تین موونگ اوسط کم تاخیر تیز تجارتی حکمت عملی

حکمت عملی کا اصول

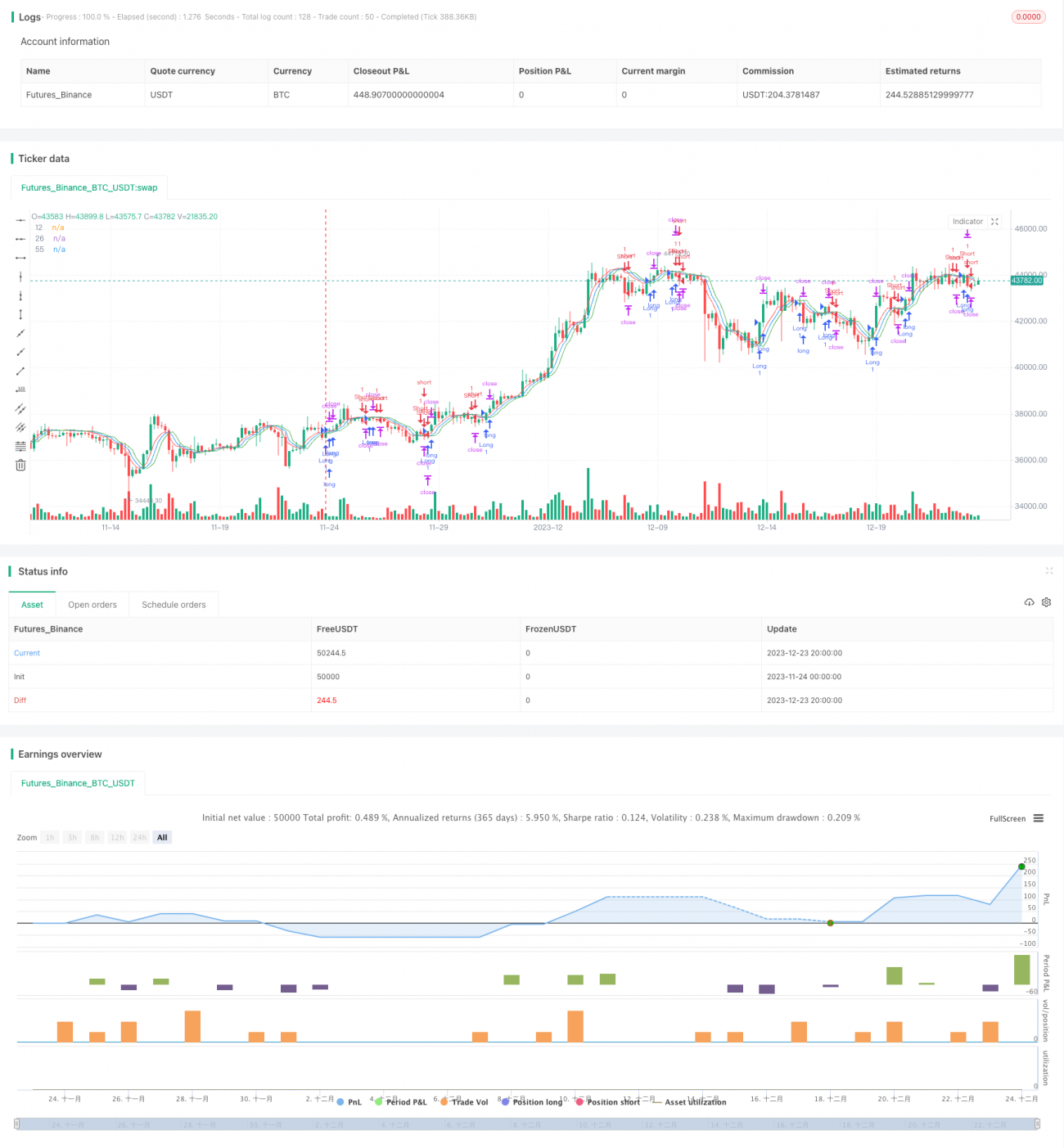

یہ حکمت عملی تین کم تاخیر والی حرکت پذیری اوسطیں استعمال کرتی ہے، جن میں 12، 26 اور 55 ادوار کی کم تاخیر والی TEMA اوسطیں شامل ہیں۔ یہ تین اوسطیں بالترتیب تیز رفتار، درمیانی رفتار اور سست رفتار اوسطوں کی نمائندگی کرتی ہیں۔ جب تیز رفتار اوسط درمیانی رفتار اوسط کو اوپر سے پار کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے۔ جب تیز رفتار اوسط درمیانی رفتار اوسط کو نیچے سے پار کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔ اس طرح تین اوسطوں کے کراس اوور کے ذریعے مارکیٹ میں خرید و فروخت کے مقامات کا تعین کیا جاتا ہے، جس سے اعلی تعدد تجارت ممکن ہوتی ہے۔

کوڈ میں tema() نامی ٹیمپلیٹ فنکشن کی وضاحت کی گئی ہے جو کم تاخیر والی TEMA اوسط کا حساب لگاتا ہے۔ اس کا حساب کتابی فارمولا ہے: TEMA = 2*EMA - EMA(EMA)۔ یہ دوہری ایکسپونینشل موونگ ایوریج EWMA کا استعمال کرتا ہے۔ بنیادی طور پر یہ ایک دوہری ہموار حرکت پذیری اوسط ہے جس کا سب سے بڑا فائدہ تاخیر کو نمایاں طور پر کم کرنا ہے۔ اس طرح یہ قیمت کی تبدیلیوں پر زیادہ تیزی سے رد عمل ظاہر کر سکتی ہے اور تجارتی سگنلز کی بروقت تشخیص کو بہتر بنا سکتی ہے۔

خاص طور پر، اس حکمت عملی کے داخلے کا فیصلہ اس طرح ہے: جب تیز رفتار اوسط درمیانی رفتار اوسط کو اوپر سے پار کرتی ہے اور تیز رفتار اوسط سست رفتار اوسط سے زیادہ ہوتی ہے تو خرید کا سگنل پیدا ہوتا ہے۔ جب تیز رفتار اوسط درمیانی رفتار اوسط کو نیچے سے پار کرتی ہے اور تیز رفتار اوسط سست رفتار اوسط سے کم ہوتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کا سب سے بڑا فائدہ داخلے اور اخراج کا تیز اور درست فیصلہ ہے۔ تین اوسطوں کا کم تاخیر والا ڈیزائن تاخیر کو بہت کم کر دیتا ہے، جس سے وہ قیمت کی تبدیلیوں پر تیزی سے رد عمل ظاہر کر سکتی ہیں۔ نیز، تین اوسطوں کے کراس اوور کا استعمال کرتے ہوئے سگنلز کی تشخیص غلط سگنلز سے بچاتی ہے۔

اس کے علاوہ، یہ حکمت عملی اعلی تعدد تجارت کے لیے موزوں ہے تاکہ قلیل مدتی قیمت کے اتار چڑھاؤ سے منافع کمایا جا سکے۔ تیز اندراج اور اخراج کے ذریعے یہ زیادہ اتار چڑھاؤ والی مارکیٹوں میں منافع کما سکتی ہے۔

خطرے کا تجزیہ

سب سے بڑا خطرہ یہ ہے کہ انتہائی قلیل مدتی جھولے (وہپسا) پیدا ہو سکتے ہیں۔ کم تاخیر والے ڈیزائن کی وجہ سے قیمت کی تبدیلیوں کے لیے زیادہ حساسیت کی وجہ سے، کچھ مارکیٹوں میں زیادہ تعدد والے اتار چڑھاؤ کا سامنا ہو سکتا ہے۔ پھر جھولے (وہپسا) ہونے کا بہت امکان ہے۔

نیز، اعلی تعدد تجارت میں نسبتاً زیادہ کمیشن اور سلپج لاگت ادا کرنی پڑتی ہے۔ اگر منافع حاصل کرنے کی صلاحیت ناکافی ہے تو تجارتی اخراجات کی وجہ سے نقصان اٹھانا آسان ہے۔

مزید برآں، اس حکمت عملی کے لیے تاجر کو مضبوط ریئل ٹائم نگرانی کی صلاحیتوں کی ضرورت ہوتی ہے تاکہ وہ سٹاپ لاس اور ٹیک پروف کو بروقت اپ ڈیٹ کر سکے۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

-

تین اوسطوں کے دورانیے کے پیرامیٹرز کو بہتر بنائیں تاکہ مختلف مارکیٹوں کی خصوصیات کے ساتھ بہتر مطابقت پیدا ہو سکے۔

-

سگنلز کی تصدیق کے لیے اتار چڑھاؤ کے اشارے یا حجم کے اشارے شامل کریں تاکہ رینج والی مارکیٹوں میں جھولے (وہپسا) سے بچا جا سکے۔

-

متحرک ٹریلنگ سٹاپ میکانزم قائم کرنے کے لیے مزید عوامل کو شامل کریں۔

-

رقم کے انتظام کی تکنیکوں کے ذریعے ایک ہی تجارت کے خطرے کو کنٹرول کرنے کے لیے پوزیشن سائزنگ کو بہتر بنائیں۔

-

حکمت عملی کے پیرامیٹرز کو متحرک طور پر بہتر بنانے کے لیے مشین لرننگ الگورتھم شامل کریں۔

خلاصہ

یہ حکمت عملی ایک کم تاخیر والی تین اوسطوں پر مبنی تیز رفتار تجارتی حکمت عملی ہے۔ یہ کم تاخیر والے ڈیزائن کے ذریعے تیز اندراج اور اخراج کو ممکن بناتی ہے، جو اعلی تعدد تجارت کے ذریعے قلیل مدتی مواقع حاصل کرنے کے لیے موزوں ہے۔ اس حکمت عملی کا سب سے بڑا فائدہ سگنلز کی تیز اور درست تشخیص ہے، جبکہ سب سے بڑا نقصان یہ ہے کہ یہ اتار چڑھاؤ والی مارکیٹوں میں جھولے (وہپسا) کا شکار ہو سکتی ہے۔ اس مضمون میں مفصل اصولوں کے تجزیے، فوائد کے تجزیے، خطرے کے تجزیے اور بہتری کے بارے میں بحث کرکے اس تجارتی حکمت عملی کا مکمل جائزہ پیش کیا گیا ہے۔

نتیجہ

یہ ایک کم تاخیر والی تین مووینگ اوسط کی تیز رفتار تجارتی حکمت عملی ہے۔ اس کی کم تاخیر والی ڈیزائن کی وجہ سے تیزی سے داخلے اور اخراج ممکن ہوتا ہے، جو قلیل مدتی مواقع حاصل کرنے کے لیے اعلی تعدد تجارت کے لیے موزوں ہے۔ اس حکمت عملی کا سب سے بڑا فائدہ یہ ہے کہ اس کے سگنل کا تعین تیز اور درست ہے۔ سب سے بڑا نقصان یہ ہے کہ یہ رینج مارکیٹوں میں آسانی سے جھوٹے سگنل دینے کا شکار ہوتی ہے۔ یہ مضمون اس تجارتی حکمت عملی کے عقلی بنیادوں، فوائد، خطرات اور اصلاح کی سمتوں کے تفصیلی تجزیے کے ذریعے جامع خلاصہ پیش کرتا ہے۔

[/trans]

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("scalping low lag tema etal", shorttitle="Scalping tema",initial_capital=10000, overlay=true)

mav = input(title="Moving Average Type", defval="temadelay", options=["nkclose", "ema", "emadelay", "fastema", "tema", "temadelay"])

lenb = 3- 1