مومینٹم موونگ ایوریج پر مبنی تجارتی حکمت عملی

جائزہ

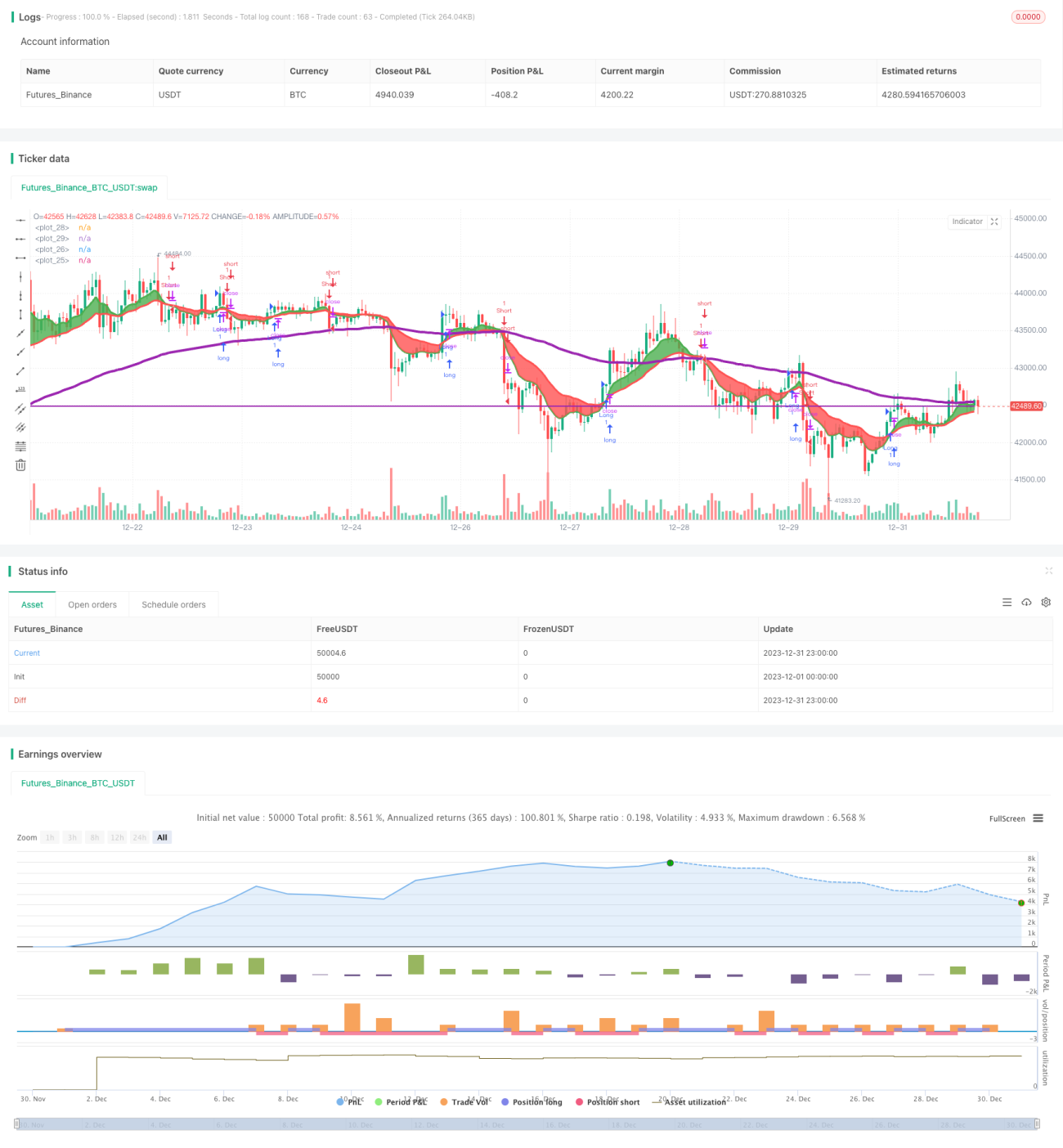

یہ حکمت عملی تیز اور سست حرکت پذیر اوسط کی کراس اوور پر مبنی ہے تاکہ مارکیٹ کے رجحان اور خرید و فروخت کے مقامات کا تعین کیا جا سکے۔ جب تیز EMA (8 دن) سست EMA (21 دن) کو اوپر سے کراس کرتا ہے تو مارکیٹ میں اوپر کی طرف رجحان سمجھا جاتا ہے اور خرید کا سگنل پیدا ہوتا ہے۔ جب تیز EMA سست EMA کو نیچے سے کراس کرتا ہے تو مارکیٹ میں نیچے کی طرف رجحان سمجھا جاتا ہے اور فروخت کا سگنل پیدا ہوتا ہے۔ حکمت عملی میں نقصان روکنے اور منافع کم کرنے کی قیمتیں بھی مقرر کی گئی ہیں تاکہ خطرے کا انتظام کیا جا سکے۔

حکمت عملی کا اصول

یہ حکمت عملی تیز EMA (8 دن کی لائن) اور سست EMA (21 دن کی لائن) کے کراس اوور کا استعمال کرتے ہوئے مارکیٹ کے رجحان کا تعین کرتی ہے۔ مخصوص منطق مندرجہ ذیل ہے:

- 8 دن کے EMA اور 21 دن کے EMA کا حساب لگائیں

- جب 8 دن کا EMA 21 دن کے EMA کو اوپر سے کراس کرتا ہے تو یہ مارکیٹ میں تبدیلی اور اوپر کی طرف رجحان کا آغاز سمجھا جاتا ہے

- جب 8 دن کا EMA 21 دن کے EMA کو نیچے سے کراس کرتا ہے تو یہ مارکیٹ میں تبدیلی اور نیچے کی طرف رجحان کا آغاز سمجھا جاتا ہے

- اوپر کی طرف رجحان میں خرید کا سگنل پیدا ہوتا ہے؛ نیچے کی طرف رجحان میں فروخت کا سگنل پیدا ہوتا ہے

- ہر آرڈر کے خطرے کا انتظام کرنے کے لیے نقصان روکنے اور منافع کم کرنے کی قیمتیں مقرر کریں

یہ حکمت عملی رفتار کے اشارے اور رجحان کے تجزیہ کو یکجا کرتی ہے، جو مارکیٹ کی سمت اور الٹنے کے مقامات کو مؤثر طریقے سے پکڑ سکتی ہے۔ تیز اور سست EMA کا کراس اوور ہموار حرکت پذیر اوسط کے ساتھ مل کر کچھ شور والے تجارتی سگنلز کو فلٹر کر سکتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل اہم فوائد ہیں:

- تیز EMA اور سست EMA کا کراس اوور مارکیٹ کے رجحان اور خرید و فروخت کے مقامات کو مؤثر طریقے سے طے کر سکتا ہے

- حکمت عملی کے پیرامیٹرز میں بہتری کی گنجائش ہے، EMA ادوار کو مزید ایڈجسٹ کیا جا سکتا ہے

- رفتار کے اشارے کے ساتھ مل کر، شور کے سگنلز کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے

- نقصان روکنے اور منافع کم کرنے کی منطق مقرر کر کے خطرے کو فعال طور پر کنٹرول کیا جا سکتا ہے

مجموعی طور پر، یہ حکمت عملی رجحان اور رفتار کے اشارے کو یکجا کرتی ہے، اور پیرامیٹرز کو ایڈجسٹ کر کے مختلف مارکیٹ کے حالات کے مطابق ڈھالا جا سکتا ہے، یہ ایک نسبتاً لچکدار قلیل مدتی تجارتی حکمت عملی ہے۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- اتار چڑھاؤ والی مارکیٹ میں، EMA کراس اوور سگنلز بار بار آتے ہیں، جس کی وجہ سے غلط تجارت زیادہ ہوتی ہے

2.ギャップ (قیمت کے خلاء) کی صورت حال کو مؤثر طریقے سے نہیں سنبھال سکتا - بڑے درجے کے طویل مدتی رجحان پر غور نہیں کیا گیا

ان خطرات کے لیے، ہم درج ذیل پہلوؤں سے بہتری لا سکتے ہیں:

- دیگر اشارے جیسے بولنگر بینڈز، KDJ وغیرہ شامل کریں تاکہ غلط سگنلز کے امکانات کم ہوں

- طویل مدتی رجحان کا تعین کرنے کے لیے بڑے درجے کے دورانیے کے اشارے کو شامل کریں

- پیرامیٹرز کو بہتر بنائیں، EMA کی لمبائی کو ایڈجسٹ کریں تاکہ مختلف مارکیٹ کے حالات کے مطابق ڈھالا جا سکے

- تجارت میں انسانی مداخلت کریں تاکہギャップ (قیمت کے خلاء) کی وجہ سے نقصان روکنے کی حد سے زیادہ بڑے نقصان سے بچا جا سکے

بہتری کی سمت

اس حکمت عملی میں بہتری کی کافی گنجائش ہے، بنیادی طور پر درج ذیل سمتوں سے بہتری لا سکتے ہیں:

- EMA کے دورانیے کے پیرامیٹرز کو بہتر بنائیں، تاریخی ڈیٹا پر مختلف پیرامیٹرز کے منافع کی شرح کو جانچیں

- فلٹرنگ کے لیے دیگر تکنیکی اشارے جیسے KDJ، MACD وغیرہ شامل کریں تاکہ حکمت عملی کی درستگی بڑھے

- نقصان روکنے اور منافع کم کرنے کی ترتیبات کو بہتر بنائیں تاکہ وہ مارکیٹ کی خصوصیات کے لیے زیادہ موزوں ہوں

- مشین لرننگ کے طریقوں سے خود بخود پیرامیٹرز کو بہتر بنائیں

یہ بہتری کے اقدامات حکمت عملی کے استحکام، موافقت اور منافع کی صلاحیت کو بہت بڑھا سکتے ہیں۔

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک عام قلیل مدتی تجارتی حکمت عملی ہے جو رجحان کی پیروی اور رفتار کے اشارے کے کراس اوور پر مبنی ہے۔ یہ EMA تیز اور سست لائنوں کے کراس اوور اور نقصان روکنے/منافع کم کرنے کی منطق کو یکجا کرتی ہے، جس سے مارکیٹ کی سمت کے مواقع کو تیزی سے پکڑا جا سکتا ہے۔ اس حکمت عملی میں بہتری کی کافی گنجائش ہے، اگر اس میں مزید معاون اشارے، خودکار پیرامیٹر آپٹیمائزیشن جیسے ذرائع شامل کیے جائیں تو حکمت عملی کی کارکردگی مزید مستحکم اور شاندار ہو سکتی ہے۔ یہ حکمت عملی ان سرمایہ کاروں کے لیے موزوں ہے جو مارکیٹ کے بارے میں کچھ علم رکھتے ہیں اور بار بار تجارت کرنے کو تیار ہیں۔

- 1