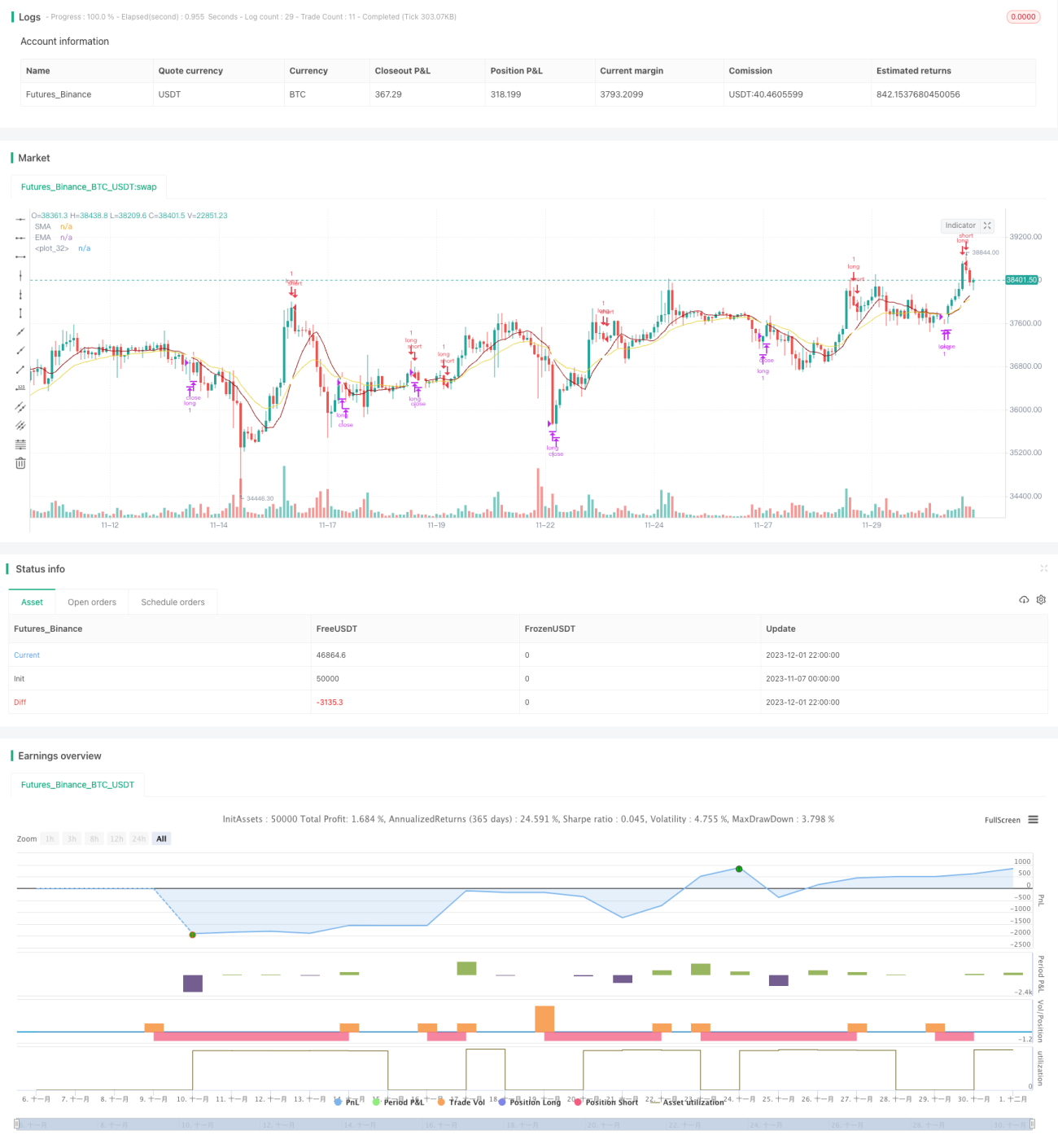

SMA، EMA اور حجم پر مبنی ایک سادہ مومنٹم حکمت عملی

جائزہ

یہ حکمت عملی ایک سادہ دن کی رفتار کی حکمت عملی ہے جو صرف لمبی پوزیشن لیتی ہے (صرف تیزی، مندی نہیں)۔ یہ SMA، EMA اور حجم کے اشارے استعمال کرتی ہے تاکہ بہترین وقت پر (یعنی جب قیمت اور رفتار دونوں بڑھ رہے ہوں) مارکیٹ میں داخل ہو سکے۔ اس کا فائدہ یہ ہے کہ یہ سادہ ہے اور رجحان کو کسی حد تک پہچاننے کی صلاحیت رکھتی ہے۔

حکمت عملی کا اصول

اس حکمت عملی کے Entry سگنل پیدا کرنے کی منطق یہ ہے: جب SMA اشارے EMA اشارے سے اوپر ہو اور مسلسل 3 یا 4 K-لائنوں میں اضافے کا رجحان ہو، اور درمیانی K-لائن کی کم ترین قیمت اضافے کی شروعاتی K-لائن کی افتتاحی قیمت سے زیادہ ہو، تو Entry سگنل پیدا ہوتا ہے۔

Exit سگنل پیدا کرنے کی منطق یہ ہے: جب SMA اشارے EMA اشارے سے نیچے آ جائے تو Exit سگنل پیدا ہوتا ہے۔

یہ حکمت عملی صرف لمبی پوزیشنیں لیتی ہے، مندی نہیں۔ اس کی Entry اور Exit منطق مسلسل بڑھتے ہوئے رجحان کو کسی حد تک پہچاننے کی صلاحیت رکھتی ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- حکمت عملی کی منطق سادہ، سمجھنے اور لاگو کرنے میں آسان ہے؛

- یہ SMA، EMA اور حجم جیسے عام تکنیکی اشارے استعمال کرتی ہے، پیرامیٹرز کو لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے؛

- مسلسل بڑھتے ہوئے رجحان کو کسی حد تک پہچاننے کی صلاحیت رکھتی ہے، رجحان کے کچھ مواقع کو پکڑ سکتی ہے۔

خطرات کا تجزیہ

اس حکمت عملی میں درج ذیل خطرات بھی ہیں:

- نیچے کی طرف یا سائیڈ ویز مارکیٹ کو پہچاننے سے قاصر، جس کی وجہ سے بڑی واپسی ہو سکتی ہے؛

- منافع کے مواقع استعمال نہیں کر سکتی، زوال پذیر رجحان کے خلاف ہیج نہیں کر سکتی، ممکنہ طور پر بہتر منافع کے مواقع سے محروم ہو سکتی ہے؛

- حجم کا اشارے اعلی تعدد والے ڈیٹا پر اچھی کارکردگی نہیں دکھاتا، پیرامیٹرز کو ایڈجسٹ کرنے کی ضرورت ہے؛

- نقصان روکنے والے (Stop Loss) کا استعمال کر کے خطرے کو کنٹرول کیا جا سکتا ہے۔

بہتری کے امکانات

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- مندی کے مواقع بڑھائیں، دو طرفہ (لمبی اور چھوٹی) تجارت کو نافذ کریں، زوال پذیر رجحان سے فائدہ اٹھائیں؛

- زیادہ جدید اشارے جیسے MACD، RSI وغیرہ کے مجموعے والی حکمت عملی استعمال کریں، رجحان کی تشخیص کی صلاحیت بہتر بنائیں؛

- نقصان روکنے کی منطق کو بہتر بنائیں، واپسی کے خطرے کو کم کریں؛

- پیرامیٹرز کو ایڈجسٹ کریں، مختلف ادوار کے ڈیٹا کا تجربہ کریں، بہترین پیرامیٹر مجموعہ تلاش کریں۔

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک بہت سادہ رجحان کی پیروی کرنے والی حکمت عملی ہے جو SMA، EMA اور حجم کے اشارے کے ذریعے داخلے کے وقت کا تعین کرتی ہے۔ اس کا فائدہ سادگی اور آسانی سے لاگو ہونا ہے، جو ابتدائی سیکھنے کے لیے موزوں ہے، لیکن یہ سائیڈ ویز اور نیچے کی طرف کے رجحان کو پہچان نہیں سکتی، اس میں کچھ خطرہ ہے۔ مندی کی پوزیشنیں متعارف کروا کر، اشاروں کو بہتر بنا کر اور نقصان روکنے کے استعمال کے ذریعے اسے بہتر بنایا جا سکتا ہے۔

- 1