زمان و مکان سے ماورا موفی اشارے کی حکمت عملی

خلاصہ

یہ ایک سادہ مقداری حکمت عملی ہے جو مارکیٹ میں "بڑی شارک" کی شناخت کے لیے مرفی انڈیکیٹر استعمال کرتی ہے۔ یہ 5 منٹ کے ٹائم فریم پر لاگو ہوتی ہے اور بنیادی طور پر کرپٹو کرنسی ٹریڈنگ کے لیے استعمال ہوتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی مرفی انڈیکیٹر کی 3 کی لمبائی استعمال کرتی ہے، جس میں اوور باؤٹ لائن 100 اور اوور سولڈ لائن 0 مقرر کی گئی ہے۔ حکمت عملی مرفی انڈیکیٹر کے اوور باؤٹ لیول تک پہنچنے کا انتظار کرتی ہے، جو مارکیٹ میں "بڑی شارک" کی موجودگی کی نشاندہی کرتی ہے۔ اگر اسی دن پہلے دو مرفی اوور باؤٹ پوائنٹس کے بعد بھی قیمت اپنی تیزی برقرار رکھتی ہے، تو یہ ایک لانگ انٹری سگنل ہے۔

جب مرفی انڈیکیٹر = 100 اور اگلی کینڈل بڑی بُلش ہو، تو لانگ انٹری کریں۔ سٹاپ لاس اس ٹریڈنگ دن کی سب سے کم قیمت پر رکھیں، اور ٹیک پروفٹ انٹری کے بعد 60 منٹ میں مقرر کریں۔

شارٹ ٹریڈنگ کے لیے آئینہ دار منطق استعمال کی جا سکتی ہے۔ یعنی جب مرفی انڈیکیٹر اوور سولڈ تک پہنچ جائے اور اگلی کینڈل بڑی بیئرش ہو، تو شارٹ انٹری کریں۔

حکمت عملی کے فوائد

-

مرفی انڈیکیٹر کا استعمال مارکیٹ میں "بڑی شارک" کے ممکنہ اسٹاک جمع کرنے کے رویے کو مؤثر طریقے سے شناخت کرتا ہے، جو مزید بڑھنے کا امکان رکھتے ہیں۔

-

کینڈل باڈی کی طاقت والے بریک آؤٹ پوائنٹس کا استعمال بہت سے جھوٹے بریک آؤٹس کو فلٹر کر سکتا ہے۔

-

ایس ایم اے فلٹر کے ساتھ مل کر، گرتی ہوئی ٹرینڈ والے اسٹاک کی خریداری سے بچا جا سکتا ہے، جس سے تجارتی خطرہ کم ہوتا ہے۔

-

انٹرا ڈے الٹرا شارٹ ٹرم طریقہ کار استعمال کرتے ہوئے، 60 منٹ کا ٹیک پروفٹ فوری منافع حاصل کرنے اور ڈرا ڈاؤن کے امکانات کو کم کرنے میں مدد کرتا ہے۔

حکمت عملی کے خطرات

-

مرفی انڈیکیٹر جھوٹے سگنل پیدا کر سکتا ہے، جس سے غیر ضروری نقصان ہو سکتا ہے۔ پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کیا جا سکتا ہے یا دیگر انڈیکیٹرز شامل کیے جا سکتے ہیں۔

-

60 منٹ کا الٹرا شارٹ ٹرم آپریشن طریقہ بہت زیادہ جارحانہ ہو سکتا ہے اور زیادہ اتار چڑھاؤ والے اسٹاک کے لیے موزوں نہیں ہے۔ ٹیک پروفٹ کے وقت کو ایڈجسٹ کیا جا سکتا ہے یا مووِنگ سٹاپ لاس استعمال کیا جا سکتا ہے۔

-

بڑے معاشی واقعات کے دوران مارکیٹ کے اثرات کے خطرے کو مدنظر نہیں رکھا گیا ہے۔ ایسی صورت میں حکمت عملی کو روک دیا جانا چاہیے، اور مارکیٹ کے دوبارہ مستحکم ہونے کے بعد جاری رکھا جانا چاہیے۔

حکمت عملی کی اصلاح کے رخ

-

پیرامیٹرز کے مختلف امتزاج کی جانچ کی جا سکتی ہے، جیسے مرفی انڈیکیٹر کی لمبائی کو ایڈجسٹ کرنا، ایس ایم اے سائیکل پیرامیٹرز کو بہتر بنانا وغیرہ۔

-

دوسرے انڈیکیٹرز جیسے بولنگر بینڈ، کے ڈی انڈیکیٹر وغیرہ شامل کرکے دیکھا جا سکتا ہے کہ آیا سگنلز کی درستگی بہتر ہوتی ہے۔

-

سٹاپ لاس کی حد کو مناسب طریقے سے بڑھانے سے فی ٹریڈ زیادہ منافع حاصل کیا جا سکتا ہے یا نہیں۔

-

اس حکمت عملی کے فریم ورک پر مبنی دیگر ٹائم فریمز جیسے 15 منٹ یا 30 منٹ کے ورژن تیار کرنے کی کوشش کی جا سکتی ہے۔

خلاصہ

یہ حکمت عملی مجموعی طور پر بہت سادہ اور سمجھنے میں آسان ہے، اور اس کا بنیادی تصور کلاسک "بڑی شارک" کی پیروی کرنے والی حکمت عملیوں سے ملتا ہے۔ مرفی انڈیکیٹر کے اوور باؤٹ اور اوور سولڈ اہم نکات کو شناخت کرکے، اور کینڈل باڈی کے ذریعے فلٹر کرکے، بہت سے شور کو ختم کیا جا سکتا ہے۔ ایس ایم اے فلٹر کے اضافے نے حکمت عملی کے استحکام کو مزید بڑھا دیا ہے۔

60 منٹ کا الٹرا شارٹ ٹرم طریقہ تیزی سے منافع کما سکتا ہے، لیکن اس میں زیادہ آپریشنل خطرہ بھی ہے۔ مجموعی طور پر، یہ ایک بہت قیمتی مقداری حکمت عملی کا نمونہ ہے جو گہرائی سے تحقیق اور اصلاح کے لائق ہے، اور ہمیں حکمت عملی کی ترقی کے لیے قیمتی خیالات فراہم کرتا ہے۔

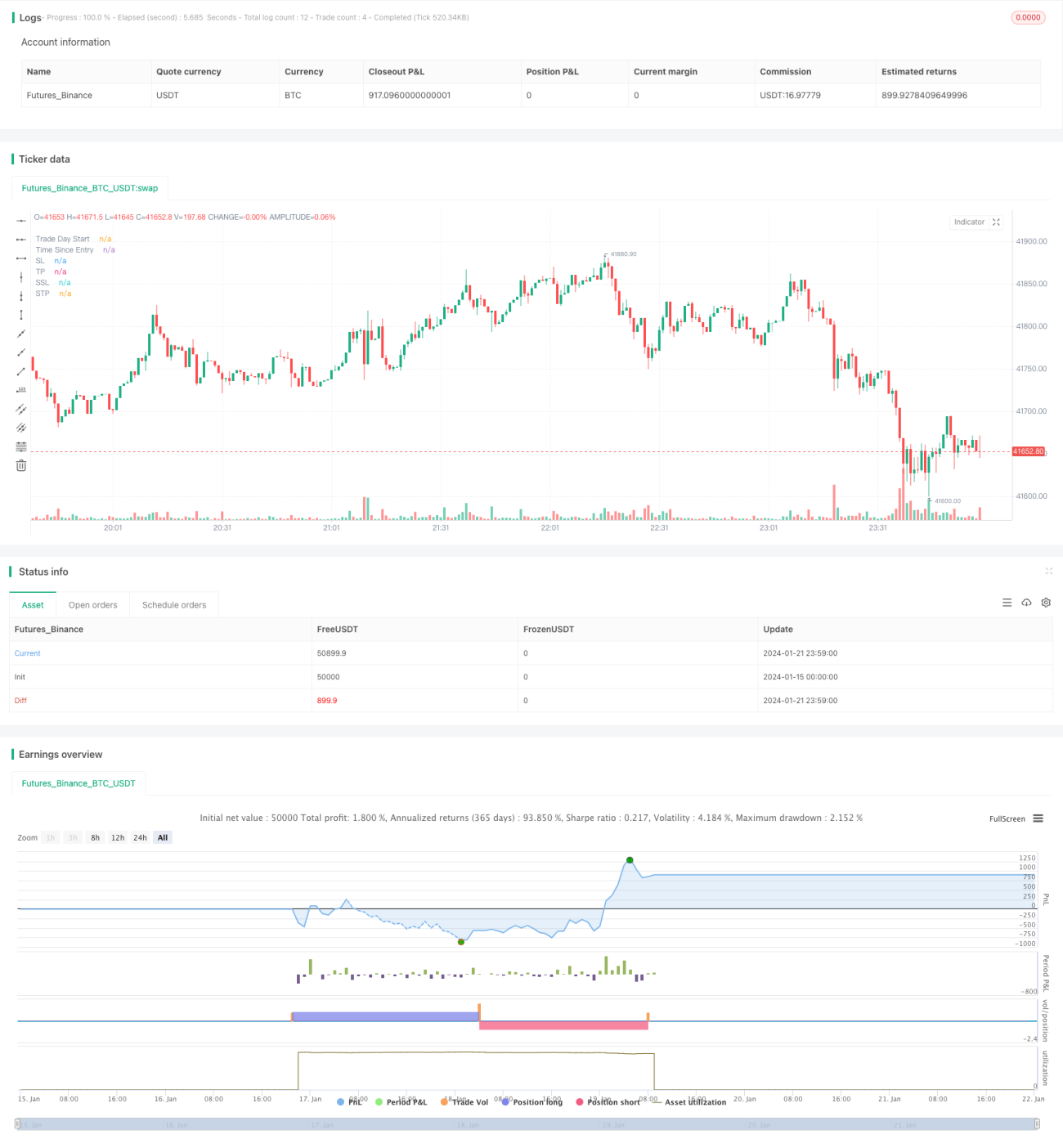

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1