کثیر عنصر RSI ریورسل حکمت عملی

جائزہ

یہ حکمت عملی RSI انڈیکیٹر کا استعمال کرتے ہوئے اوور باؤٹ اور اوور سیلڈ حالات کی نشاندہی کرتی ہے، اور MACD، Stochastic جیسے متعدد معاون عوامل کے ساتھ داخل ہوتی ہے۔ یہ حکمت عملی مختصر مدت کے ریورسل مواقع کو حاصل کرنے کے لیے بنائی گئی ہے اور یہ ایک ریورسل حکمت عملی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر RSI انڈیکیٹر کا استعمال کرتے ہوئے مارکیٹ کے اوور باؤٹ یا اوور سیلڈ ہونے کا اندازہ لگاتی ہے۔ جب RSI انڈیکیٹر مقرر کردہ اوور باؤٹ لائن سے زیادہ ہو جاتا ہے، تو اس کا مطلب ہے کہ مارکیٹ اوور باؤٹ حالت میں ہو سکتی ہے، اس صورت میں حکمت عملی شارٹ پوزیشن لینے کا انتخاب کرتی ہے۔ جب RSI انڈیکیٹر مقرر کردہ اوور سیلڈ لائن سے کم ہو جاتا ہے، تو اس کا مطلب ہے کہ مارکیٹ اوور سیلڈ حالت میں ہو سکتی ہے، اس صورت میں حکمت عملی لانگ پوزیشن لینے کا انتخاب کرتی ہے۔ اس طرح، مارکیٹ کے ایک انتہائی حالت سے دوسری انتہائی حالت میں تبدیل ہونے کے دوران پیدا ہونے والے مختصر مدت کے تجارتی مواقع کو حاصل کرکے منافع کمایا جاتا ہے۔

اس کے علاوہ، حکمت عملی میں MACD، Stochastic جیسے متعدد معاون عوامل بھی شامل کیے گئے ہیں۔ ان معاون عوامل کا مقصد کچھ ممکنہ جھوٹے مثبت تجارتی سگنلز کو فلٹر کرنا ہے۔ جب RSI انڈیکیٹر سگنل جاری کرتا ہے اور معاون عوامل بھی اس سگنل کی حمایت کرتے ہیں، تب ہی حکمت عملی حقیقی تجارتی کارروائی کرتی ہے۔ یہ کثیر عنصری تعاون حکمت عملی کے سگنلز کی قابل اعتمادی کو بڑھاتا ہے، جس سے حکمت عملی کے استحکام میں بھی اضافہ ہوتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کا سب سے بڑا فائدہ اس کی اعلیٰ گرفتاری کی کارکردگی ہے، اور کثیر عنصری تصدیق کی بدولت سگنل کے معیار میں بہتری آئی ہے۔ خاص طور پر، یہ درج ذیل پہلوؤں میں ظاہر ہوتا ہے:

- RSI انڈیکیٹر خود مارکیٹ کے رجیمز کی شناخت کی مضبوط صلاحیت رکھتا ہے، اور یہ اوور باؤٹ اور اوور سیلڈ حالات کو مؤثر طریقے سے پہچان سکتا ہے۔

- متعدد معاون ٹولز کے ذریعے کثیر عنصری تصدیق سے سگنل کے معیار میں بہتری آئی ہے، اور بہت سے جھوٹے مثبت سگنلز کو فلٹر کیا گیا ہے۔

- حکمت عملی پیرامیٹرز کے لیے حساس نہیں ہے، جس سے اسے بہتر بنانا آسان ہے۔

خطرات اور حل

اس حکمت عملی کو کچھ خطرات کا بھی سامنا ہے، جو بنیادی طور پر دو پہلوؤں میں مرکوز ہیں:

- ریورسل کی ناکامی کا خطرہ۔ ریورسل سگنل خود شماریاتی اربیٹریج مواقع پر انحصار کرتا ہے، اور کچھ ریورسلز کی ناکامی کے امکان کو رد نہیں کیا جا سکتا۔ پوزیشن کا سائز کم کرکے یا اسٹاپ لاس لگا کر رسک کو کنٹرول کیا جا سکتا ہے۔

- تیزی والی مارکیٹ میں نقصان کا خطرہ۔ حکمت عملی مجموعی طور پر اب بھی مارکیٹ کے مخالف سمت میں کام کرتی ہے، اور تیزی والی مارکیٹ میں کچھ نقصان ہونا لازمی ہے۔ اس کے لیے ہمیں بڑے رجحان کا درست اندازہ لگانے کی ضرورت ہے، اور جب ضروری ہو تو انسانی مداخلت کے ذریعے ناموافق مارکیٹ کے حالات کو چھوڑ دیں۔

بہتری کے راستے

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنانے کی ضرورت ہے:

- مختلف مصنوعات کی جانچ کریں اور پیرامیٹرز کا بہترین مجموعہ تلاش کریں۔ حکمت عملی پیرامیٹرز کے لیے حساس نہیں ہے، لیکن پھر بھی مختلف مصنوعات کے لیے بہترین پیرامیٹرز تلاش کرنے کی سفارش کی جاتی ہے۔

- خودکار اخراج کا طریقہ کار شامل کریں۔ متحرک اسٹاپ لاس، وقت پر اخراج وغیرہ کے طریقوں کی جانچ کی جا سکتی ہے تاکہ حکمت عملی مارکیٹ کی تبدیلیوں کے ساتھ بہتر طور پر ہم آہنگ ہو سکے۔

- مشین لرننگ الگورتھم متعارف کروائیں۔ ماڈل کو ریورسل کی کامیابی کے امکان کا اندازہ لگانا سکھانے کی کوشش کی جا سکتی ہے، جس سے حکمت عملی کی جیت کی شرح میں اضافہ ہو سکتا ہے۔

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک مختصر مدت کی ریورسل حکمت عملی ہے۔ یہ RSI انڈیکیٹر کی اوور باؤٹ اور اوور سیلڈ شناخت کرنے کی صلاحیت کا استعمال کرتی ہے، اور ساتھ ہی متعدد معاون ٹولز کے ذریعے کثیر عنصری تصدیق کرتی ہے، جس سے سگنل کے معیار میں بہتری آتی ہے۔ اس حکمت عملی کی گرفتاری کی کارکردگی اعلیٰ ہے اور استحکام بھی اچھا ہے۔ یہ مزید جانچ اور بہتری کے قابل ہے، اور بالآخر منافع حاصل کرنے کے قابل ہے۔

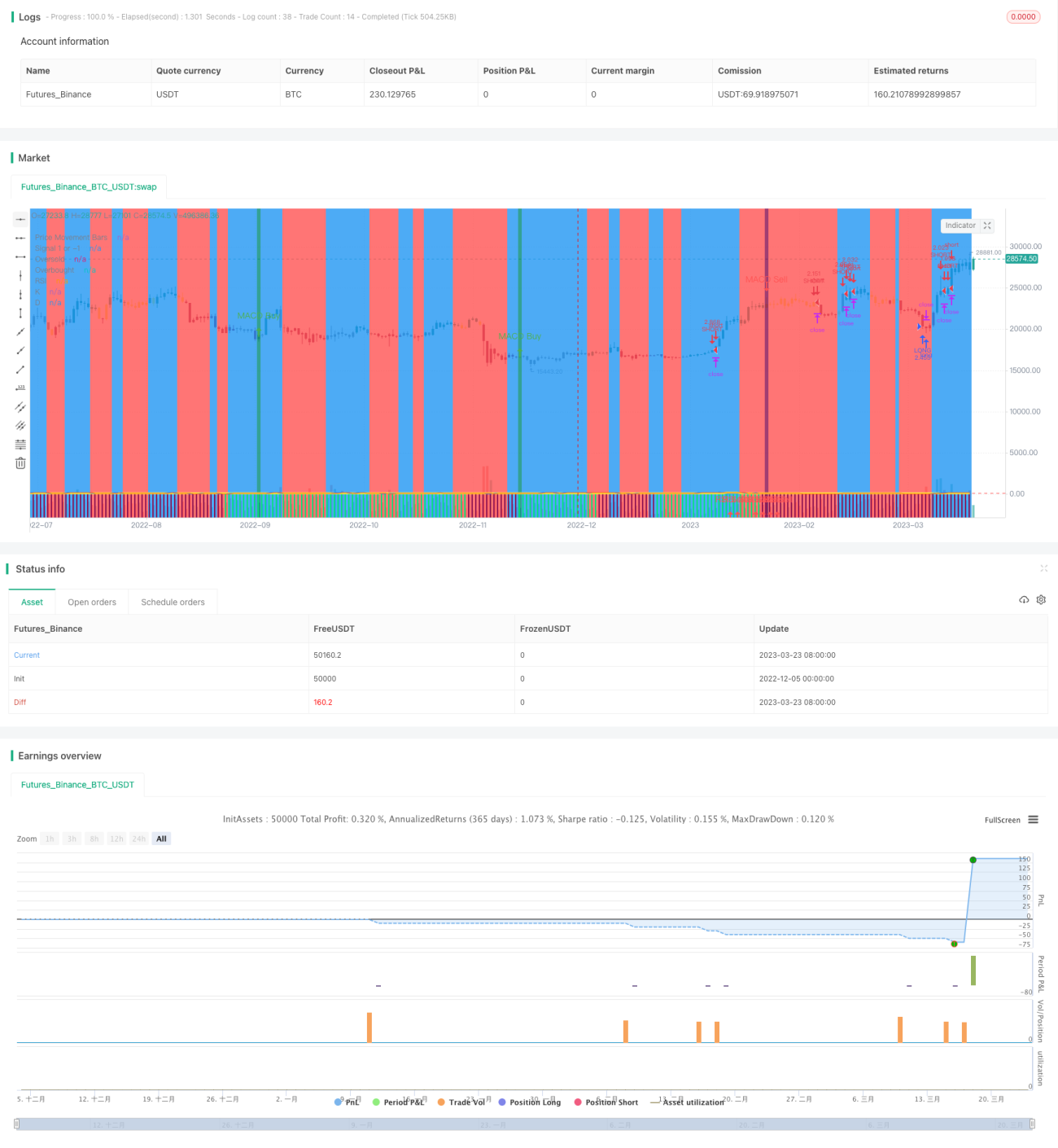

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1