صبر کے ساتھ رجحان کی پیروی کرنے والی حکمت عملی

جائزہ

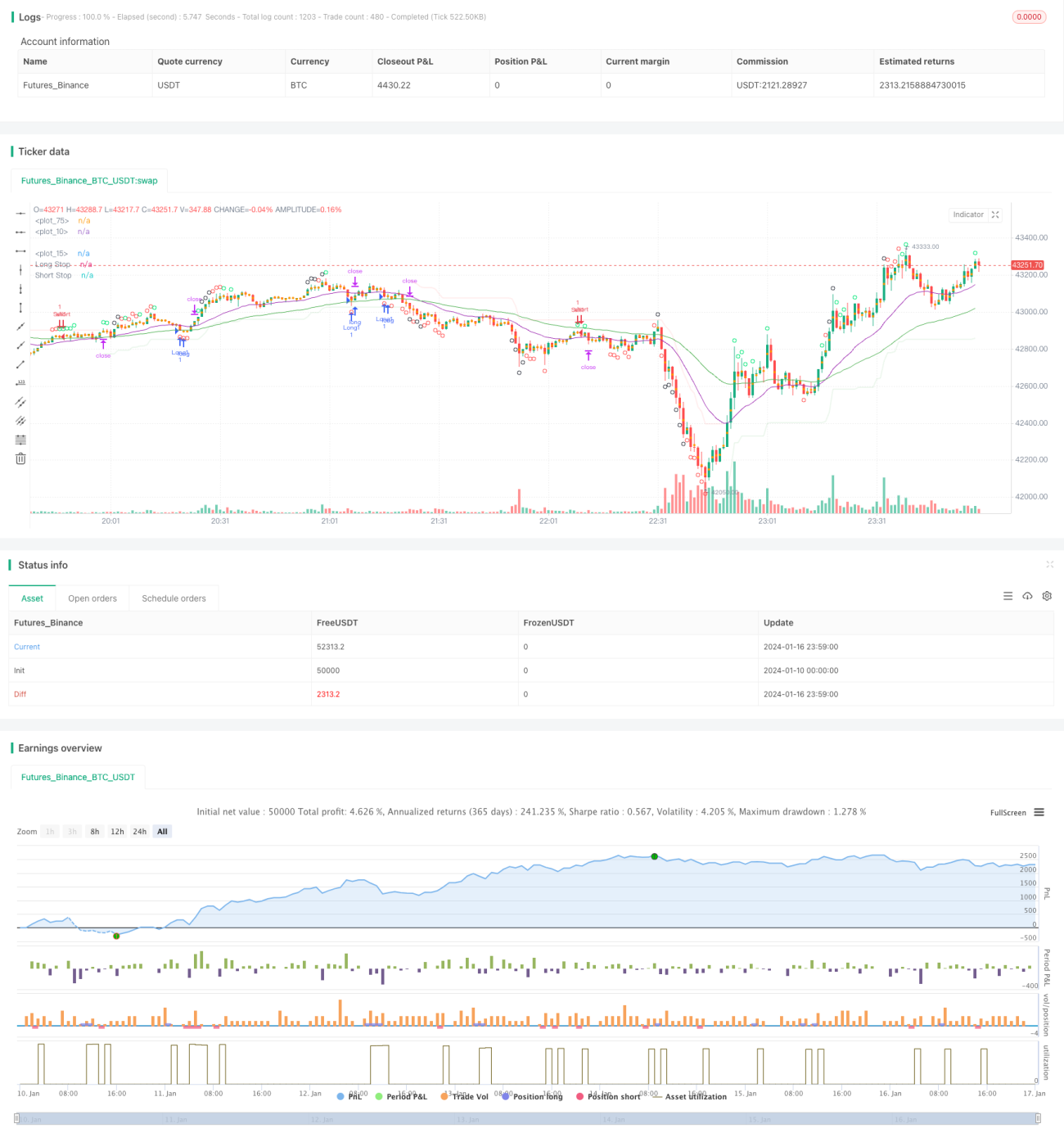

صبر کے ساتھ ٹرینڈ کو فالو کرنے کی حکمت عملی ایک ٹرینڈ فالو کرنے والی حکمت عملی ہے۔ یہ حرکت پذیر اوسط کے اشاریوں کے امتزاج سے رجحان کی سمت کا تعین کرتی ہے اور اوور باؤٹ/اوور سیلڈ انڈیکیٹر CCI کے ساتھ مل کر تجارتی سگنل جاری کرتی ہے۔ یہ حکمت عملی بڑے رجحان کا پیچھا کرتی ہے اور اتار چڑھاؤ والی مارکیٹ میں پھنسنے سے مؤثر طور پر بچ سکتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی 21 اور 55 ادوار کی EMA کے امتزاج سے رجحان کی سمت کا تعین کرتی ہے۔ جب قلیل مدتی EMA طویل مدتی EMA سے اوپر ہو تو اسے اوپر کا رجحان (اپ ٹرینڈ) کہا جاتا ہے، اور جب قلیل مدتی EMA طویل مدتی EMA سے نیچے ہو تو اسے نیچے کا رجحان (ڈاؤن ٹرینڈ) کہا جاتا ہے۔ CCI انڈیکیٹر اوور باؤٹ/اوور سیلڈ حالات کا تعین کرنے کے لیے استعمال ہوتا ہے۔ CCI کا -100 لائن کو اوپر سے عبور کرنا نیچے کے اوور سیلڈ سگنل ہے، اور 100 لائن کو نیچے سے عبور کرنا اوپر کے اوور باؤٹ سگنل ہے۔ CCI انڈیکیٹر کی مختلف اوور باؤٹ/اوور سیلڈ لائنوں کی بنیاد پر، حکمت عملی تین تجارتی سگنل کی شدت کی سطحوں میں تقسیم ہوتی ہے۔ جب اوپر کے رجحان کا تعین کیا جائے اور CCI انڈیکیٹر مضبوط نیچے کا اوور سیلڈ سگنل دے، تو لانگ پوزیشن میں داخل ہوں۔ جب نیچے کے رجحان کا تعین کیا جائے اور CCI انڈیکیٹر مضبوط اوپر کا اوور باؤٹ سگنل دے، تو شارٹ پوزیشن میں داخل ہوں۔ سٹاپ لاس SuperTrend انڈیکیٹر کے طور پر مقرر کیا جاتا ہے، اور منافع کا ہدف مقرر پوائنٹس پر طے کیا جاتا ہے۔

فوائد کا تجزیہ

- بڑے رجحان کا پیچھا کرنا، پھنسنے سے بچنا

- CCI انڈیکیٹر مؤثر طریقے سے ریورسل پوائنٹس کا تعین کر سکتا ہے

- SuperTrend سٹاپ لاس مناسب طریقے سے مقرر کیا گیا ہے

- مقررہ سٹاپ لاس اور مقررہ ٹیک پروفٹ، خطرہ قابل کنٹرول

خطرے کا تجزیہ

- بڑے رجحان کے تعین میں غلطی کا امکان

- CCI انڈیکیٹر کے غلط سگنل دینے کا امکان

- سٹاپ لاس پوائنٹ کے بہت کم یا بہت زیادہ ہونے کی وجہ سے غیر ضروری سٹاپ لاس کا امکان

- مقررہ ٹیک پروفٹ کے ساتھ مسلسل رجحان کی پیروی کرکے منافع حاصل کرنے میں ناکامی کا امکان

ان خطرات سے نمٹنے کے لیے، ہم EMA کے دورانیے کے پیرامیٹرز، CCI کے پیرامیٹرز اور سٹاپ لاس/ٹیک پروفٹ پوائنٹس کو ایڈجسٹ کرکے اصلاح کر سکتے ہیں۔ ساتھ ہی مزید انڈیکیٹرز متعارف کروانا جو حکمت عملی کے سگنلز کی تصدیق کریں، بہت ضروری ہے۔

اصلاح کی سمت

- مزید انڈیکیٹرز کے امتزاج کی جانچ کریں، بہتر رجحان کے تعین اور سگنل کی تصدیق کے لیے انڈیکیٹرز تلاش کریں۔

- ATR کا استعمال کرتے ہوئے متحرک سٹاپ لاس اور ٹیک پروفٹ کا استعمال کریں تاکہ رجحان کی بہتر پیروی اور خطرے پر قابو پایا جا سکے۔

- تاریخی ڈیٹا پر تربیت یافتہ مشین لرننگ ماڈل متعارف کروائیں تاکہ رجحان کے امکان کا تعین کیا جا سکے۔

- مختلف مصنوعات کے لیے پیرامیٹرز کو ایڈجسٹ اور بہتر بنائیں۔

خلاصہ

صبر کے ساتھ ٹرینڈ کو فالو کرنے کی حکمت عملی مجموعی طور پر ایک بہت ہی عملی ٹرینڈ فالو کرنے والی حکمت عملی ہے۔ یہ حرکت پذیر اوسطوں کا استعمال کرتے ہوئے بڑے رجحان کی سمت کا تعین کرتی ہے، CCI انڈیکیٹر ریورسل پوائنٹس کے سگنل تلاش کرتا ہے، اور سپر ٹرینڈ سٹاپ لاس مناسب طریقے سے مقرر کیا گیا ہے۔ پیرامیٹرز کو ایڈجسٹ کرنے اور متعدد انڈیکیٹرز کے امتزاج سے تصدیق کے ذریعے، اس حکمت عملی کو مزید بہتر بنایا جا سکتا ہے، اور یہ طویل مدتی حقیقی تجارت میں جانچ کے قابل ہے۔

- 1