مضبوط رجحان کی پیروی کی حکمت عملی

خلاصہ

اس حکمت عملی کا بنیادی خیال 123 ریورسل پیٹرن اور اسمارٹ منی انڈیکس (SMI) اشارے کو یکجا کرکے مستحکم ٹرینڈ ٹریکنگ ٹریڈنگ حاصل کرنا ہے۔ جب دونوں سگنل بیک وقت خرید یا فروخت کے سگنل جاری کریں گے، تب ہی یہ حکمت عملی متعلقہ لانگ یا شارٹ پوزیشن قائم کرے گی۔

حکمت عملی کا اصول

یہ حکمت عملی دو حصوں پر مشتمل ہے:

-

123 ریورسل حکمت عملی: یہ حکمت عملی اسٹاک کی بند قیمت اور 9 روزہ Stoch اشارے کی بنیاد پر ریورسل ٹریڈنگ کو نافذ کرتی ہے۔ خاص طور پر، جب مسلسل دو دنوں کی بند قیمتوں کا تعلق الٹ جائے (یعنی پچھلے دن کی بند قیمت اس سے پہلے والے دن سے زیادہ ہو، اور اگلے دن کی بند قیمت پچھلے دن سے کم ہو)، اور Stoch تیز رفتار لائن سست رفتار لائن سے اوپر ہو، تو شارٹ کریں؛ جب مسلسل دو دنوں کی بند قیمتوں کا تعلق الٹ جائے (یعنی پچھلے دن کی بند قیمت اس سے پہلے والے دن سے کم ہو، اور اگلے دن کی بند قیمت پچھلے دن سے زیادہ ہو)، اور Stoch تیز رفتار لائن سست رفتار لائن سے نیچے ہو، تو لانگ کریں۔

-

SMI حکمت عملی: یہ حکمت عملی اسمارٹ منی انڈیکس کی بنیاد پر ٹرینڈ ٹریکنگ کو نافذ کرتی ہے۔ SMI اشارہ ادارہ جاتی فنڈز اور خوردہ فنڈز کے درمیان مقابلے کی عکاسی کر سکتا ہے، SMI کا بڑھنا ادارہ جاتی فنڈز کے جذب ہونے کی نشاندہی کرتا ہے، جبکہ اس کا گرنا ادارہ جاتی فنڈز کے فروخت ہونے کی نشاندہی کرتا ہے۔ جب SMI بڑھے تو لانگ کریں، اور جب SMI گرے تو شارٹ کریں۔

جب 123 ریورسل پیٹرن اور SMI اشارہ بیک وقت خرید کا سگنل دیں گے، تب ہی یہ حکمت عملی لانگ پوزیشن لے گی؛ جب دونوں بیک وقت فروخت کا سگنل دیں گے، تب ہی یہ حکمت عملی شارٹ پوزیشن لے گی۔

حکمت عملی کے فوائد

یہ حکمت عملی ریورسل پیٹرن اور ٹرینڈ ٹریکنگ اشاروں کو یکجا کرکے مارکیٹ کے ریورسل پوائنٹس کو مؤثر طریقے سے شناخت کرتی ہے اور مستحکم منافع کے لیے ٹرینڈ کو ٹریک کرتی ہے۔ مخصوص فوائد درج ذیل ہیں:

-

123 ریورسل پیٹرن میں نسبتاً زیادہ جیت کی شرح اور منافع کی شرح ہوتی ہے، جو قلیل مدتی ریورسل مواقع کو مؤثر طریقے سے شناخت کر سکتی ہے۔

-

SMI اشارہ ادارہ جاتی فنڈز کی سمت کی عکاسی کر سکتا ہے۔ ادارہ جاتی فنڈز کو ٹریک کرنے سے نسبتاً مستحکم منافع حاصل کیا جا سکتا ہے۔

-

ریورسل پیٹرن اور ٹرینڈ ٹریکنگ اشاروں کے مشترکہ استعمال سے سگنلز کے معیار کو بہتر بنایا جا سکتا ہے، غیر ضروری ٹریڈنگ کو کم کیا جا سکتا ہے، اور خطرات کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے۔

حکمت عملی کے خطرات

اس حکمت عملی میں کچھ خطرات بھی ہیں، جو بنیادی طور پر درج ذیل شعبوں میں مرکوز ہیں:

-

123 ریورسل پیٹرن میں جھوٹے سگنلز کا ایک خاص خطرہ ہوتا ہے اور یہ نقصان دہ ٹریڈز کو مکمل طور پر نہیں روک سکتا۔ سگنل کے معیار کو بہتر بنانے کے لیے پیرامیٹرز کو مناسب طریقے سے بہتر بنایا جا سکتا ہے۔

-

SMI اشارے میں ایک خاص تاخیر ہوتی ہے اور یہ حقیقی وقت میں فنڈز کی سمت کو مکمل طور پر ظاہر نہیں کر سکتا۔ درستگی کو بہتر بنانے کے لیے تصدیق کے لیے دوسرے اشارے بھی شامل کیے جا سکتے ہیں۔

-

دوہرے سگنلز انتہائی قدامت پسندانہ مسائل کا باعث بن سکتے ہیں، ممکنہ طور پر مضبوط یک طرفہ رجحان کے مواقع سے محروم ہو سکتے ہیں۔ فلٹرنگ کے معیار کو کم کرنے کے لیے سگنل کی شرائط کو مناسب طریقے سے نرم کیا جا سکتا ہے۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

-

پیرامیٹرز کو بہتر بنانا، بہترین پیرامیٹر کمبینیشن تلاش کرنا، اور حکمت عملی کی منافع بخش صلاحیت کو بڑھانا۔

-

نقصان روکنے کا طریقہ کار شامل کرنا، جو ایک ٹریڈ کے نقصان کو مؤثر طریقے سے کنٹرول کر سکتا ہے۔

-

سگنل کے معیار کی مزید تصدیق کرنے اور سگنل کی درستگی کو بڑھانے کے لیے دوسرے اشارے یا پیٹرن کو شامل کرنا۔

-

مختلف مصنوعات کے لیے الگ الگ پیرامیٹرز کو بہتر بنانا، حکمت عملی کی موافقت کو بڑھانا۔

خلاصہ

اس حکمت عملی کا مجموعی نقطہ نظر واضح ہے، یہ مؤثر طریقے سے ریورسل پیٹرن اور ٹرینڈ ٹریکنگ اشاروں کو یکجا کرتی ہے، قلیل مدتی ریورسل مواقع کو مستحکم طریقے سے شناخت کر سکتی ہے اور درمیانی سے طویل مدتی رجحان کو ٹریک کر سکتی ہے۔ پیرامیٹرز کی اصلاح اور طریقہ کار کے ڈیزائن میں بہتری کے ذریعے، حکمت عملی کی منافع بخش صلاحیت اور خطرے پر قابو پانے کی صلاحیت کو مزید بڑھایا جا سکتا ہے۔

اصلاح کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

-

پیرامیٹرز کو بہتر بنا کر بہترین پیرامیٹر کمبینیشن تلاش کریں اور حکمت عملی کی منافع بخشی میں اضافہ کریں۔

-

نقصان روکنے کے طریقہ کار شامل کریں تاکہ ایک ہی نقصان کو مؤثر طریقے سے کنٹرول کیا جا سکے۔

-

دیگر اشارے یا پیٹرن کو ملا کر سگنل کے معیار کی مزید تصدیق کریں اور سگنل کی درستگی کو بہتر بنائیں۔

-

مختلف اقسام کے لیے الگ الگ پیرامیٹرز کو بہتر بنا کر حکمت عملی کی موافقت میں اضافہ کریں۔

خلاصہ

حکمت عملی کا مجموعی تصور واضح ہے، جس میں ریورسل پیٹرن اور ٹرینڈ ٹریکنگ انڈیکیٹرز کو مؤثر طریقے سے ملا کر قلیل مدتی ریورسل مواقع کی شناخت اور درمیانی سے طویل مدتی رجحانات کی پیروی کی جاتی ہے۔ پیرامیٹرز کی اصلاح اور طریقہ کار کے ڈیزائن کو بہتر بنا کر حکمت عملی کی منافع بخشی اور رسک کنٹرول کی صلاحیتوں کو مزید بڑھایا جا سکتا ہے۔

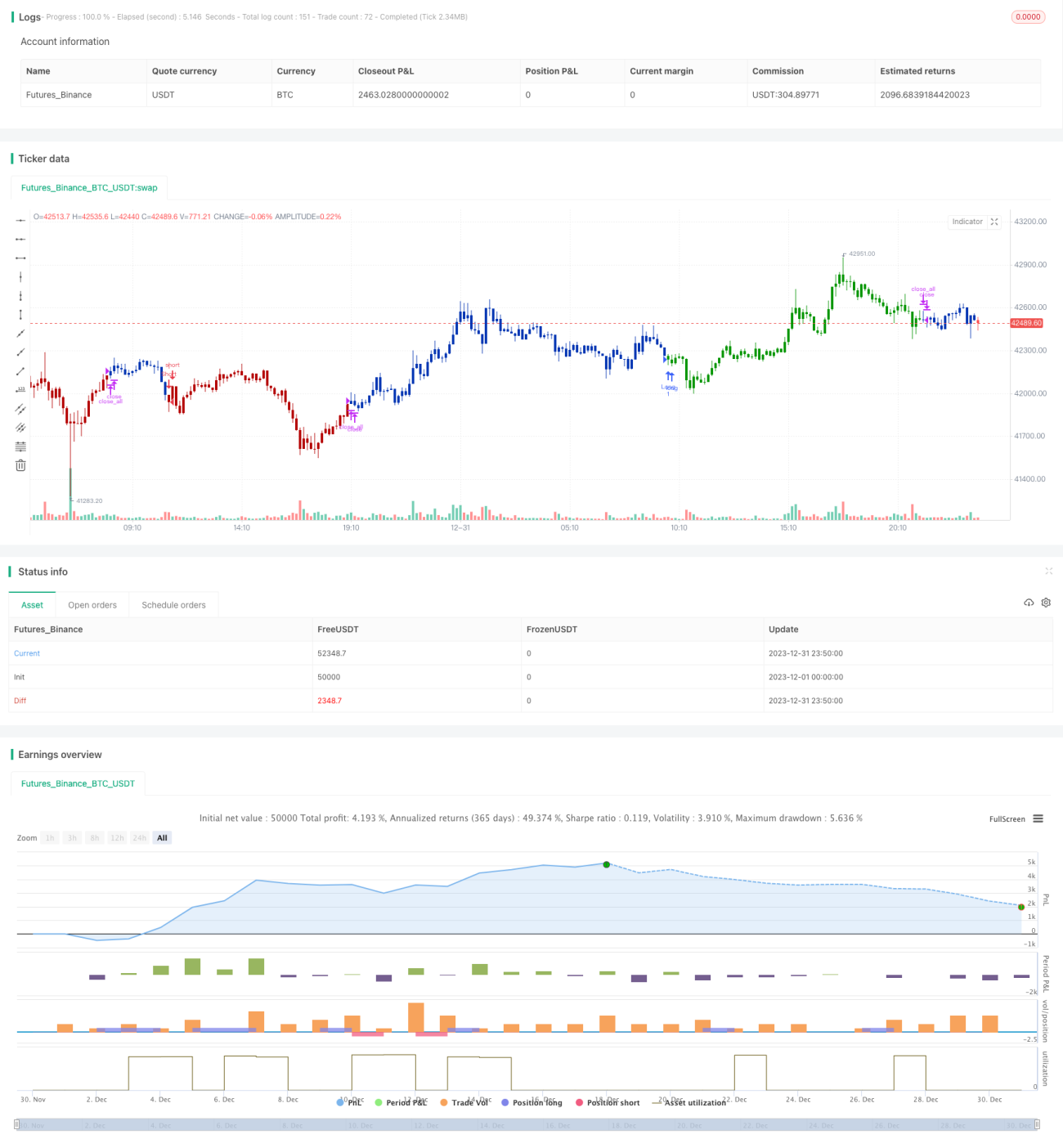

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 10/07/2021

// This is combo strategies for get a cumulative signal. - 1