TRSI اور SUPER Trend اشاریوں پر مبنی مقداری تجارتی حکمت عملی

جائزہ

یہ حکمت عملی نسبتاً مضبوط اشاریہ (TRSI) اور سپر ٹرینڈ انڈیکیٹر (SUPER Trend) کو ملا کر ایک مکمل مقداری تجارتی حکمت عملی تشکیل دیتی ہے۔ یہ حکمت عملی بنیادی طور پر درمیانی سے طویل مدتی رجحانات کو پکڑنے کے لیے استعمال ہوتی ہے، جبکہ مختصر مدتی اشاریوں کی مدد سے شور والے تجارتی سگنلز کو فلٹر کیا جاتا ہے۔

حکمت عملی کا اصول

- TRSI انڈیکیٹر کا حساب لگا کر مارکیٹ کی اوسط خرید و فروخت کی حالت کا تعین کیا جاتا ہے، جس سے خرید و فروخت کے سگنل ملتے ہیں۔

- SUPER Trend انڈیکیٹر کا استعمال شور والے سگنلز کو فلٹر کرنے اور بنیادی رجحان کی تصدیق کرنے کے لیے کیا جاتا ہے۔

- منافع بخش پوزیشنوں کے مختلف مراحل میں اسٹاپ لاس اور ٹیک پرافٹ پوائنٹس مقرر کیے جاتے ہیں۔

خاص طور پر، حکمت عملی پہلے TRSI انڈیکیٹر کا حساب لگاتی ہے تاکہ یہ معلوم کیا جا سکے کہ آیا مارکیٹ میں فروخت کا زون موجود ہے، پھر SUPER Trend انڈیکیٹر کا حساب لگا کر بڑے رجحان کی سمت کا تعین کرتی ہے۔ دونوں کو ملا کر تجارتی سگنل جاری کیے جاتے ہیں۔ اس کے بعد مختلف مراحل میں منافع کی واپسی کے مختلف تناسب کے ساتھ اسٹاپ لاس اور ٹیک پرافٹ پوائنٹس مقرر کیے جاتے ہیں۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- متعدد اشاریوں کا مجموعہ، جس سے سگنل کی درستگی بڑھ جاتی ہے۔ TRSI وقت کا تعین کرتا ہے، جبکہ SUPER Trend سمت کو فلٹر کرتا ہے۔

- درمیانی سے طویل مدتی رجحانات کی تجارت کے لیے موزوں ہے۔ اوسط خرید و فروخت کے سگنل اکثر رجحان کی تبدیلی کا باعث بنتے ہیں۔

- اسٹاپ لاس اور ٹیک پرافٹ کی مناسب ترتیب، مختلف مراحل میں منافع کی واپسی کے مختلف تناسب سے سرمائے کا مؤثر کنٹرول۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- درمیانی سے طویل مدتی تجارت، مختصر مدتی تجارتی مواقعوں کو پکڑنے سے قاصر۔

- TRSI پیرامیٹرز کی غلط ترتیب سے اوسط خرید و فروخت کے زون چھوٹ سکتے ہیں۔

- SUPER Trend پیرامیٹرز کی غلط ترتیب سے غلط سگنل جاری ہو سکتے ہیں۔

- اسٹاپ لاس کی حد بہت بڑی ہونے سے خطرے پر مؤثر کنٹرول نہیں ہو پاتا۔

ان خطرات سے نمٹنے کے لیے، ہم درج ذیل پہلوؤں سے اصلاح کر سکتے ہیں:

اصلاح کی سمتیں

- مزید مختصر مدتی اشاریوں کو شامل کرکے زیادہ تجارتی مواقعوں کی نشاندہی۔

- TRSI پیرامیٹرز کو ایڈجسٹ کرکے غلطی کے زون کو کم کرنا۔

- SUPER Trend پیرامیٹرز کی جانچ اور اصلاح۔

- فلوٹنگ اسٹاپ لاس کا تعین، جو حقیقی وقت میں اسٹاپ لاس لائن کو ٹریک کرے۔

خلاصہ

یہ حکمت عملی TRSI اور SUPER Trend جیسے متعدد اشاریوں کو یکجا کرکے ایک مکمل مقداری تجارتی حکمت عملی تشکیل دیتی ہے۔ یہ درمیانی سے طویل مدتی رجحانات کو مؤثر طریقے سے پہچان سکتی ہے، جبکہ اسٹاپ لاس اور ٹیک پرافٹ کے ذریعے خطرے کو کنٹرول کرتی ہے۔ حکمت عملی میں ابھی بہت گنجائش ہے، آئندہ سگنل کی درستگی بڑھانے، زیادہ تجارتی مواقعوں کی نشاندہی وغیرہ کے ذریعے بہتری لائی جا سکتی ہے۔ مجموعی طور پر، یہ ایک اچھا مقداری حکمت عملی کا نقطہ آغاز ہے۔

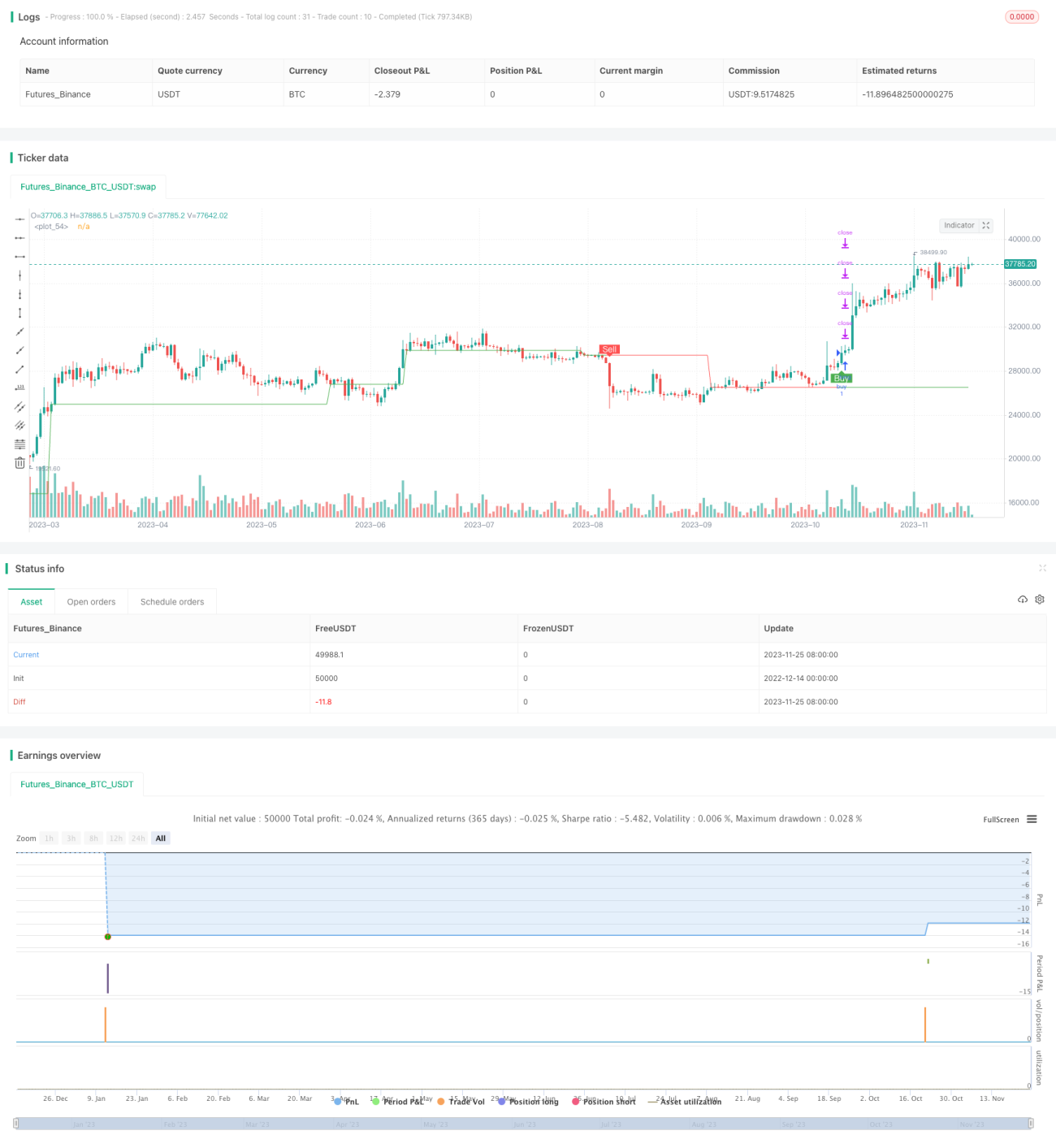

/*backtest

start: 2022-12-14 00:00:00

end: 2023-11-26 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "SuperTREX strategy", overlay = true)

strat_dir_input = input(title="Strategy Direction", defval="long", options=["long", "short", "all"])- 1