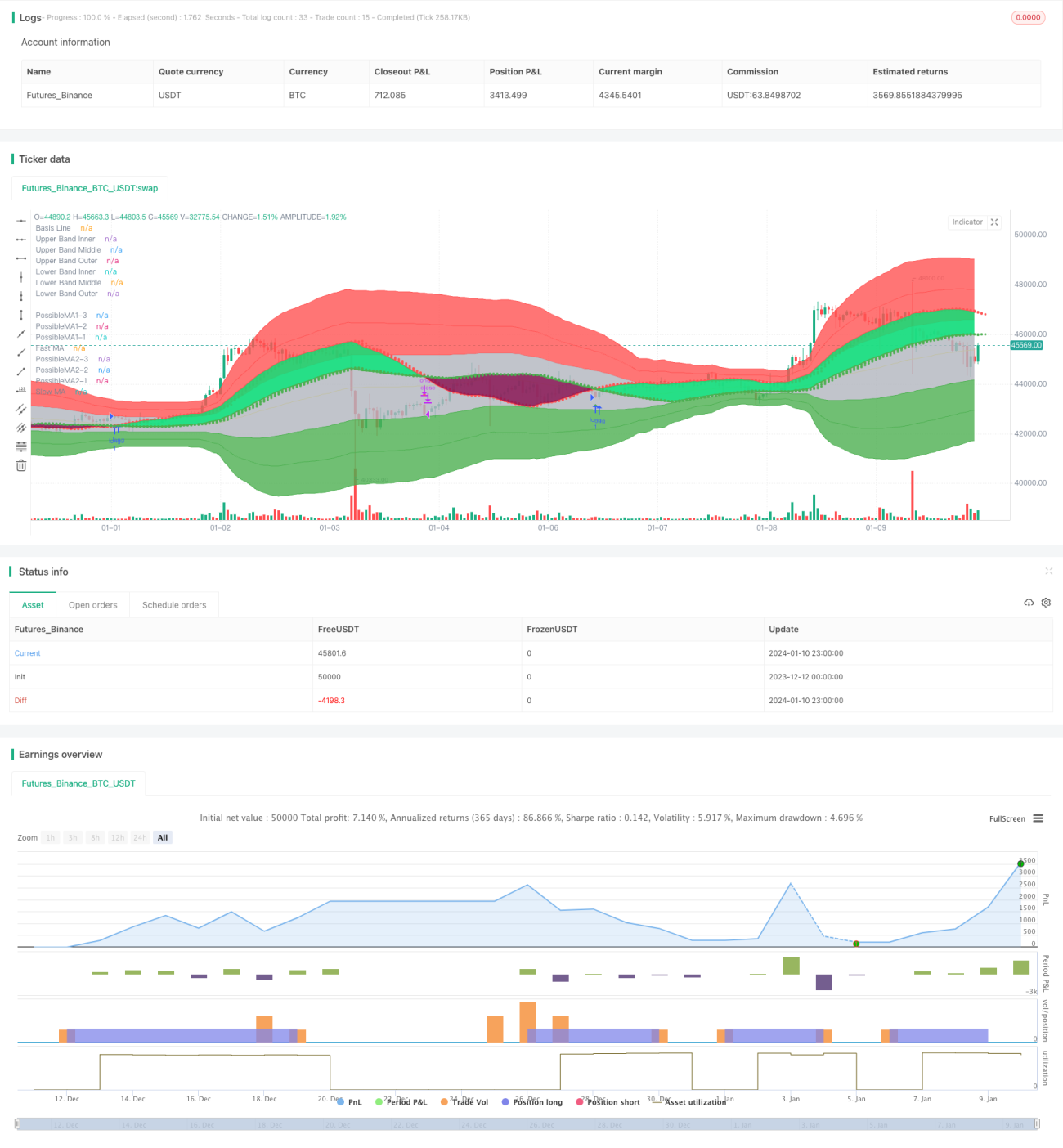

حرکت توانائی وزنی متحرک اوسط دوہرا کراس اوور حکمت عملی

1

Follow

1802

Followers

خلاصہ

یہ حکمت عملی دو مختلف ادوار کے متحرک وزن والے موونگ ایوریج (MAEMA) کا حساب لگا کر، ان کے کراس اوور پر خرید و فروخت کے سگنل تیار کرتی ہے۔ اس میں مختصر دورانیے کی لائن مارکیٹ کے رجحان اور قلیل مدتی الٹ جانے کے سگنلز کا تعین کرتی ہے، جبکہ طویل دورانیے کی لائن بنیادی رجحان کی سمت متعین کرتی ہے۔

اصول

- تیز لائن (80 دورانیہ) اور سست لائن (144 دورانیہ) کے MAEMA کا حساب لگائیں۔

- تیز لائن قلیل مدتی رجحان اور الٹ جانے کے نکات کی عکاسی کرتی ہے۔ سست لائن بنیادی رجحان کی سمت دکھاتی ہے۔

- جب تیز لائن سست لائن کو اوپر سے عبور کرے تو خرید کا سگنل پیدا ہوتا ہے۔ جب تیز لائن سست لائن کو نیچے سے عبور کرے تو فروخت کا سگنل پیدا ہوتا ہے۔

- یہ حکمت عملی اگلے دورانیے کے ممکنہ اقدار کی پیش گوئی کے لیے 3 پوائنٹس بھی کھینچتی ہے، جس سے مستقبل کے کراس اوور کے رجحان کا اندازہ لگایا جا سکتا ہے۔

- حکمت عملی میں MAEMA انڈیکیٹر کی خود کی حرکیاتی خصوصیت اور پیش گوئی کی صلاحیت کو پوری طرح استعمال کیا گیا ہے۔

فوائد کا تجزیہ

- MAEMA میں خود ہی حرکیاتی عنصر شامل ہے، جو رجحانات میں تبدیلی کو تیزی سے پکڑ سکتا ہے۔

- دوہری موونگ ایوریج حکمت عملی، مختلف وقت کے فریموں میں رجحان کی سمت کا تعین کرتی ہے۔

- تیز اور سست لائنوں کے کراس اوور کے ساتھ MAEMA کے خودکار پیش گوئی پوائنٹس کا امتزاج خرید و فروخت کے سگنلز کو زیادہ قابل اعتماد بناتا ہے۔

- خودکار چارٹنگ مکمل ہے، جو مارکیٹ کی اتار چڑھاؤ کو بصارت سے ظاہر کرتی ہے۔

خطرے کا تجزیہ

- مارکیٹ میں غیر معمولی اتار چڑھاؤ کی صورت میں، MAEMA انڈیکیٹر کی حساسیت بہت زیادہ ہو سکتی ہے، جس سے غلط سگنل پیدا ہو سکتے ہیں۔ اسٹاپ لاس پوائنٹس کو مناسب حد تک نرم کیا جا سکتا ہے۔

- موونگ ایوریج سسٹم رینج مارکیٹ میں جعلی سگنل پیدا کرنے کا امکان رکھتا ہے۔ دیگر فلٹرز شامل کیے جا سکتے ہیں۔

- تیز اور سست لائنوں کے ادوار کی ترتیب کو مختلف مصنوعات کے مطابق بہترین پیرامیٹرز تلاش کرنے کی ضرورت ہے۔

بہتری کی سمت

- MAEMA کی تیز اور سست لائنوں کے دورانیے کے پیرامیٹرز کو بہتر بنائیں اور بہترین پیرامیٹرز کا مجموعہ تلاش کریں۔

- اوسیلیٹنگ مارکیٹ میں پوزیشن کھولنے سے بچنے کے لیے فلٹرنگ کے حالات شامل کریں، مثلاً DMI، MACD وغیرہ متعارف کروائیں تاکہ رجحان کی پہچان ہو سکے۔

- بیک ٹیسٹ کے نتائج کی بنیاد پر ATR کوفیشنٹ اور متحرک اسٹاپ لاس پوائنٹس کو مسلسل ایڈجسٹ کریں تاکہ غلط مثبت سگنلز کم ہوں اور خطرے پر قابو پایا جا سکے۔

نتیجہ

یہ حکمت عملی متحرک وزن والے موونگ ایوریج کی دوہری لائنوں کے کراس اوور کے ذریعے مارکیٹ کے رجحان میں تبدیلی کا تعین کرتی ہے، اس کا بنیادی اصول سادہ اور واضح ہے۔ MAEMA کی خود کی حرکیاتی اور پیش گوئی کی صلاحیتوں کو ملا کر، الٹ جانے کے سگنلز کو پہچاننے میں اچھی کارکردگی دکھاتی ہے۔ پیرامیٹرز کی بہتری اور فلٹرنگ کے حالات کو مضبوط کرنے کی ضرورت ہے تاکہ استحکام بڑھایا جا سکے۔

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1