تیز اور سست EMA کا گولڈن کراس بریک آؤٹ حکمت عملی

جائزہ

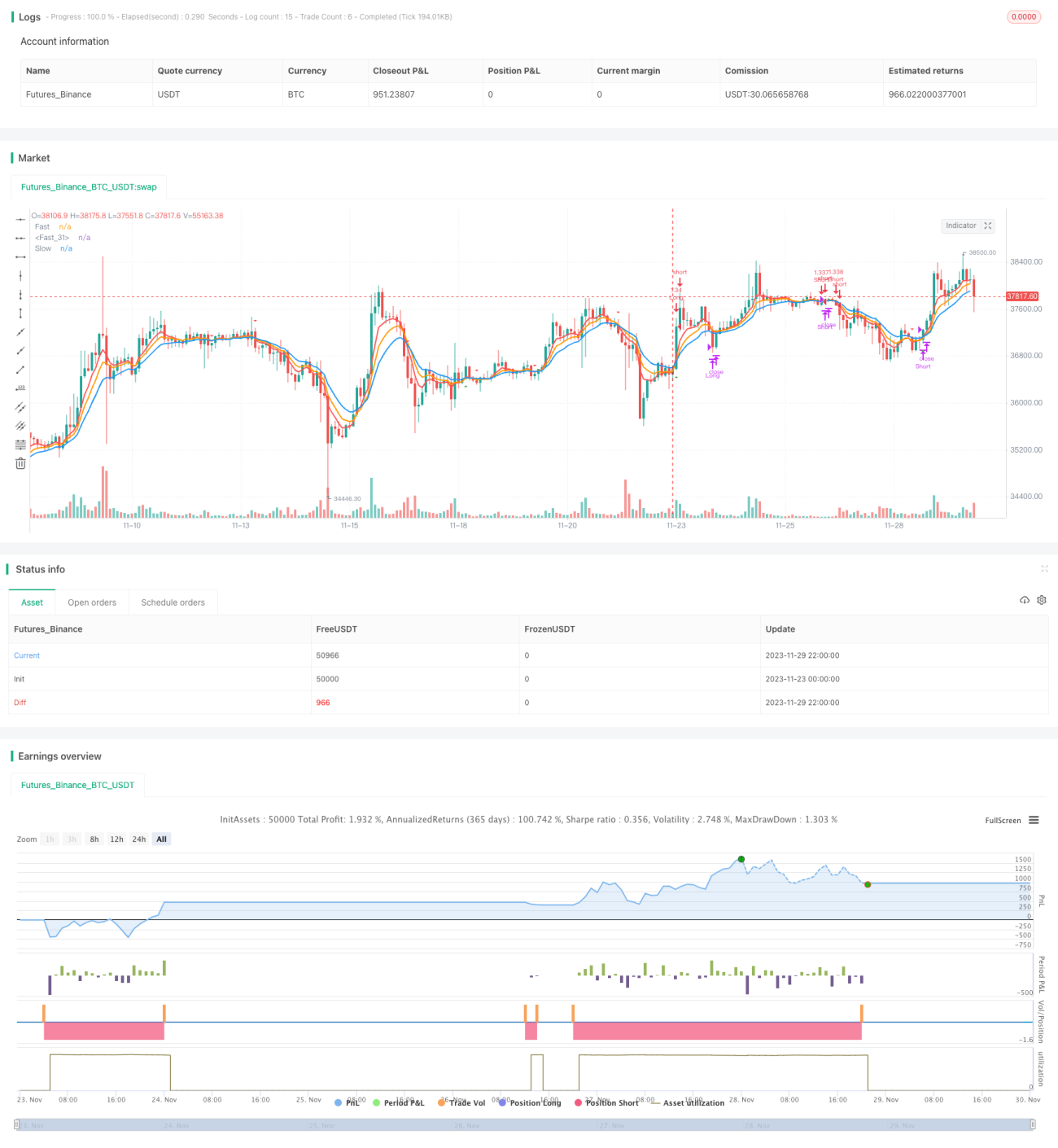

فاسٹ اینڈ سلو ای ایم اے (EMA) گولڈن کراس بریک آؤٹ حکمت عملی مارکیٹ کے رجحان کو ٹریک کرنے کا ایک سادہ اور مؤثر طریقہ ہے۔ یہ مختلف دورانیوں کے ای ایم اے (EMA) اوسطوں کے کراس اوور بریک آؤٹ کا استعمال کرتی ہے تاکہ خرید و فروخت کے سگنل تیار کیے جا سکیں۔ بنیادی خیال یہ ہے: جب مختصر دورانیے کا ای ایم اے طویل دورانیے کے ای ایم اے کو اوپر سے کراس کرتا ہے تو خرید کا سگنل پیدا ہوتا ہے؛ جب مختصر دورانیے کا ای ایم اے طویل دورانیے کے ای ایم اے کو نیچے سے کراس کرتا ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر 5، 8 اور 13 دورانیوں کے ای ایم اے (EMA) اوسطوں کا موازنہ کرکے تجارتی سگنل تیار کرتی ہے۔ اس میں شامل ہیں:

- 5 دورانیے کا ای ایم اے، 8 دورانیے کا ای ایم اے اور 13 دورانیے کا ای ایم اے شمار کریں۔

- جب 5 دورانیے کا ای ایم اے 8 اور 13 دورانیوں کے ای ایم اے کو اوپر سے کراس کرے تو خرید کا سگنل پیدا ہوگا۔

- جب 5 دورانیے کا ای ایم اے 8 اور 13 دورانیوں کے ای ایم اے کو نیچے سے کراس کرے تو فروخت کا سگنل پیدا ہوگا۔

- اس کے ساتھ ساتھ، ای ڈی ایکس (ADX) انڈیکیٹر کے ذریعے رجحان کی مضبوطی کا اندازہ لگایا جاتا ہے، اور صرف اس صورت میں سگنل پیدا ہوتا ہے جب رجحان کافی مضبوط ہو۔

اس طرح، یہ درمیانی تا طویل مدت کے رجحان کو ٹریک کرنے کا اثر پیدا کرتی ہے۔ جب مختصر مدت کی اوسط طویل مدت کی اوسط کو اوپر سے کراس کرتی ہے تو یہ ظاہر کرتا ہے کہ مختصر مدت کا رجحان تیزی کی طرف مڑ گیا ہے، لہذا خریدنا چاہیے؛ جب مختصر مدت کی اوسط طویل مدت کی اوسط کو نیچے سے کراس کرتی ہے تو یہ ظاہر کرتا ہے کہ مختصر مدت کا رجحان مندی کی طرف ہے، لہذا فروخت کرنا چاہیے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل اہم فوائد ہیں:

- عمل درآمد آسان اور آسانی سے قابل عمل ہے۔

- ای ایم اے اوسطوں کی ہموار کرنے کی خصوصیت سے بھرپور فائدہ اٹھاتا ہے، مؤثر طریقے سے رجحان کو ٹریک کرتا ہے۔

- متعدد ای ایم اے سیٹوں کا کراس اوور جھوٹے سگنلز سے بچاتا ہے۔

- ای ڈی ایکس (ADX) انڈیکیٹر کے ساتھ مل کر سگنلز کو زیادہ قابل اعتماد بناتا ہے۔

- ڈرا ڈاؤن اور زیادہ سے زیادہ نقصان زیادہ نہیں ہوتا۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی موجود ہیں:

- رجحان کی شدید تبدیلی پر، نقصان روکنے کی حد (Stop Loss) بڑی ہو سکتی ہے۔ اسٹاپ لاس کی حد کو مناسب طریقے سے بڑھایا جا سکتا ہے۔

- تجارتی تعدد نسبتاً زیادہ ہے، جس سے تجارتی اخراجات بڑھ سکتے ہیں۔ ای ایم اے کے پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کرکے تجارتی تعدد کو کم کیا جا سکتا ہے۔

بہتری کے راستے

اس حکمت عملی کو درج ذیل راستوں سے بہتر بنایا جا سکتا ہے:

- ای ایم اے کے پیرامیٹرز کو بہتر بنائیں، بہترین پیرامیٹر کا مجموعہ تلاش کریں۔

- دیگر انڈیکیٹرز جیسے کے ڈی جے (KDJ)، بولنگر بینڈز (BOLL) وغیرہ شامل کریں تاکہ سگنل کے معیار میں اضافہ ہو۔

- پوزیشن کے انتظام کو ایڈجسٹ کریں، خطرے کے کنٹرول کو بہتر بنائیں۔

- مشین لرننگ کے طریقوں کا استعمال کرتے ہوئے بہتر اندراج اور اخراج کے قواعد تلاش کریں۔

خلاصہ

مذکورہ بالا تمام باتوں کی روشنی میں، فاسٹ اینڈ سلو ای ایم اے گولڈن کراس بریک آؤٹ حکمت عملی مجموعی طور پر ہموار طریقے سے کام کرتی ہے، سگنل نسبتاً قابل اعتماد ہیں، ڈرا ڈاؤن زیادہ نہیں ہے، اور یہ درمیانی تا طویل مدت کے رجحان کو ٹریک کرنے کے لیے موزوں ہے۔ پیرامیٹرز کو بہتر بنانے اور قواعد کو مکمل کرنے سے بہتر حکمت عملی کے نتائج حاصل کیے جا سکتے ہیں۔

- 1