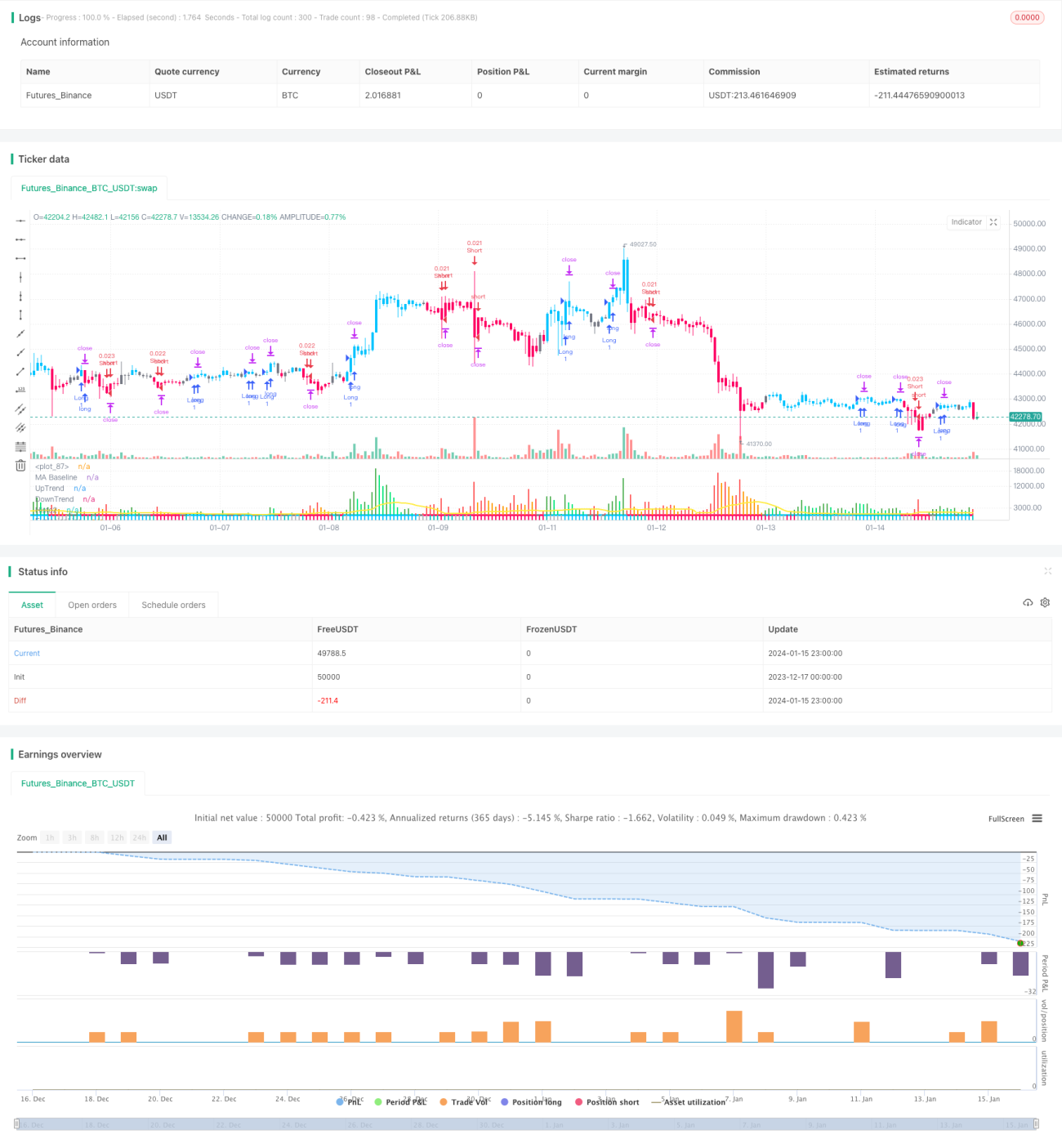

متعدد اشاروں کو یکجا کرنے والی جذباتی بریک آؤٹ حکمت عملی

خلاصہ

یہ حکمت عملی تین جذباتی اشاریوں یعنی QQE بہتر کردہ اشارے، SSL ہائبرڈ اشارے اور Waddah Attar بریک آؤٹ اشارے کو ملا کر تجارتی سگنلز تشکیل دیتی ہے۔ یہ ایک کثیر اشارے پر مبنی جذباتی بریک آؤٹ حکمت عملی ہے جو بریک آؤٹ سے پہلے مارکیٹ کے جذباتی پہلو کا اندازہ لگا کر جھوٹے بریک آؤٹ سے بچتی ہے، اور ایک بہتر بریک آؤٹ حکمت عملی ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی منطق تین اشاروں پر مبنی تجارتی فیصلے کرتا ہے:

QQE بہتر کردہ اشارہ: یہ اشارہ RSI اشارے میں بہتری لا کر اسے زیادہ حساس بناتا ہے، جس سے مارکیٹ کے جذبات کی سطح کا اندازہ لگایا جا سکتا ہے۔ اس حکمت عملی میں اسے نیچے کے ریورسل اور اوپر کے ریورسل کے سگنلز کی شناخت کے لیے استعمال کیا جاتا ہے۔

SSL ہائبرڈ اشارہ: یہ اشارہ متعدد متحرک اوسطوں کے بریک آؤٹ کو مجموعی طور پر دیکھ کر مارکیٹ کے آثار کا تعین کرتا ہے۔ اس حکمت عملی میں اسے چینل بریک آؤٹ کی صورتوں کی شناخت کے لیے استعمال کیا جاتا ہے۔

Waddah Attar بریک آؤٹ اشارہ: یہ اشارہ قیمت کے چینل کے اندر بریک آؤٹ کی شدت کا اندازہ لگاتا ہے۔ اس حکمت عملی میں اسے بریک آؤٹ کے وقت مناسب رفتار کو یقینی بنانے کے لیے استعمال کیا جاتا ہے۔

جب QQE اشارہ نیچے کے ریورسل کا سگنل دیتا ہے، SSL اشارہ چینل کی بالائی حد کے بریک آؤٹ کو ظاہر کرتا ہے، اور Waddah Attar اشارہ رفتار کے پھٹنے کا فیصلہ کرتا ہے، تو یہ حکمت عملی خریداری کا فیصلہ دیتی ہے۔ جب تینوں اشارے ایک ساتھ مخالف سگنل دیتے ہیں، تو فروخت کا فیصلہ کیا جاتا ہے۔

یہ حکمت عملی سٹاپ لاس اور ٹیک پروفٹ کے عین مطابق اخراج پوائنٹس بھی سیٹ کرتی ہے تاکہ منافع کو زیادہ سے زیادہ محفوظ کیا جا سکے۔ یہ ایک اعلیٰ معیار کی جذباتی محرک بریک آؤٹ حکمت عملی ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- متعدد اشاروں کو ملا کر مارکیٹ کے جذباتی پہلو کا اندازہ لگانا، جھوٹے بریک آؤٹ کے خطرے سے بچنا۔

- بیک وقت ریورسل اشارے، چینل اشارے اور رفتار کے اشارے پر غور کرنا، بریک آؤٹ کے وقت مارکیٹ کی تصدیق کو یقینی بنانا۔

- اعلیٰ درستگی کے ساتھ متحرک سٹاپ لاس کا استعمال کرتے ہوئے خطرے کو محدود کرنا اور منافع کو ٹریک کر کے بند کرنا۔

- پیرامیٹرز کو وسیع پیمانے پر بہتر بنانے کے بعد استحکام اچھا ہے، درمیانی سے طویل مدتی ہولڈنگ کے لیے موزوں ہے۔

- انڈیکیٹر پیرامیٹرز کو اپنی مرضی کے مطابق ترتیب دینے کی صلاحیت، مختلف مارکیٹ حالات کے مطابق ڈھالنے کے لیے حکمت عملی کے انداز کو تبدیل کرنا۔

خطرے کا تجزیہ

اس حکمت عملی میں بنیادی طور پر درج ذیل خطرات ہیں:

- جب مارکیٹ مسلسل کمزور ہوتی ہے، تو چھوٹے نقصان کے ساتھ بہت سے سودے ہو سکتے ہیں۔

- ایک ساتھ متعدد اشاروں پر انحصار کرنے کی وجہ سے، بعض مارکیٹوں میں یہ غیر معمولی طور پر ناکام ہو سکتی ہے۔

- QQE اشارے جیسے متعدد اشاروں میں پیرامیٹرز کے زیادہ بہتر ہونے کا خطرہ ہے، انہیں احتیاط سے ترتیب دینا چاہیے۔

- متحرک سٹاپ لاس خاص حالات میں صحیح طریقے سے کام نہیں کر سکتا۔

مندرجہ بالا خطرات سے نمٹنے کے لیے، تجویز ہے کہ اشاروں کے پیرامیٹرز کو مزید مستحکم بنانے کے لیے ایڈجسٹ کیا جائے، اور ہولڈنگ کی مدت کو مناسب طور پر بڑھایا جائے تاکہ منافع کی شرح بہتر ہو۔

بہتری کے راستے

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

- مختلف اشاروں کے پیرامیٹرز کو ایڈجسٹ کر کے انہیں زیادہ مستحکم یا زیادہ حساس بنایا جا سکتا ہے۔

- اتار چڑھاؤ پر مبنی پوزیشن سائز آپٹیمائزیشن ماڈیول شامل کیا جا سکتا ہے۔

- مشین لرننگ پر مبنی رسک مینجمنٹ ماڈیول شامل کیا جا سکتا ہے جو مارکیٹ کی حالت کا حقیقی وقت میں جائزہ لے۔

- ڈیپ لرننگ ماڈل کا استعمال کرتے ہوئے اشارے کی شکلوں کی پیش گوئی کر کے فیصلے کی درستگی بہتر بنائی جا سکتی ہے۔

- مختلف ٹائم فریموں کا تجزیہ شامل کر کے جھوٹے بریک آؤٹ کے امکانات کو کم کیا جا سکتا ہے۔

خلاصہ

اس حکمت عملی نے متعدد مرکزی جذباتی اشاروں کے فوائد کو یکجا کر کے ایک مؤثر جذباتی محرک بریک آؤٹ حکمت عملی تشکیل دی ہے۔ اس نے کامیابی کے ساتھ کم معیار کے بریک آؤٹ سے پیدا ہونے والے بہت سے خطرات سے بچا لیا ہے، اور ساتھ ہی اعلیٰ درستگی کے سٹاپ لاس کے تصور کے ذریعے منافع کو بند کرنے کی صلاحیت بھی رکھتی ہے۔ یہ ایک پختہ اور قابل اعتماد بریک آؤٹ حکمت عملی ہے جو سیکھنے اور استعمال کرنے کے قابل ہے۔ پیرامیٹرز کی مسلسل بہتری اور ماڈل کی پیش گوئی کے تعارف کے ساتھ، اس حکمت عملی سے مستقل اور مستحکم اضافی منافع حاصل ہونے کی امید ہے۔

- 1