TFO اور ATR پر مبنی ٹرینڈ فالوونگ اسٹاپ لاس حکمت عملی

جائزہ

یہ حکمت عملی ڈاکٹر جان ایہلرز کے رجحان لچک دار آسیلیٹر (Trend Flex Oscillator, TFO) اور اوسط حقیقی حد (Average True Range, ATR) کے اشارے پر مبنی ایک رجحان کی پیروی کرنے والی اسٹاپ لاس حکمت عملی ہے۔ یہ طویل بازاروں کے لیے موزوں ہے، جب زیادہ فروخت ہونے کے بعد قیمت میں الٹ پلٹ ہوتی ہے تو طویل پوزیشن کھولتا ہے۔ یہ عام طور پر چند دنوں میں پوزیشن بند کر دیتا ہے، جب تک کہ وہ ریچھ کے بازار میں نہ پھنس جائے، ایسی صورت میں یہ پوزیشن پر قائم رہتا ہے۔ یہ حکمت عملی سادہ بیک ٹیسٹنگ کے ذریعے قابل ترتیب پیرامیٹرز کو ایڈجسٹ کرتی ہے، لیکن بیک ٹیسٹنگ کے نتائج پر مکمل اعتماد نہیں کرنا چاہیے۔

حکمت عملی کا اصول

یہ حکمت عملی TFO اور ATR دونوں اشاروں کو یکجا کرتی ہے، خریداری کی شرائط پوری ہونے پر طویل پوزیشن کھولتی ہے، اور فروخت کی شرائط پوری ہونے پر پوزیشن بند کرتی ہے۔

خریداری کی شرط: جب TFO ایک خاص حد سے نیچے ہو (زیادہ فروخت ہونے کی نشاندہی کرتا ہے)، اور پچھلی کندل کا TFO قدر موجودہ کندل سے کم ہو (TFO کے الٹ پلٹ کر بڑھنے کی نشاندہی کرتا ہے)، اور اسی وقت ATR مقرر کردہ اتار چڑھاؤ کی حد سے اوپر ہو (مارکیٹ میں اتار چڑھاؤ بڑھنے کی نشاندہی کرتا ہے)، تو ان تین شرائط کے پورا ہونے پر طویل پوزیشن کھولی جاتی ہے۔

پوزیشن بند کرنے کی شرط: جب TFO ایک خاص حد سے اوپر ہو (زیادہ خریداری کی نشاندہی کرتا ہے)، اور اسی وقت ATR مقرر کردہ حد سے اوپر ہو، تو شرط پوری ہونے پر تمام طویل پوزیشنیں بند کر دی جاتی ہیں۔ اس کے علاوہ، یہ حکمت عملی ایک ٹریلنگ اسٹاپ لاس بھی مقرر کرتی ہے، جب قیمت مقرر کردہ ٹریلنگ اسٹاپ لاس کی سطح سے نیچے آ جاتی ہے، تو بھی تمام طویل پوزیشنیں بند کر دی جاتی ہیں۔ صارف یہ انتخاب کر سکتا ہے کہ حکمت عملی اشارے کے سگنلز کے مطابق پوزیشن بند کرے، یا صرف اسٹاپ لاس کی قیمت کے مطابق بند کرے۔

یہ حکمت عملی ایک وقت میں زیادہ سے زیادہ 15 طویل پوزیشنیں کھول سکتی ہے۔ اس کے پیرامیٹرز کو ایڈجسٹ کیا جا سکتا ہے، اور یہ مختلف وقت کے ادوار کے لیے موزوں ہے۔

حکمت عملی کے فوائد

-

رجحان اور اتار چڑھاؤ کو ملا کر مارکیٹ کی سمت کا فیصلہ کرنا، نسبتاً مستحکم ہے۔ TFO رجحان میں بریک آؤٹ کے ابتدائی سگنلز کو پکڑ سکتا ہے، جبکہ ATR مارکیٹ میں بڑھتے ہوئے اتار چڑھاؤ کے مواقع کو سمجھ سکتا ہے۔

-

قابل ایڈجسٹ خرید و فروخت کے پیرامیٹرز اور اسٹاپ لاس پیرامیٹرز مرتب کیے گئے ہیں، جس سے عمل میں لچک آتی ہے۔ صارف مارکیٹ کے مطابق پیرامیٹرز کو ایڈجسٹ کر کے زیادہ سے زیادہ اصلاح حاصل کر سکتا ہے۔

-

اسٹاپ لاس کی خصوصیت شامل ہے، جو انتہائی مارکیٹ کی صورت حال میں نقصان کو کم کر سکتی ہے۔ اسٹاپ لاس حکمت عملی مقداری تجارت میں ایک بہت اہم جزو ہے۔

-

اضافی پوزیشن کھولنے اور جزوی پوزیشن بند کرنے کی حمایت کرتا ہے، جس سے پوزیشن کے سائز کو بڑھا کر منافع کو بڑھایا جا سکتا ہے۔ یہ تیزی والی مارکیٹ کے لیے موزوں ہے۔

حکمت عملی کے خطرات

-

یہ حکمت عملی صرف طویل پوزیشنیں لیتی ہے، مختصر پوزیشنیں نہیں لیتی، لہذا مندی والی مارکیٹ میں منافع نہیں کما سکتی۔ اگر شدید ریچھ کی مارکیٹ آئے تو بھاری نقصان ہو سکتا ہے۔

-

پیرامیٹرز کی غلط ترتیب سے زیادہ تجارت یا خرید و فروخت چھوٹنے کا سبب بن سکتا ہے۔ بہترین پیرامیٹرز کا مجموعہ تلاش کرنے کے لیے بار بار جانچ کی ضرورت ہے۔

-

انتہائی مارکیٹ کی صورت حال میں، اسٹاپ لاس غیر موثر ہو سکتا ہے، اور بھاری نقصان کو روکنے میں ناکام ہو سکتا ہے۔ یہ وہ مسئلہ ہے جس کا سامنا تمام اسٹاپ لاس حکمت عملیوں کو ہو سکتا ہے۔

-

بیک ٹیسٹنگ حقیقی تجارت کی صورت حال کو مکمل طور پر ظاہر نہیں کر سکتی، حقیقی نتائج اس سے کچھ انحراف کر سکتے ہیں۔

حکمت عملی کی اصلاح

-

فروخت کی شرط میں ٹریلنگ اسٹاپ لاس لائن شامل کرنے پر غور کیا جا سکتا ہے، تاکہ حکمت عملی بروقت اسٹاپ لاس لگا سکے اور نیچے کی جانب خطرے کو مؤثر طریقے سے کنٹرول کر سکے۔

-

مختصر پوزیشن لینے کے طریقہ کار کو بڑھایا جا سکتا ہے، جب TFO الٹ پلٹ کر نیچے آئے اور ATR کافی بڑا ہو تو مختصر پوزیشن کھولی جا سکتی ہے، تاکہ حکمت عملی مندی والی مارکیٹ پر بھی لاگو ہو سکے۔

-

مزید فلٹرنگ شرائط شامل کی جا سکتی ہیں، جیسے حجم میں تبدیلی، تاکہ غیر معمولی مارکیٹ کی صورت حال کا حکمت عملی پر اثر کم ہو۔

-

مختلف وقت کے ادوار کے پیرامیٹر سیٹنگز اور بیک ٹیسٹنگ کے نتائج کی جانچ کی جا سکتی ہے، تاکہ بہترین دورانیہ اور پیرامیٹرز کا مجموعہ تلاش کیا جا سکے۔

خلاصہ

یہ حکمت عملی رجحان کے تجزیہ اور اتار چڑھاؤ کی نگرانی کے فوائد کو یکجا کرتی ہے، TFO اور ATR کے اشاروں کے امتزاج کے ذریعے مارکیٹ کی سمت کا فیصلہ کرتی ہے۔ اس میں اضافی پوزیشن کھولنے، جزوی پوزیشن بند کرنے، ٹریلنگ اسٹاپ لاس جیسے طریقہ کار شامل ہیں، جو منافع کو بڑھانے اور خطرے کو کنٹرول کرنے میں مدد دیتے ہیں، اور تیزی والی مارکیٹ کے لیے موزوں ہے۔ اس میں توسیع پذیر اصلاح کی گنجائش بھی ہے، مزید اشاروں کے فلٹرز اور پیرامیٹر ٹیوننگ کے ذریعے حکمت عملی کی کارکردگی کو مزید بہتر بنایا جا سکتا ہے۔ یہ بنیادی طور پر ایک مقداری حکمت عملی کی بنیادی ضروریات کو پورا کرتی ہے، اور گہرائی سے تحقیق اور استعمال کے قابل ہے۔

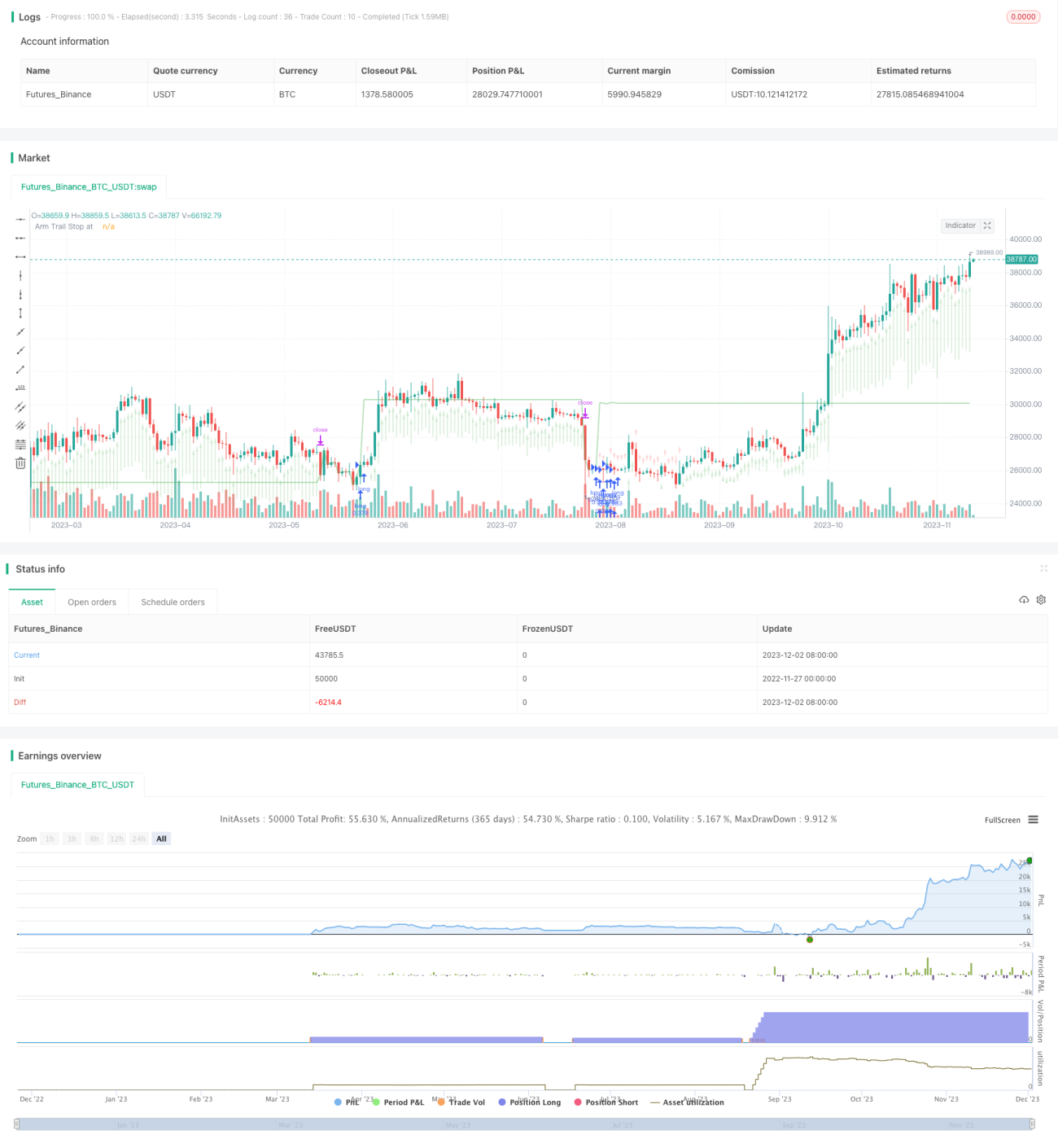

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1