انطباقی ذہین گرڈ تجارتی حکمت عملی

خلاصہ

یہ حکمت عملی TradingView پلیٹ فارم پر مبنی ایک خودکار ذہین گرڈ ٹریڈنگ حکمت عملی ہے، جو Pine Script v4 میں لکھی گئی ہے۔ یہ قیمت کے چارٹ پر اوورلے ہوتی ہے اور ایک متعین رینج کے اندر گرڈ تشکیل دیتی ہے تاکہ خرید و فروخت کے سگنلز پیدا کیے جا سکیں۔

حکمت عملی کا اصول

اہم خصوصیات

-

پرامڈنگ اور سرمایہ کا انتظام:

- ایک ہی سمت میں زیادہ سے زیادہ 14 بار اضافی پوزیشن کھولنے کی اجازت (پرامڈنگ)،

- نقد رقم پر مبنی حکمت عملی کے ذریعے پوزیشن کے سائز کا انتظام،

- تخمینی مقاصد کے لیے ابتدائی سرمایہ 100 ڈالر مقرر کیا گیا ہے،

- ہر لین دین پر 0.1% کمیشن وصول کیا جاتا ہے۔

-

گرڈ کی حد:

- صارف خودکار حساب شدہ حد یا دستی طور پر گرڈ کی بالائی اور زیریں حدود کا انتخاب کر سکتا ہے،

- خودکار حد قیمت کی حالیہ بلندیوں اور پستیوں یا سادہ موونگ ایوریج (SMA) سے اخذ کی جا سکتی ہے،

- صارف حد کے حساب کے لیے نظرثانی کی مدت متعین کر سکتا ہے اور حد کو بڑھانے یا گھٹانے کے لیے انحراف ایڈجسٹ کر سکتا ہے۔

-

گرڈ لائنیں:

- یہ حکمت عملی حد کے اندر حسب ضرورت تعداد میں گرڈ لائنوں کی اجازت دیتی ہے، تجویز کردہ تعداد 3 سے 15 کے درمیان ہے،

- گرڈ لائنیں بالائی اور زیریں حدود کے درمیان یکساں فاصلے پر رکھی جاتی ہیں۔

حکمت عملی کا منطق

-

پوزیشن میں داخلہ:

- جب قیمت گرڈ لائن سے نیچے آجاتی ہے اور اس گرڈ لائن سے منسلک کوئی کھلا آرڈر نہیں ہوتا، تو اسکرپٹ خرید کا آرڈر دیتا ہے،

- ہر خرید آرڈر کی مقدار ابتدائی سرمایہ کو گرڈ لائنوں کی تعداد سے تقسیم کر کے شمار کی جاتی ہے، اور موجودہ قیمت کے مطابق ایڈجسٹ کی جاتی ہے۔

-

پوزیشن سے نکلنا:

- جب قیمت اوپر کی کسی اونچی گرڈ لائن سے تجاوز کر جاتی ہے، اور اس سے نیچے والی گرڈ لائن سے منسلک کوئی کھلا آرڈر موجود ہوتا ہے، تو فروخت کا سگنل متحرک ہوتا ہے۔

-

خودکار موافق گرڈ:

- اگر خودکار حد استعمال کی جائے تو گرڈ بالائی اور زیریں حدود کا دوبارہ حساب لگا کر اور ان کے مطابق ایڈجسٹ ہو کر بدلتے ہوئے بازار کے حالات سے ہم آہنگ ہو جاتا ہے۔

فوائد کا تجزیہ

یہ حکمت عملی گرڈ ٹریڈنگ کی منظم کارکردگی اور موثر عملدرآمد کو یکجا کرتی ہے۔ پرامڈنگ کی اجازت اور سرمایہ کے انتظام کے ذریعے خطرے کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے۔ گرڈ خود بخود بازار کے مطابق ہو جاتا ہے، جو مختلف حالات میں کارآمد ہے۔ پیرامیٹرز کو ایڈجسٹ کیا جا سکتا ہے، جو مختلف ٹریڈنگ اسٹائلز کے مطابق ہوتا ہے۔

خطرات کا تجزیہ

قیمت کا گرڈ کی بالائی یا زیریں حدود سے باہر نکل جانا بڑے نقصان کا سبب بن سکتا ہے۔ پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کرنا چاہیے، یا نقصان کو روکنے کے لیے سٹاپ لاس استعمال کرنا چاہیے۔ اس کے علاوہ، زیادہ بار بار لین دین سے ٹرانزیکشن لاگت بڑھ جاتی ہے۔

بہتری کے ممکنہ راستے

سگنلز کو فلٹر کرنے کے لیے ٹرینڈ انڈیکیٹرز کو شامل کیا جا سکتا ہے یا گرڈ پیرامیٹرز کو بہتر بنایا جا سکتا ہے۔ انتہائی صورتحال کے خطرے سے بچنے کے لیے سٹاپ لاس بھی استعمال کیا جا سکتا ہے۔

خلاصہ

یہ حکمت عملی منظم طریقے سے خرید و فروخت کے مقامات پیدا کرتی ہے اور پوزیشنوں کا انتظام کرتی ہے۔ پیرامیٹرز کو ایڈجسٹ کرکے مختلف ترجیحات کے مطابق ڈھالا جا سکتا ہے۔ یہ گرڈ ٹریڈنگ کی ضابطہ بندی اور ٹرینڈ ٹریڈنگ کی لچک کو مربوط کرتی ہے، جس سے عملی دشواری کم ہوتی ہے اور ایک حد تک برداشت پیدا ہوتی ہے۔

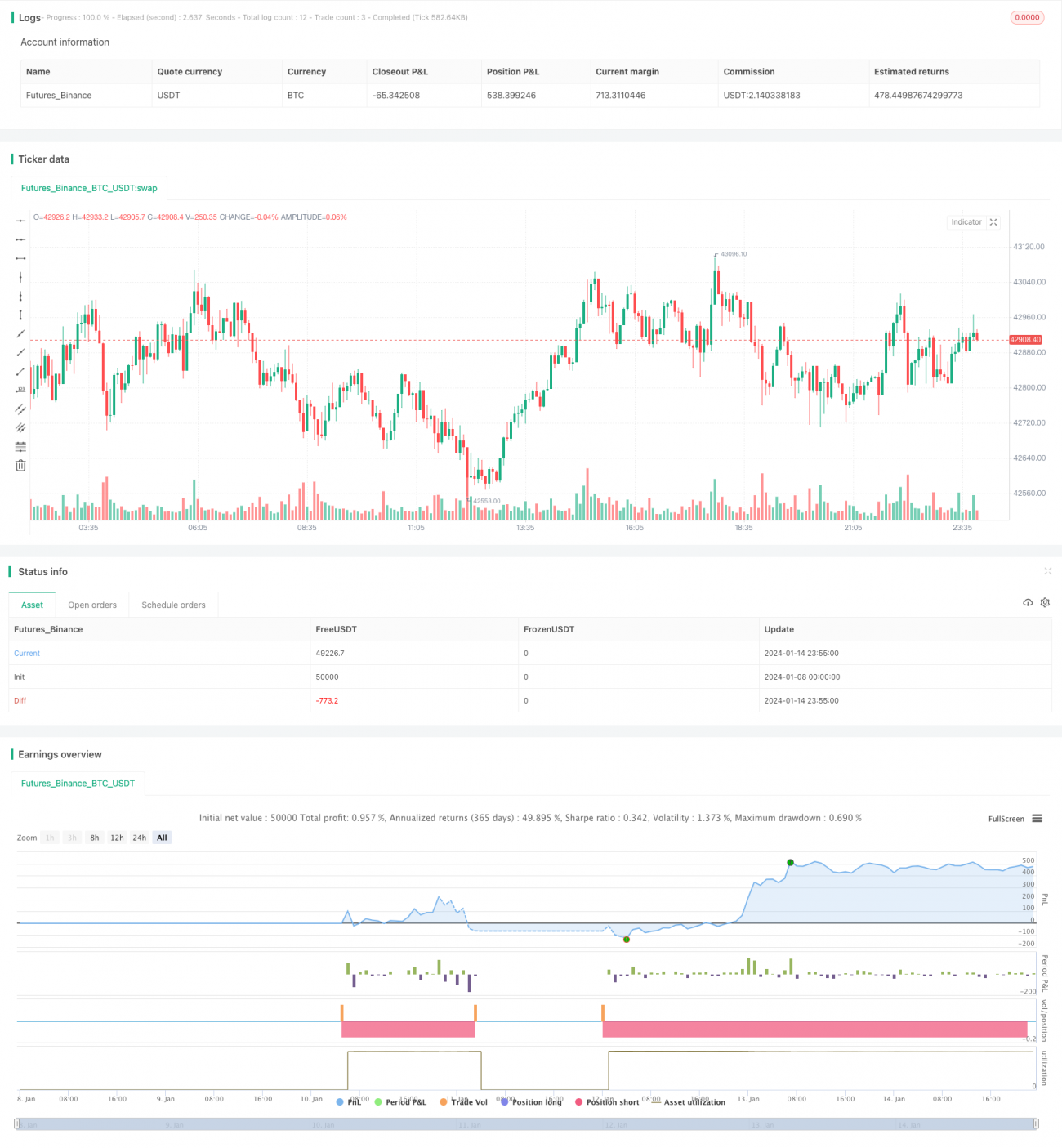

/*backtest

start: 2024-01-08 00:00:00

end: 2024-01-15 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("(IK) Grid Script", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving Average- 1