قیمت میں تبدیلی کی شرح اور حرکت پذیر اوسط پر مبنی مقداری حکمت عملی

جائزہ

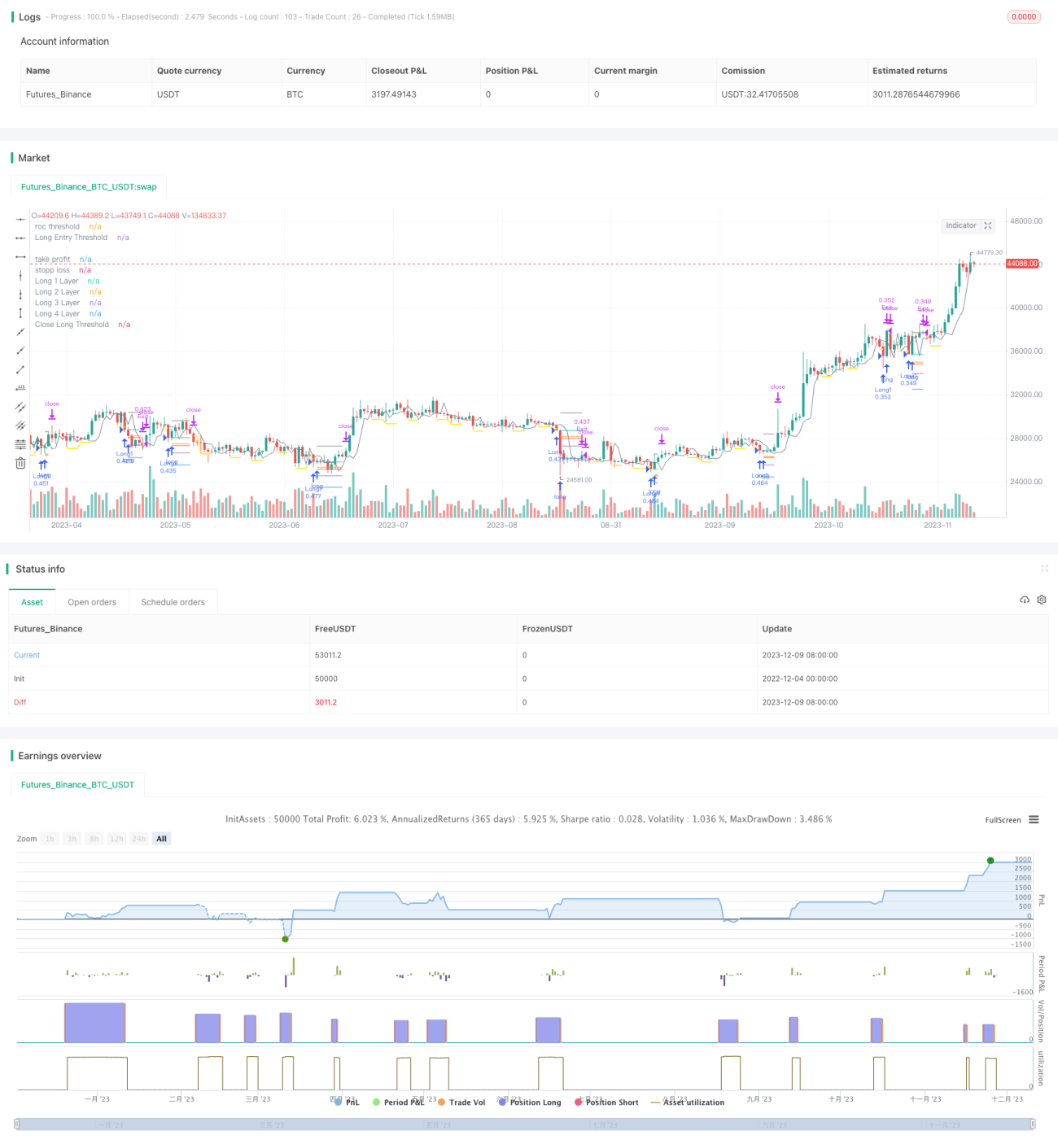

یہ حکمت عملی قیمت کی تبدیلی کی شرح اور متحرک اوسط کے تکنیکی اشاریوں کو ملا کر خرید و فروخت کے نکات کی درست نشاندہی کرتی ہے۔ جب قیمت میں واضح کمی ہوتی ہے تو خرید کی حد مقرر کی جاتی ہے اور مزید کمی پر لمبی پوزیشن کھولی جاتی ہے؛ جب قیمت میں اضافہ ہوتا ہے تو فروخت کی حد مقرر کی جاتی ہے اور مزید اضافے پر پوزیشن بند کی جاتی ہے۔ اس کے ساتھ ساتھ، حکمت عملی میں پوزیشن میں اضافے کا طریقہ بھی استعمال کیا جاتا ہے، متعدد بار خرید کر لاگت کم کی جاتی ہے۔

حکمت عملی کے اصول

خریداری کی منطق

- قیمت کی تبدیلی کی شرح (ROC) کا حساب لگائیں اور خرید کی حد کی لکیر مقرر کریں۔

- جب قیمت خرید کی حد کی لکیر سے نیچے ٹوٹتی ہے، تو اس نقطہ کو ریکارڈ کریں اور خرید کی محدود لکیر کو فعال کریں۔

- خرید کی محدود لکیر ان پٹ پیرامیٹرز کے مطابق مدت مقرر کرتی ہے، مدت ختم ہونے پر بند ہو جاتی ہے۔

- جب قیمت مزید گرتی ہے اور خرید کی محدود لکیر سے نیچے ٹوٹتی ہے، تو پہلی لمبی پوزیشن کھولیں۔

فروخت کی منطق

- قیمت کی تبدیلی کی شرح (ROC) کا حساب لگائیں اور فروخت کی حد کی لکیر مقرر کریں۔

- جب قیمت فروخت کی حد کی لکیر سے اوپر ٹوٹتی ہے، تو اس نقطہ کو ریکارڈ کریں اور فروخت کی محدود لکیر کو فعال کریں۔

- فروخت کی محدود لکیر ان پٹ پیرامیٹرز کے مطابق مدت مقرر کرتی ہے، مدت ختم ہونے پر بند ہو جاتی ہے۔

- جب قیمت مزید بڑھتی ہے اور فروخت کی محدود لکیر سے اوپر ٹوٹتی ہے، تو تمام لمبی پوزیشنیں بند کریں۔

خطرے کا کنٹرول

حکمت عملی میں نقصان روکنے اور منافع روکنے کے بلٹ ان فنکشنز ہیں، پیرامیٹرز کو اپنی مرضی کے مطابق ترتیب دیا جا سکتا ہے، اور موجودہ پوزیشنوں کے خطرے کو حقیقی وقت میں کنٹرول کیا جا سکتا ہے۔

پوزیشن میں اضافے کا طریقہ

ہر تجارتی پوزیشن کھولتے وقت، ان پٹ پیرامیٹرز کے مطابق ایک خاص تناسب میں بعد کی خریداری کی قیمت مقرر کریں، تاکہ قسطوں میں خرید کر پوزیشن میں اضافے کا اثر حاصل ہو۔

فوائد کا تجزیہ

- قیمت کی تبدیلی کی شرح کے اشاریہ ROC کا استعمال کرتے ہوئے خرید و فروخت کے نکات تلاش کریں، ROC قیمت کی تبدیلی پر بہت حساس ہے، خرید و فروخت کے نکات کی درست نشاندہی کرتا ہے۔

- محدود لکیر کا طریقہ استعمال کرتے ہوئے خرید و فروخت کے وقت کی مزید تصدیق کریں، جھوٹے بریک آؤٹ سے بچیں۔

- پوزیشن میں اضافے کا طریقہ خطرے کو قابو میں رکھتے ہوئے مارکیٹ کی قدر کی پیروی کر سکتا ہے۔

- بلٹ ان نقصان روکنے اور منافع روکنے کے فنکشنز ایک پوزیشن کے خطرے کو سختی سے کنٹرول کرتے ہیں۔

خطرات اور حل

- جب مارکیٹ میں شدید اتار چڑھاؤ ہوتا ہے، تو حکمت عملی بہت زیادہ پوزیشنیں کھول سکتی ہے۔ حل یہ ہے کہ پوزیشن میں اضافے کے پیرامیٹرز کو مناسب طریقے سے ترتیب دیا جائے اور پوزیشنوں کی کل تعداد کو کنٹرول کیا جائے۔

- جب قیمت کی حرکت کی سمت واضح نہ ہو، تو نقصان روکنے یا منافع روکنے کی قیمتیں بار بار متحرک ہو سکتی ہیں۔ مناسب طور پر نقصان اور منافع کی حدوں کو وسیع کیا جا سکتا ہے، یا اس فنکشن کو بند کیا جا سکتا ہے۔

بہتری کی تجاویز

- دیگر اشاریوں کے ساتھ ملا کر داخلے کے وقت کو فلٹر کریں۔ مثلاً، متحرک اوسط کے ساتھ، صرف اس وقت ROC اشاریہ پر بھروسہ کریں جب قیمت متحرک اوسط سے نیچے ٹوٹے۔

- پوزیشن میں اضافے کی منطق کو بہتر بنائیں، صرف مخصوص شرائط پوری ہونے پر اضافہ شروع کریں۔ مثلاً، صرف اس وقت مزید اضافہ کریں جب قیمت دوبارہ ایک خاص حد سے زیادہ گرے۔

- مختلف آلات کے پیرامیٹر کی ترتیبات میں کافی فرق ہو سکتا ہے، بہترین پیرامیٹر مجموعہ حاصل کرنے کے لیے مکمل بیک ٹیسٹنگ اور نقلی لائیو ٹریڈنگ کی ضرورت ہے۔

- انکولی نقصان اور منافع روکنے کو ترتیب دیا جا سکتا ہے، مارکیٹ کے اتار چڑھاؤ کی بنیاد پر مختلف نقصان کی حدیں مقرر کریں۔

خلاصہ

یہ حکمت عملی ROC اشاریہ کو خرید و فروخت کے نکات کی درست نشاندہی کے لیے، محدود لکیر کے طریقہ کار کو سگنلز کو فلٹر کرنے کے لیے، بلٹ ان نقصان اور منافع روکنے کو خطرے سے بچاؤ کے لیے، اور پوزیشن میں اضافے کے ذریعے منافع بڑھانے کے لیے یکجا کرتی ہے۔ مناسب پیرامیٹر ترتیبات کے تحت، خطرے کو قابو میں رکھتے ہوئے اضافی منافع حاصل کیا جا سکتا ہے۔ مستقبل میں سگنل فلٹرنگ اور رسک مینجمنٹ میکانزم کو مزید بہتر بنا کر حکمت عملی کو زیادہ مارکیٹ حالات کے مطابق ڈھالا جا سکتا ہے۔

- 1