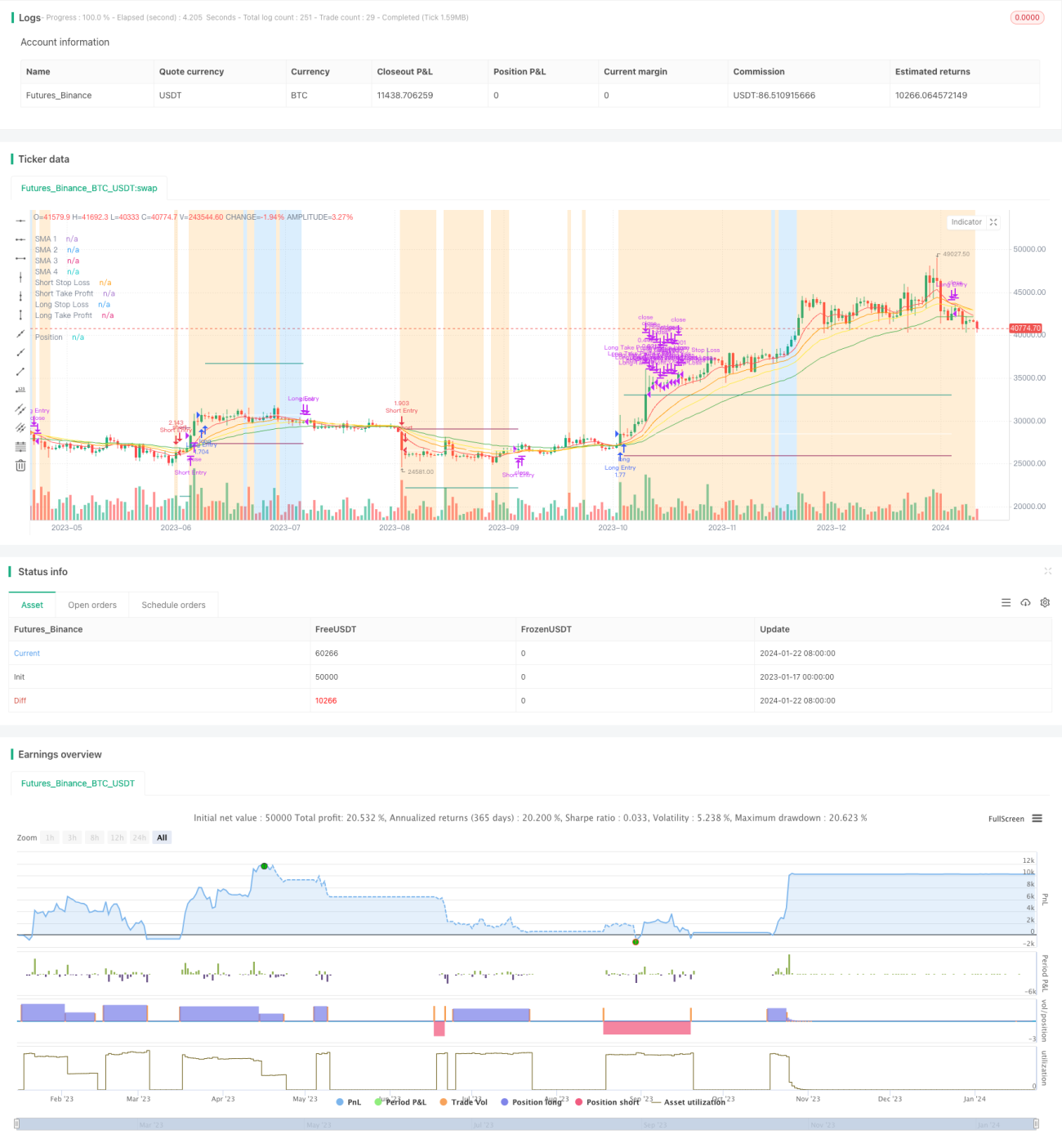

متحرک اوسط پر مبنی رجحان پیروی کی حکمت عملی

جائزہ

یہ حکمت عملی ایک سادہ ٹرینڈ فالو کرنے والی حکمت عملی ہے جو موونگ اوسط پر مبنی ہے۔ یہ مختلف ادوار کی موونگ اوسطوں کے درمیان سائز کے تعلق کا موازنہ کرکے موجودہ رجحان کی سمت اور اس کے دورانیے کا تعین کرتی ہے۔ جب قلیل مدتی اوسط طویل مدتی اوسط کو نیچے سے اوپر کرتی ہے تو لمبی پوزیشن (لانگ) لی جاتی ہے، اور جب قلیل مدتی اوسط طویل مدتی اوسط کو اوپر سے نیچے کرتی ہے تو چھوٹی پوزیشن (شارٹ) لی جاتی ہے۔ اس کے علاوہ، حکمت عملی میں خطرے کو کنٹرول کرنے کے لیے اسٹاپ لاس اور ٹیک پرافٹ پوائنٹس بھی مقرر کیے گئے ہیں۔

حکمت عملی کا اصول

یہ حکمت عملی مختلف ادوار کی چار موونگ اوسطیں استعمال کرتی ہے: 5 دن، 10 دن، 15 دن اور 25 دن۔ ان چار اوسطوں کو MA1، MA2، MA3 اور MA4 کہا جاتا ہے۔ ان میں MA1 سب سے چھوٹی اور MA4 سب سے بڑی ہے۔

جب MA1 > MA2 > MA3 > MA4 ہو تو اس کا مطلب ہے کہ قیمت اوپر کی طرف رجحان میں ہے، اس وقت لمبی پوزیشن لی جاتی ہے۔ جب MA1 < MA2 < MA3 < MA4 ہو تو اس کا مطلب ہے کہ قیمت نیچے کی طرف رجحان میں ہے، اس وقت چھوٹی پوزیشن لی جاتی ہے۔

لمبی اور چھوٹی پوزیشن کھولنے کی شرط میں ATR اسٹاپ فلٹر بھی شامل ہے، یعنی ATR کی قدر ATR کے 40 دورانیے کے سادہ موونگ اوسط سے زیادہ ہونی چاہیے، اس سے قیمت کے اتار چڑھاؤ بہت کم ہونے پر غلط سگنل دینے سے بچا جا سکتا ہے۔

حکمت عملی کے فوائد

اس حکمت عملی کے درج ذیل فوائد ہیں:

- خیال سادہ اور سمجھنے میں آسان ہے، نافذ کرنا آسان ہے۔

- متعدد موونگ اوسطوں کا استعمال کرکے رجحان کی سمت کا تعین قابل اعتماد ہے۔

- ٹیک پرافٹ اور اسٹاپ لاس پوائنٹس مقرر کرنے سے ایک ٹریڈ میں زیادہ سے زیادہ نقصان کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے۔

- ATR اسٹاپ فلٹر قیمت کے اتار چڑھاؤ بہت کم ہونے پر غلط سگنل دینے سے روکتا ہے۔

خطرے کا تجزیہ

اس حکمت عملی میں درج ذیل خطرات بھی موجود ہیں:

- بہت زیادہ اتار چڑھاؤ والی مارکیٹ میں غلط سگنل پیدا ہونے کا امکان ہے۔

- پیرامیٹر کی ترتیبات (موونگ اوسط کے ادوار وغیرہ) اگر مناسب نہ ہوں تو حکمت عملی کی کارکردگی خراب ہو سکتی ہے۔

- بنیادی عوامل اور اہم خبروں کے قیمت پر اثرات کو مدنظر نہیں رکھا گیا۔

ان خطرات کو کم کرنے کے لیے، پیرامیٹرز کو مناسب طریقے سے بہتر بنایا جا سکتا ہے، یا حکمت عملی کے استحکام کو بڑھانے کے لیے دیگر فلٹر کی شرائط شامل کی جا سکتی ہیں۔

بہتری کے رخ

اس حکمت عملی کی بہتری کے درج ذیل رخ ہیں:

- موونگ اوسط کے مختلف دورانیے کے پیرامیٹرز کے مختلف مجموعوں کی جانچ کرنا، بہترین پیرامیٹرز تلاش کرنا۔

- دیگر تکنیکی اشاریوں جیسے MACD، KDJ وغیرہ کے فلٹرز شامل کرنا تاکہ سگنل کی وشوسنییتا کا تعین کیا جا سکے۔

- ٹریڈنگ والیوم فلٹر شامل کرنا، صرف اس وقت ٹریڈ کرنا جب والیوم بڑھا ہوا ہو۔

- مختلف پروڈکٹس کے پیرامیٹر کے فرق کے مطابق تفصیلی پروڈکٹ کے لحاظ سے پیرامیٹر کی بہتری کرنا۔

- سگنل کا فیصلہ کرنے کے لیے مشین لرننگ الگورتھم شامل کرنا۔

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک نسبتاً سادہ ٹرینڈ فالو کرنے والی حکمت عملی ہے، جو موونگ اوسط کے ذریعے رجحان کی سمت کا تعین کرتی ہے اور خطرے کی سطح کو کنٹرول کرنے کے لیے مناسب ٹیک پرافٹ اور اسٹاپ لاس مقرر کرتی ہے۔ حکمت عملی میں بہتری کی کافی گنجائش ہے، پیرامیٹرز کو ایڈجسٹ کرنے، اضافی فلٹرز شامل کرنے وغیرہ کے ذریعے حکمت عملی کے استحکام اور منافع کی صلاحیت کو مزید بڑھایا جا سکتا ہے۔

- 1