خودمطابقت پذیر بووینکو اشاریہ کی لانگ اور شارٹ حکمت عملی

جائزہ (Overview)

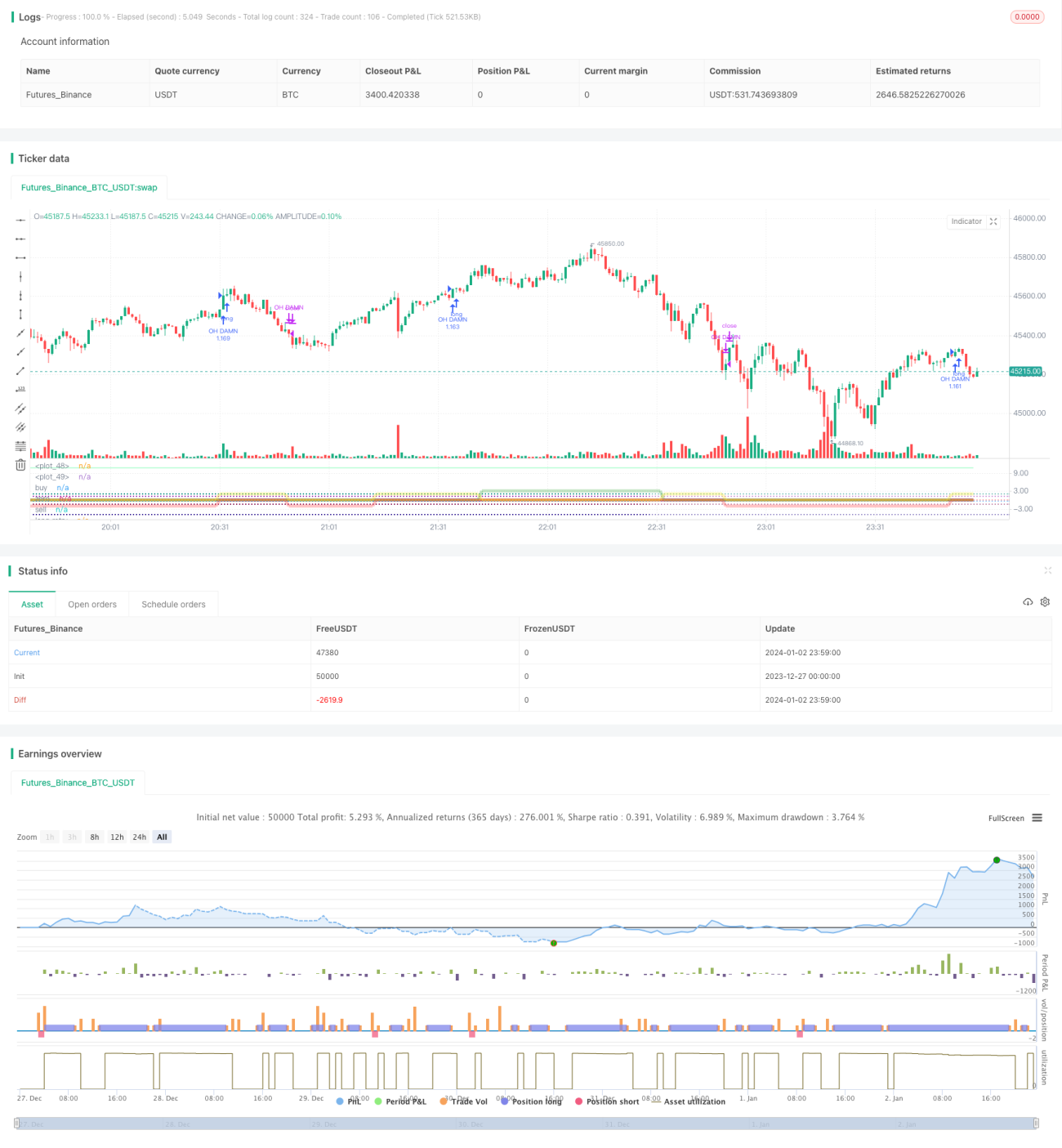

یہ حکمت عملی بووینکو انڈیکیٹر پر مبنی ہے اور خود بخود مارکیٹ کے رجحان کی شناخت کر کے لمبی اور چھوٹی پوزیشنیں قائم کرتی ہے۔ اس میں بووینکو انڈیکیٹر، موونگ ایوریجز اور افقی سپورٹ لائنز جیسے تکنیکی اشارے شامل ہیں، جو خود بخود بریک آؤٹ سگنلز کی شناخت اور پوزیشنیں قائم کر سکتے ہیں۔

حکمت عملی کا اصول (Strategy Principle)

اس حکمت عملی کا بنیادی انڈیکیٹر بووینکو انڈیکیٹر ہے، جو مختلف ٹریڈنگ دنوں کی اختتامی قیمتوں کے لوگارتھمک فرق کا حساب لگا کر مارکیٹ کے رجحان اور اہم سپورٹ/مزاحمتی سطحوں کا تعین کرتا ہے۔ جب انڈیکیٹر کسی افقی لائن کو اوپر سے کراس کرتا ہے تو لمبی پوزیشن لی جاتی ہے، اور جب نیچے سے کراس کرتا ہے تو چھوٹی پوزیشن لی جاتی ہے۔

اس کے علاوہ، یہ حکمت عملی 21 دن اور 55 دن کی متعدد موونگ ایوریجز پر مشتمل "EMA پروٹیکشن بیلٹ" کو بھی مربوط کرتی ہے۔ ان موونگ ایوریجز کی ترتیب کی بنیاد پر یہ طے کیا جاتا ہے کہ مارکیٹ فی الحال تیزی کا رجحان رکھتی ہے، مندی کا رجحان رکھتی ہے، یا سائیڈ ویز ہے، اور اس کے مطابق چھوٹی یا لمبی پوزیشنوں پر پابندی لگائی جاتی ہے۔

بووینکو انڈیکیٹر سے ٹریڈنگ سگنلز کی شناخت اور موونگ ایوریجز سے مارکیٹ کے مرحلے کا تعین کرکے، ان دونوں کو ملا کر استعمال کرنے سے نامناسب پوزیشنوں کے قیام سے بچا جا سکتا ہے۔

فوائد کا تجزیہ (Advantage Analysis)

اس حکمت عملی کا سب سے بڑا فائدہ یہ ہے کہ یہ خود بخود مارکیٹ کے تیزی اور مندی کے رجحان کی شناخت کر سکتی ہے۔ بووینکو انڈیکیٹر دو وقت کے ادوار کی قیمتوں کے فرق کے لیے بہت حساس ہے، جس سے یہ اہم سپورٹ اور مزاحمت کو تیزی سے تلاش کر سکتا ہے؛ اسی کے ساتھ، موونگ ایوریجز کی ترتیب مؤثر طریقے سے اس بات کا تعین کر سکتی ہے کہ مارکیٹ کس مرحلے میں ہے، تیزی میں یا مندی میں۔

تیز رفتار انڈیکیٹرز اور رجحانی انڈیکیٹرز کو یکجا کرنے کا یہ طریقہ حکمت عملی کو خرید و فروخت کے مقامات کو تیزی سے تلاش کرنے کے ساتھ ساتھ نامناسب خرید و فروخت سے بچنے کی صلاحیت فراہم کرتا ہے۔ یہی اس حکمت عملی کا سب سے بڑا فائدہ ہے۔

خطرے کا تجزیہ (Risk Analysis)

اس حکمت عملی کے خطرات بنیادی طور پر دو پہلوؤں سے آتے ہیں: پہلا، بووینکو انڈیکیٹر خود قیمت کی تبدیلیوں کے لیے بہت حساس ہے، جس کی وجہ سے بہت سے غیر ضروری ٹریڈنگ سگنلز پیدا ہو سکتے ہیں؛ دوسرا، سائیڈ ویز مارکیٹ میں موونگ ایوریجز کی ترتیب میں الجھن پیدا ہو سکتی ہے، جس سے پوزیشنوں کے قیام میں ابہام پیدا ہو سکتا ہے۔

پہلے خطرے کے لیے، بووینکو انڈیکیٹر کے پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کیا جا سکتا ہے، انڈیکیٹر کے حساب کتاب کے دورانیے میں اضافہ کر کے غیر ضروری ٹریڈنگ کو کم کیا جا سکتا ہے؛ دوسرے خطرے کے لیے، مزید موونگ ایوریجز شامل کی جا سکتی ہیں تاکہ رجحان کا تعین زیادہ درست ہو سکے۔

بہتری کی سمت (Optimization Directions)

اس حکمت عملی کی اہم بہتری کی سمت پیرامیٹر ایڈجسٹمنٹ اور فلٹر شرائط میں اضافہ ہے۔

بووینکو انڈیکیٹر کے لیے، مختلف دورانیے کے پیرامیٹرز آزمائے جا سکتے ہیں تاکہ بہترین پیرامیٹر مجموعہ حاصل کیا جا سکے؛ موونگ ایوریجز کے لیے، مزید اوسطیں شامل کی جا سکتی ہیں تاکہ رجحان کے تعین کا ایک مکمل نظام تشکیل دیا جا سکے۔ اس کے علاوہ، اتار چڑھاؤ کے انڈیکیٹرز، ٹریڈنگ والیوم کے انڈیکیٹرز وغیرہ جیسے فلٹر شرائط بھی شامل کی جا سکتی ہیں تاکہ جھوٹے سگنلز کو کم کیا جا سکے۔

پیرامیٹرز اور شرائط کی جامع ایڈجسٹمنٹ کے ذریعے، حکمت عملی کے استحکام اور منافع بخشی کو مزید بہتر بنایا جا سکتا ہے۔

خلاصہ (Summary)

یہ خود کار بووینکو لمبی اور چھوٹی حکمت عملی کامیابی کے ساتھ تیز رفتار انڈیکیٹرز اور رجحانی انڈیکیٹرز کو یکجا کرتی ہے، جو مارکیٹ کے اہم نکات کی خود بخود شناخت اور صحیح پوزیشنیں قائم کر سکتی ہے۔ اس کا فائدہ تیزی سے مقامات کی شناخت اور نامناسب پوزیشنوں کے قیام سے بچنے کی صلاحیت ہے۔ اگلے مرحلے میں پیرامیٹرز اور شرائط کی بہتری کے ذریعے حکمت عملی کے استحکام اور منافع بخشی کو مزید بڑھایا جا سکتا ہے۔

- 1