اپنی مرضی کے مطابق غیر ریپینٹنگ HTF MACD MFI توسیع پذیر بوٹ حکمت عملی

خلاصہ

یہ حکمت عملی ایک انتہائی حسب منشا، غیر دوبارہ ڈرائنگ کرنے والے MACD اور MFI اشاریوں کا مجموعہ ہے، جو الگورتھمک ٹریڈنگ روبوٹس کے لیے موزوں ہے۔ یہ رجحان (Trend) اور رفتار (Momentum) کے اشاریوں کو ملا کر متعدد فلٹرز کے ذریعے ٹریڈنگ سگنلز پیدا کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی مارکیٹ کے رجحان کی سمت جاننے کے لیے MACD اشاریہ استعمال کرتی ہے۔ MACD ایک رجحان پر مبنی رفتار کا اشاریہ ہے، جو تیز رفتار موونگ ایوریج کو سست رفتار موونگ ایوریج سے منہا کر کے MACD ہسٹوگرام بناتا ہے، اور پھر MACD کے ایکسپونینشل موونگ ایوریج سے سگنل لائن حاصل کی جاتی ہے۔ جب تیز لائن سست لائن کو اوپر سے عبور کرے تو یہ خرید کا سگنل ہوتا ہے، اور جب نیچے سے عبور کرے تو فروخت کا سگنل ہوتا ہے۔

اس کے علاوہ، یہ حکمت عملی مارکیٹ کی زیادہ خریدی گئی (Overbought) یا زیادہ فروخت کی گئی (Oversold) حالت جاننے کے لیے MFI اشاریہ بھی استعمال کرتی ہے۔ MFI اشاریہ قیمت اور حجم کی معلومات کو یکجا کرتا ہے، اور اس کی قدر 0 سے 100 کے درمیان اتار چڑھاؤ کرتی ہے۔ جب MFI 20 سے نیچے ہوتا ہے تو یہ زیادہ فروخت کا علاقہ ہوتا ہے، اور جب 80 سے اوپر ہوتا ہے تو یہ زیادہ خرید کا علاقہ ہوتا ہے۔

جھوٹے سگنلز کو فلٹر کرنے کے لیے، اس حکمت عملی میں رجحان فلٹر (Trend Filter) اور RSI فلٹر بھی شامل کیے گئے ہیں۔ جب قیمت بڑھتے ہوئے رجحان میں ہو اور RSI مقررہ حد سے کم ہو تو خرید کا سگنل پیدا ہوتا ہے۔

حکمت عملی کے فوائد

- متعدد اشاریوں کو ملا کر مارکیٹ کی حالت کا جامع جائزہ لینا، جیت کی شرح میں اضافہ

- فلٹر میکنزم شامل کر کے جھوٹے سگنلز سے بچنا اور غیر ضروری ٹریڈنگ کو کم کرنا

- مختلف پیرامیٹرز اور فلٹرز کو حسب منشا ترتیب دیا جا سکتا ہے، جو مختلف اثاثوں اور ٹریڈنگ ترجیحات کے مطابق ڈھل سکتے ہیں

- دستی ٹریڈنگ کے ساتھ ساتھ الگورتھمک روبوٹ سے منسلک کر کے پروگرامیٹک ٹریڈنگ بھی کی جا سکتی ہے

حکمت عملی کے خطرات اور حل

-

اشاریوں کے پیرامیٹرز کی غلط ترتیب سے جھوٹے سگنلز پیدا ہو سکتے ہیں

-

مختلف پیرامیٹرز کو جانچ کر بہترین امتزاج منتخب کیا جا سکتا ہے

-

مختلف اثاثوں کے لیے پیرامیٹرز عالمی نہیں ہوتے، انہیں الگ سے جانچنا اور بہتر بنانا ضروری ہے

-

ٹریڈنگ کی فریکوئنسی بہت زیادہ ہو سکتی ہے، جس سے ٹریڈنگ کے اخراجات اور سلپج کا خطرہ بڑھ جاتا ہے

-

فلٹرز کو ایڈجسٹ کر کے ٹریڈنگ کی فریکوئنسی کم کی جا سکتی ہے

-

حقیقی ٹریڈنگ میں لاگت پر قابو رکھنا ضروری ہے

حکمت عملی کی بہتری کے ممکنہ راستے

- طویل ڈیٹا پیریڈ پر جانچ کر کے پیرامیٹرز کے استحکام کا جائزہ لینا

- اشاریوں کے مختلف امتزاجات آزمائنا

- اشاریوں کے وزن کو بہتر بنا کر حکمت عملی کے استحکام میں اضافہ کرنا

- مزید فلٹرز شامل کر کے غیر ضروری ٹریڈنگ کو کم کرنا

خلاصہ

یہ حکمت عملی ایک انتہائی حسب منشا رجحان پر مبنی حکمت عملی ہے، جو رجحان اور رفتار کے اشاریوں کو ملا کر مارکیٹ کی حالت کا تعین کرتی ہے اور فلٹر میکنزم کے ذریعے مؤثر طریقے سے خطرے کو کنٹرول کرتی ہے۔ یہ دستی ٹریڈنگ کے ساتھ ساتھ الگورتھمک روبوٹ سے منسلک ہو کر خودکار پروگرامیٹک ٹریڈنگ کے لیے بھی استعمال کی جا سکتی ہے، اور ایک ایسا نظام ہے جس کی طویل مدتی نگرانی اور بہتری کی جا سکتی ہے۔

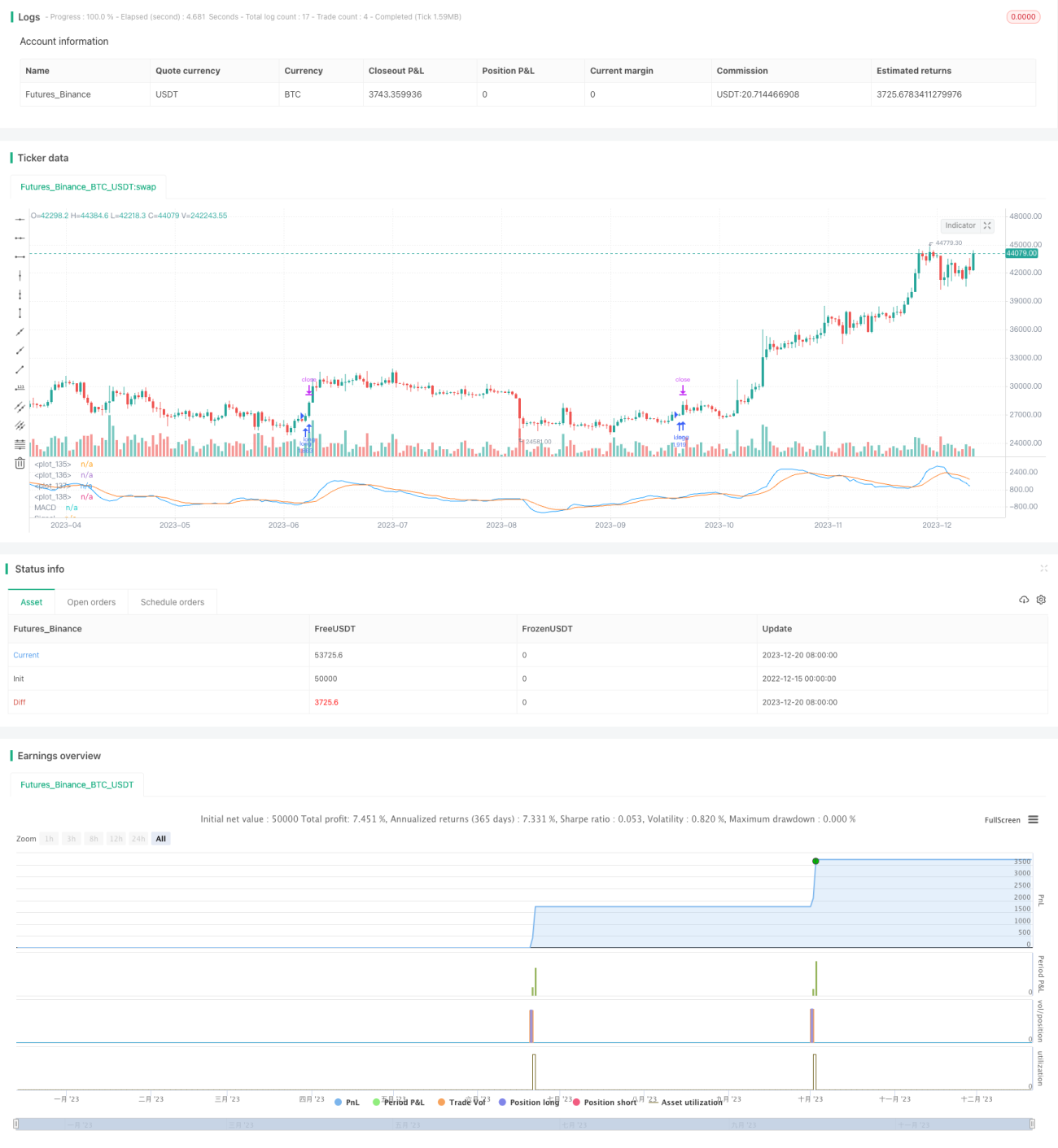

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1