مقداری اشاریوں پر مبنی بٹ کوائن تجارتی حکمت عملی

جائزہ

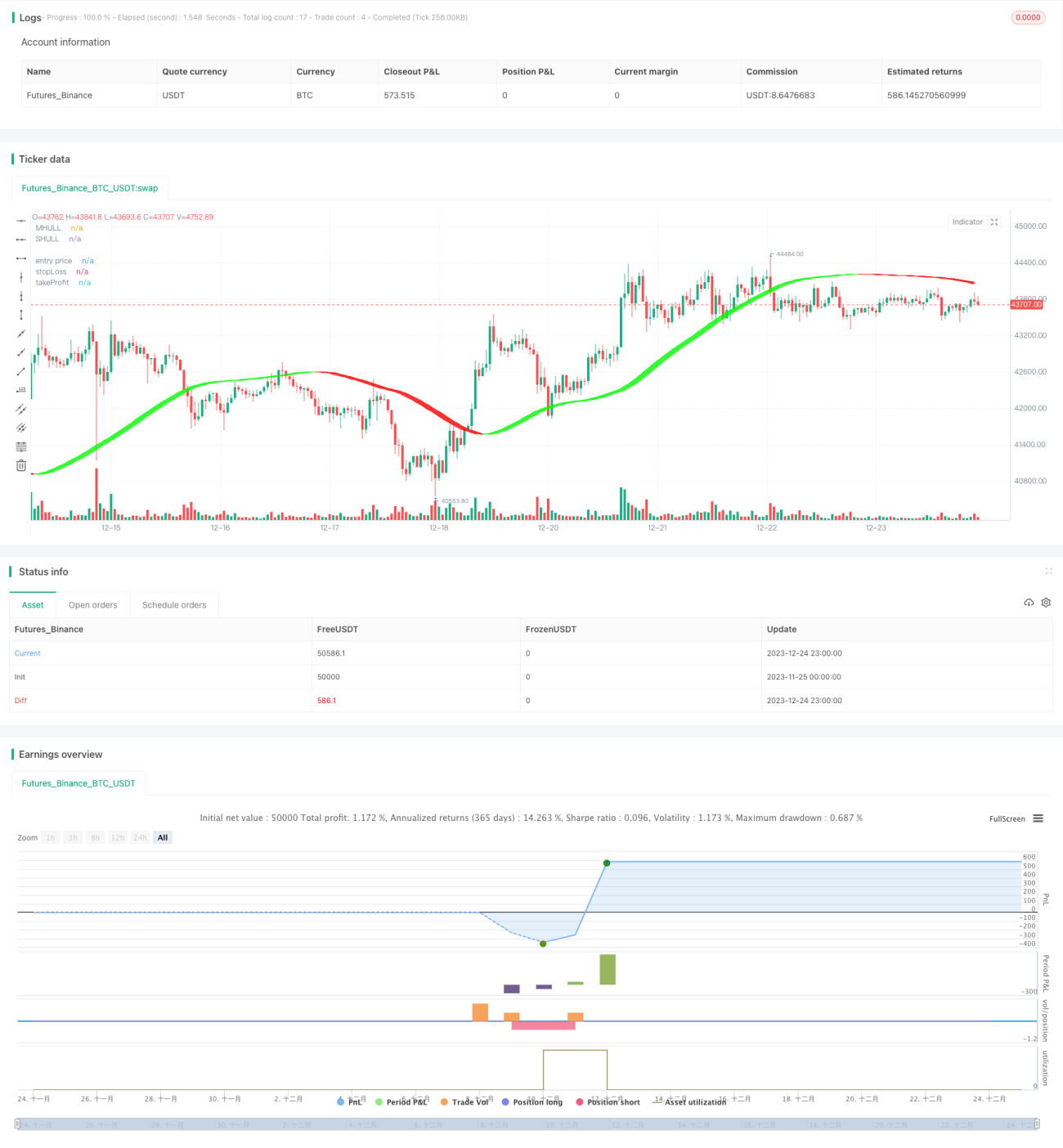

یہ حکمت عملی بٹ کوائن کی خرید و فروخت کے مواقع کا تعین کرنے کے لیے متعدد مقداری اشاریوں کا استعمال کرتی ہے، اور خودکار تجارت کو قابل بناتی ہے۔ بنیادی طور پر اس میں ہل انڈیکیٹر، رشتہ دار طاقت کا اشاریہ (RSI)، بولنگر بینڈز (BB) اور حجم اوسلیٹر (VO) شامل ہیں۔

حکمت عملی کا اصول

-

ترمیم شدہ ہل موونگ ایوریج کا استعمال کرتے ہوئے مارکیٹ کے اہم رجحان کی سمت کا تعین کیا جاتا ہے، اور بولنگر بینڈز کی مدد سے بریک آؤٹ خرید و فروخت کے مقامات کا پتہ لگایا جاتا ہے۔

-

RSI انڈیکیٹر کو موافق اتار چڑھاؤ کی حد کے ساتھ ملا کر زیادہ خریدے گئے/زیادہ بیچے گئے علاقوں کا تعین کیا جاتا ہے، اور تجارتی سگنل جاری کیے جاتے ہیں۔ اسی کے ساتھ ڈپلیکیٹ سگنل کی تصدیق کے لیے دو پیرامیٹر سیٹ رکھے جاتے ہیں۔

-

حجم اوسلیٹر خرید و فروخت کی قوت کا تعین کرتا ہے، تاکہ جھوٹے بریک آؤٹ سے بچا جا سکے۔

-

سٹاپ لاس/ٹیک پرافٹ کے تناسب کے پیرامیٹر کی بنیاد پر پہلے سے طے شدہ سٹاپ لاس اور ٹیک پرافٹ کی سطحیں رکھی جاتی ہیں، تاکہ رسک مینجمنٹ کو ممکن بنایا جا سکے۔

فوائد کا تجزیہ

-

ہل کرو رجحان کی تبدیلی کو تیزی سے پکڑ سکتا ہے، اور بولنگر بینڈز کی معاون تشخیص جھوٹے سگنلز کو کم کر سکتی ہے۔

-

RSI انڈیکیٹر کے پیرامیٹرز کو بہتر بنایا گیا ہے اور ڈپلیکیٹ سگنل کی تصدیق سے اعتماد میں اضافہ ہوا ہے۔

-

حجم اوسلیٹر رجحان اور انڈیکیٹر سگنلز کے ساتھ مل کر غلط تجارت سے بچاتا ہے۔

-

پہلے سے طے شدہ سٹاپ لاس اور ٹیک پرافٹ کا طریقہ خود بخود ایک تجارت کے نقصان کو کنٹرول کر سکتا ہے، اور مجموعی خطرے کو مؤثر طریقے سے سنبھال سکتا ہے۔

خطرات کا تجزیہ

-

پیرامیٹرز کی غلط ترتیب سے تجارت کی تعدد بہت زیادہ ہو سکتی ہے یا سگنلز کی کارکردگی خراب ہو سکتی ہے۔

-

غیر متوقع واقعات کی وجہ سے مارکیٹ میں شدید اتار چڑھاؤ کے دوران، سٹاپ لاس ٹوٹ سکتا ہے، جس سے بڑا نقصان ہو سکتا ہے۔

-

جب تجارتی شے کو کسی دوسرے سکے میں تبدیل کیا جائے تو پیرامیٹرز کو دوبارہ جانچنے اور بہتر بنانے کی ضرورت ہوتی ہے۔

-

جب حجم کا ڈیٹا غائب ہو تو حجم اوسلیٹر ناکام ہو جاتا ہے۔

بہتری کے ممکنہ راستے

-

RSI کے پیرامیٹرز کے لیے مزید امتزاجی ٹیسٹ کیے جائیں تاکہ بہترین پیرامیٹرز مل سکیں۔

-

دوسرے انڈیکیٹرز جیسے MACD، KD وغیرہ کو RSI کے ساتھ ملا کر سگنلز کی درستگی میں اضافہ کیا جا سکتا ہے۔

-

ماڈل پیش گوئی کا ماڈیول شامل کیا جائے، جو مشین لرننگ کی مدد سے مارکیٹ کی سمت کا تعین کرے۔

-

دوسرے تجارتی اثاثوں کے ساتھ پیرامیٹرز کی کارکردگی کو جانچا جائے۔

-

سٹاپ لاس اور ٹیک پرافٹ الگورتھم کو بہتر بنایا جائے تاکہ منافع زیادہ سے زیادہ حاصل کیا جا سکے۔

خلاصہ

یہ حکمت عملی متعدد مقداری تکنیکی اشاریوں کو یکجا کرکے خرید و فروخت کے مواقع کا تعین کرتی ہے۔ پیرامیٹر کی بہتری، رسک کنٹرول وغیرہ کے ذریعے بٹ کوائن کی خودکار تجارت ممکن بنائی گئی ہے۔ اس کی کارکردگی اچھی ہے، لیکن مارکیٹ کی تبدیلیوں کے مطابق ڈھالنے کے لیے مسلسل جانچ اور بہتری کی ضرورت ہے۔ یہ سرمایہ کاروں کے لیے تجارتی فیصلوں میں مدد فراہم کر سکتی ہے۔

- 1