بے ترتیب داخلے پر مبنی مرکب سٹاپ لاس اور ٹیک پرافٹ حکمت عملی

خلاصہ

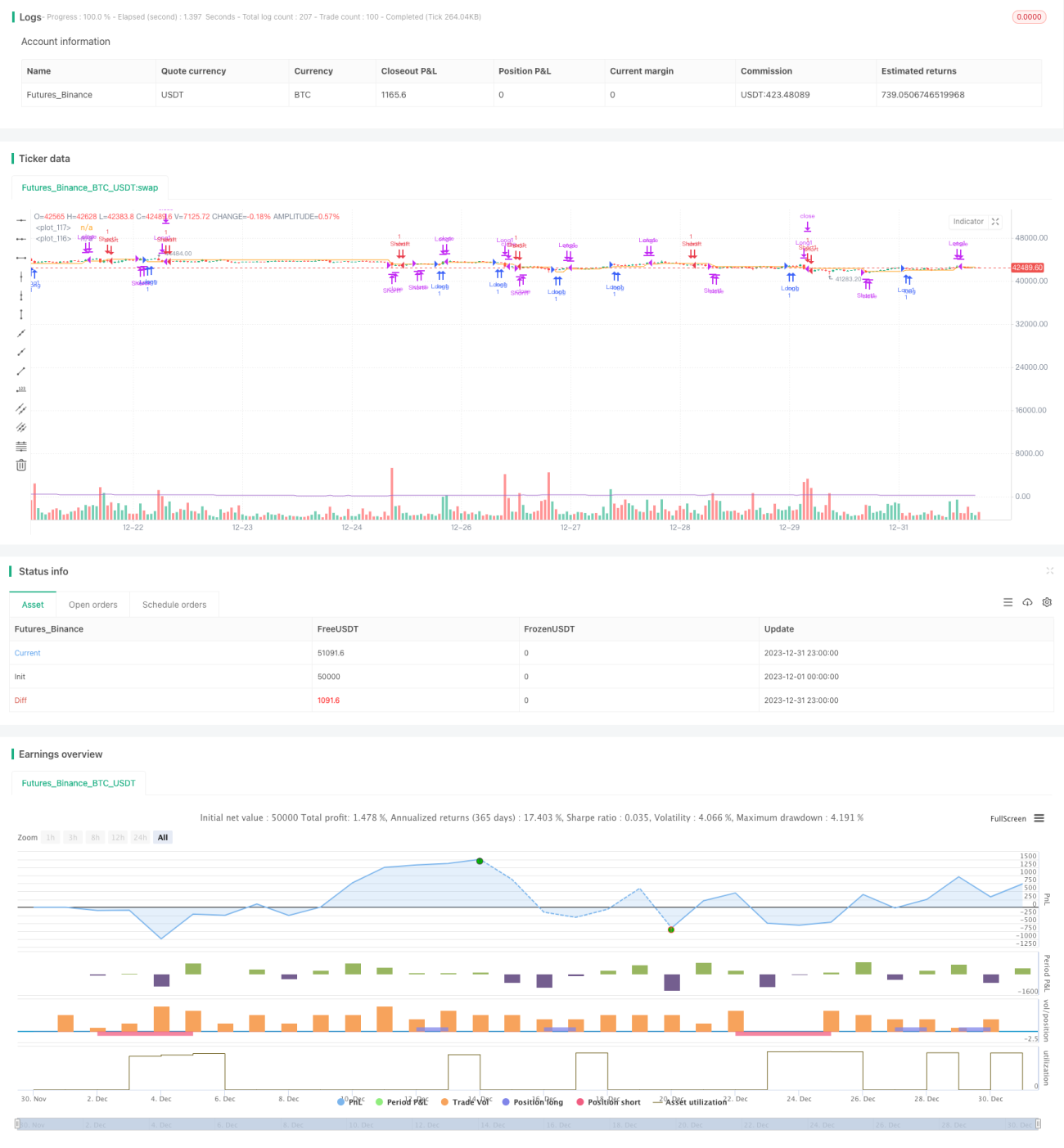

اس حکمت عملی کا بنیادی خیال بے ترتیب نمبروں کے ذریعے داخلے کے مقام کا تعین کرنا ہے، اور خطرے کو منظم کرنے کے لیے تین منافع کے اہداف اور ایک نقصان کو روکنے کا مقام مقرر کیا گیا ہے، تاکہ ہر تجارت کے منافع اور نقصان کو کنٹرول کیا جا سکے۔

حکمت عملی کا اصول

یہ حکمت عملی بے ترتیب نمبر rd_number_entry کو 11 سے 13 کے درمیان استعمال کرتی ہے تاکہ لانگ پوزیشن میں داخلے کا مقام طے کیا جا سکے، اور rd_number_exit کو 20 سے 22 کے درمیان استعمال کرتی ہے تاکہ پوزیشن بند کی جا سکے۔ لانگ کرنے کے بعد، اسٹاپ لاسس داخلے کی قیمت میں سے atr(14)* slx کو منہا کر کے رکھا جاتا ہے۔ اسی کے ساتھ تین منافع کے اہداف مقرر کیے گئے ہیں: پہلا ہدف داخلے کی قیمت میں atr(14)* tpx کا اضافہ، دوسرا ہدف داخلے کی قیمت میں 2* tpx کا اضافہ، اور تیسرا ہدف داخلے کی قیمت میں 3* tpx کا اضافہ۔ شارٹ پوزیشن کا اصول بھی اسی طرح ہے، فرق صرف یہ ہے کہ داخلے کا فیصلہ rd_number_entry کی مختلف قدروں پر مبنی ہے، اور منافع اور نقصان روکنے کی سمت مخالف ہے۔

یہ حکمت عملی tpx (منافع کا عدد) اور slx (نقصان روکنے کا عدد) کو ایڈجسٹ کرکے خطرے کو کنٹرول کر سکتی ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- بے ترتیب داخلے کا استعمال کر کے اوور فٹنگ کے امکان کو کم کیا جا سکتا ہے۔

- متعدد منافع اور نقصان روکنے کے مقامات مقرر کر کے ایک ہی تجارت کے خطرے کو کنٹرول کیا جا سکتا ہے۔

- ATR کا استعمال منافع اور نقصان روکنے کے مقامات مقرر کرنے کے لیے مارکیٹ کے اتار چڑھاؤ کی بنیاد پر منافع اور نقصان کے نکات طے کرنے میں مدد کرتا ہے۔

- اعداد کو ایڈجسٹ کر کے تجارتی خطرے کو کنٹرول کیا جا سکتا ہے۔

خطرے کا تجزیہ

اس حکمت عملی میں درج ذیل خطرات بھی موجود ہیں:

- بے ترتیب داخلے کی وجہ سے مارکیٹ کی حرکت سے محروم رہ سکتے ہیں۔

- بہت چھوٹا نقصان روکنے کا مقام بار بار اسٹاپ آؤٹ ہونے کا سبب بن سکتا ہے۔

- منافع کا ہدف بہت بڑا ہونے کی وجہ سے کافی منافع حاصل نہیں ہو سکتا۔

- پیرامیٹرز کا نامناسب انتخاب نقصان کو بڑھا سکتا ہے۔

منافع اور نقصان روکنے کے اعداد کو ایڈجسٹ کرکے اور بے ترتیب داخلے کے منطق کو بہتر بنا کر خطرے کو کم کیا جا سکتا ہے۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- بے ترتیب داخلے کے منطق کو بہتر بنانا اور رجحان کے اشاروں کے ساتھ جوڑنا۔

- منافع اور نقصان روکنے کے اعداد کو بہتر بنانا تاکہ منافع اور نقصان کا تناسب زیادہ معقول ہو۔

- پوزیشن کے سائز پر کنٹرول شامل کرنا، مختلف مراحل میں مختلف منافع کے ہدف استعمال کرنا۔

- مشین لرننگ الگورتھم کے ساتھ پیرامیٹرز کو بہتر بنانا۔

خلاصہ

یہ حکمت عملی بے ترتیب داخلے پر مبنی ہے، اور ایک ہی تجارت کے خطرے کو کنٹرول کرنے کے لیے متعدد منافع اور نقصان روکنے کے مقامات رکھے گئے ہیں۔ بے ترتیب ہونے کی وجہ سے اوور فٹنگ کا امکان کم ہو جاتا ہے، اور پیرامیٹر کی اصلاح کے ذریعے تجارتی خطرے کو کم کیا جا سکتا ہے۔ مستقبل میں بہتری کی بہت گنجائش ہے، اس پر مزید تحقیق کرنا قابل قدر ہے۔

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Random Strategy with 3 TP levels and SL", overlay=true,max_bars_back = 50)

tpx = input(defval = 0.8, title = 'Atr multiplication for TPs?')- 1