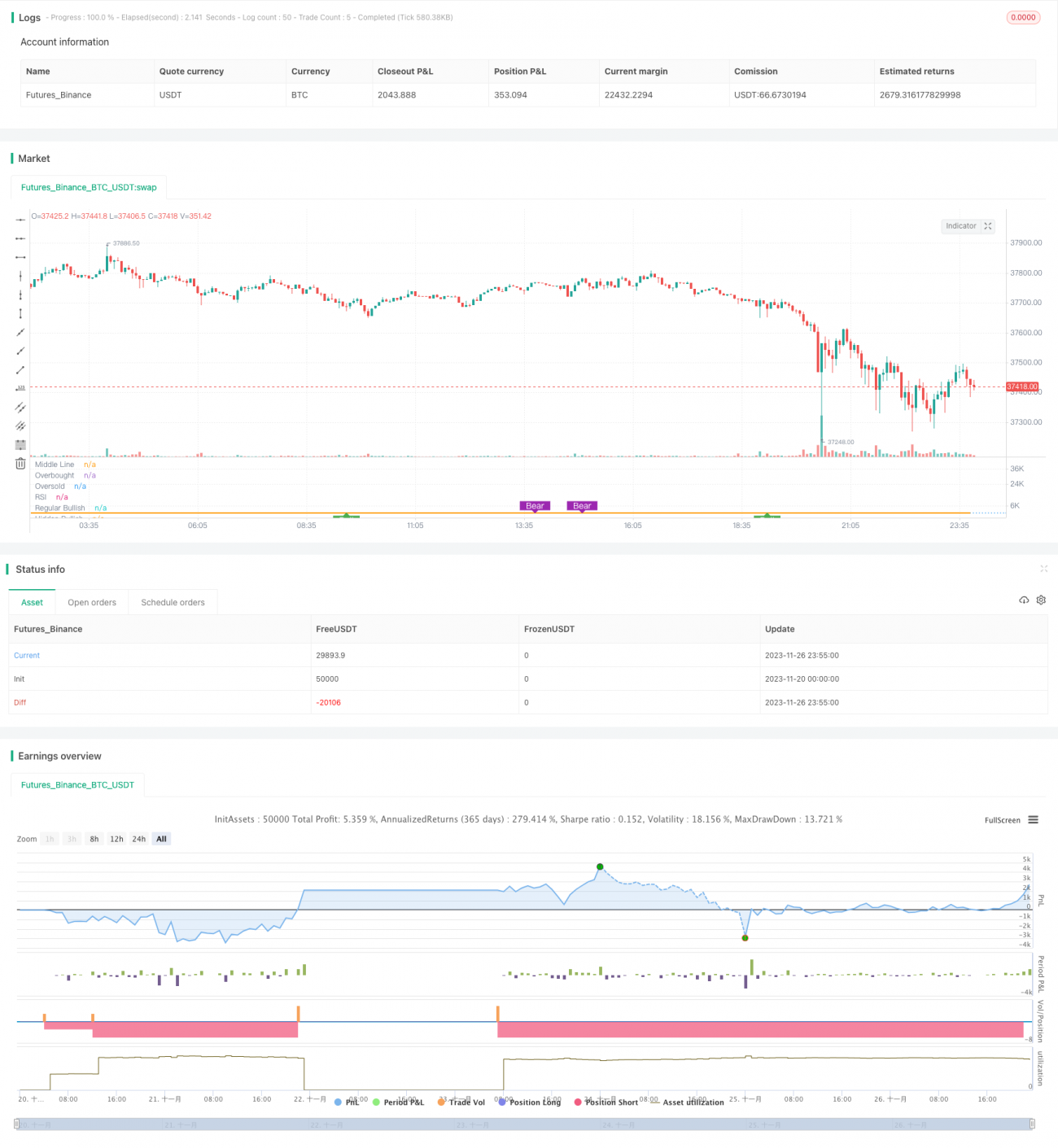

یہ حکمت عملی بنیادی طور پر اس بات کا جائزہ لیتی ہے کہ جب مختصر مدت کا RSI (مثلاً 5 دن کا RSI) اور قیمت کے درمیان "مخفی تیزی کا ڈائیورجنس" (Hidden Bullish Divergence) یا "عام تیزی کا ڈائیورجنس" (Regular Bullish Divergence) ظاہر ہو تو خریداری کا موقع ہوتا ہے۔ اور جب "مخفی مندی کا ڈائیورجنس" (Hidden Bearish Divergence) یا "عام مندی کا ڈائیورجنس" (Regular Bearish Divergence) نظر آئے تو فروخت کا موقع ہوتا ہے۔

"عام تیزی کا ڈائیورجنس" سے مراد یہ ہے کہ قیمت نئی کم ترین سطح (New Low) بنائے لیکن RSI نئی کم ترین سطح نہ بنائے۔ جبکہ "مخفی تیزی کا ڈائیورجنس" اس کے برعکس ہے: قیمت نئی کم ترین سطح نہ بنائے لیکن RSI نئی کم ترین سطح بنائے۔ ان دونوں میں "نئی کم" اور "نئی بلند" سے مراد ایک مخصوص متحرک ونڈو (Rolling Window) میں تاریخی انتہاؤں کے مقابلے ہیں۔

مزید برآں، یہ حکمت عملی طویل مدتی RSI (مثلاً 50 دن کا RSI) کو فلٹر کے طور پر بھی شامل کرتی ہے۔ صرف اس صورت میں خریداری کے سگنل پر غور کیا جاتا ہے جب طویل RSI 50 سے زیادہ ہو۔ اور جب طویل RSI 30 سے کم ہو تو نقصان کاٹنے (Stop Loss) یا منافع لینے (Take Profit) پر غور کیا جاتا ہے۔

حکمت عملی کے فوائد

اس حکمت عملی کا سب سے بڑا فائدہ یہ ہے کہ یہ مختصر مدت کے RSI کے ڈائیورجنس سگنلز اور طویل مدت کے RSI فلٹر کو بیک وقت استعمال کرتی ہے، جس سے کسی حد تک پھنسنے (Getting Trapped) اور موقع ہاتھ سے جانے (Missing Opportunities) سے بچا جا سکتا ہے۔ خاص طور پر اس کے درج ذیل فوائد ہیں:

- مختصر مدت کے RSI ڈائیورجنس سگنل قیمت میں الٹ جانے (Reversal) کے موقع کا پہلے سے اندازہ لگانے میں مدد دیتے ہیں، جس سے مارکیٹ کے اہم موڑ (Turning Points) کو بروقت پکڑا جا سکتا ہے۔

- طویل مدت کا RSI فلٹر غیر یقینی صورتحال میں بے جا خریداری سے بچاتا ہے۔

- مختلف اقسام کے منافع لینے (Take Profit) کے طریقے، خاص طور پر قسط وار منافع لینا (Partial Take Profit)، خطرے کو کم کرنے میں مددگار ہے۔

- پیرامائیڈنگ (Pyramiding) کا طریقہ کار اضافی سرمایہ کاری (Adding Positions) کی اجازت دیتا ہے، جس سے منافع کے امکانات مزید بڑھ جاتے ہیں۔

حکمت عملی کے خطرات

اس حکمت عملی میں کچھ خطرات بھی ہیں جن پر توجہ دینے کی ضرورت ہے:

- RSI کا ڈائیورجنس ہمیشہ درست نہیں ہوتا، بعض اوقات جھوٹے سگنل (False Signals) بھی آ سکتے ہیں۔

- سرمایہ کاری میں اضافہ (Adding Positions) کرنے سے خطرہ بڑھ جاتا ہے۔ اگر حکمت عملی غلط ثابت ہو تو نقصان تیزی سے بڑھ سکتا ہے۔

- منافع لینے (Take Profit) کی شرائط کا غلط تعین بھی قبل از وقت منافع لینے یا منافع کم ہونے کا باعث بن سکتا ہے۔

خطرات کے انتظام کے لیے مناسب اقدامات میں نقصان کاٹنے اور منافع لینے کی شرائط کو مناسب طریقے سے طے کرنا، ہر پوزیشن (Position) کے حجم کو کنٹرول کرنا، اور قسط وار پوزیشن کم کرنا (Partial Exit) شامل ہے، تاکہ منافع اور نقصان کا منحنی خط (P&L Curve) ہموار رہے۔

بہتری کے ممکنہ پہلو

اس حکمت عملی میں مزید بہتری کی گنجائش موجود ہے:

- RSI کے پیرامیٹرز کو مزید بہتر بنایا جا سکتا ہے تاکہ بہترین امتزاج (Optimal Combination) تلاش کیا جا سکے۔

- دوسرے انڈیکیٹرز جیسے MACD، KD وغیرہ کے ڈائیورجنس سگنلز کو بھی آزمایا جا سکتا ہے۔

- مخصوص مصنوعات (جیسے خام تیل (Crude Oil)، قیمتی دھاتیں (Precious Metals) وغیرہ) کے لیے پیرامیٹرز کو خاص طور پر بہتر بنایا جا سکتا ہے تاکہ ان کی مطابقت (Adaptability) بڑھائی جا سکے۔

خلاصہ

یہ حکمت عملی مختصر اور طویل مدتی RSI کے تیزی اور مندی کے ڈائیورجنس سگنلز کو یکجا کرتی ہے، جس سے خطرے کو کنٹرول کرنے کے ساتھ ساتھ منافع کی کارکردگی میں اضافہ ہوتا ہے۔ یہ مقداری تجارتی حکمت عملیوں (Quantitative Trading Strategies) کے ڈیزائن کے کئی اصولوں کو ظاہر کرتی ہے، جیسے کب داخل ہونا ہے، کب باہر نکلنا ہے، قسط وار پوزیشن بنانا اور کم کرنا، نقصان کاٹنے اور منافع لینے کی شرائط طے کرنا وغیرہ۔ یہ RSI ڈائیورجنس پر مبنی حکمت عملی کی ایک قابل تقلید مثال ہے۔

- 1