ایک حکمت عملی جو متعدد تکنیکی اشاریوں کا استعمال کرتے ہوئے مقداری تجارت کرتی ہے۔

خلاصہ

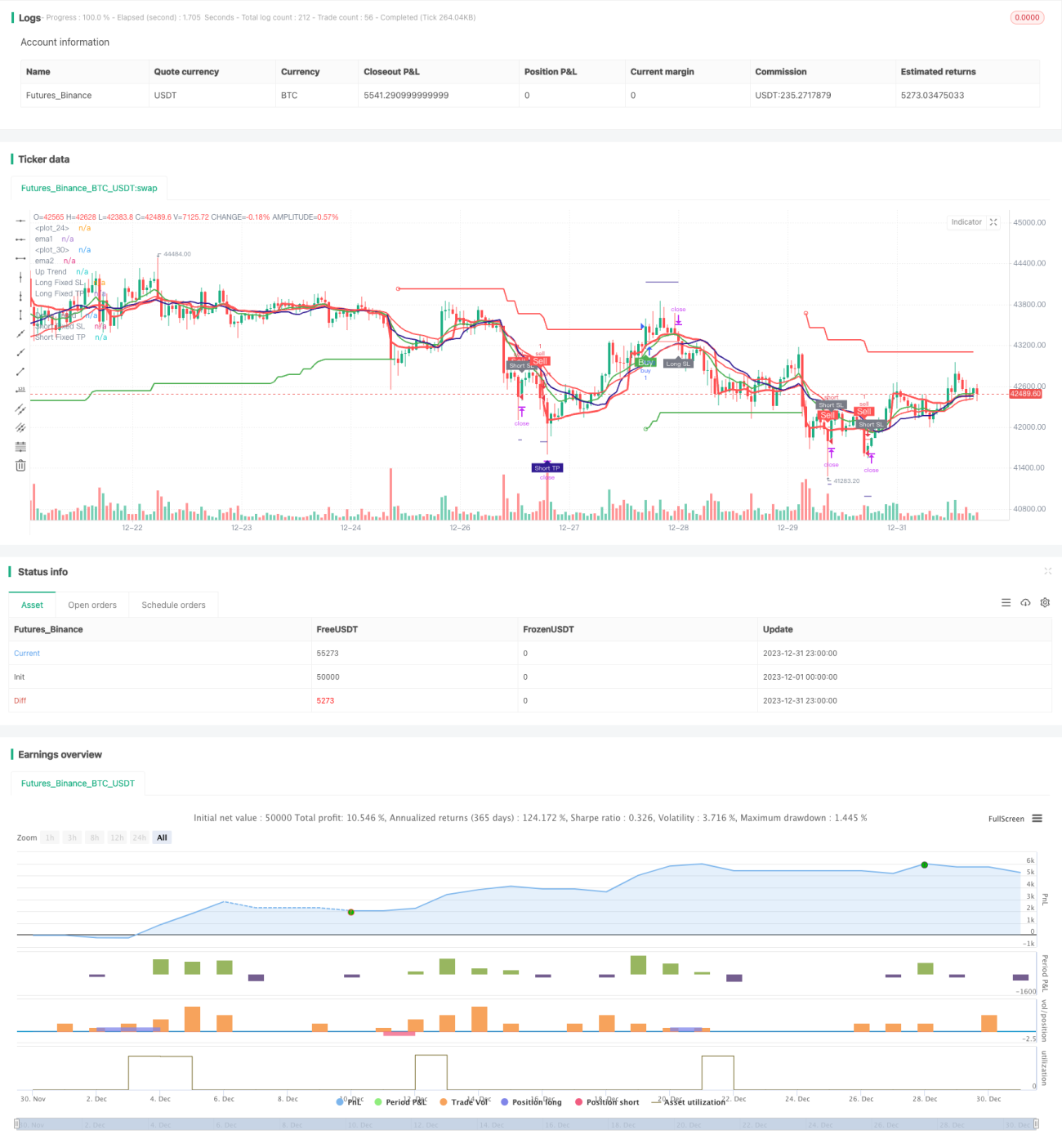

یہ حکمت عملی ایک مقداری تجارتی حکمت عملی ہے جو متعدد تکنیکی اشاریوں کا استعمال کرتی ہے۔ اس میں بنیادی طور پر EMA اوسط کراس اوور، SuperTrend اشاریہ، RSI اشاریہ، MACD اشاریہ وغیرہ جیسے مختلف اشاریوں کو ملا کر تجارتی سگنلز تیار کیے جاتے ہیں۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی تجارتی منطق درج ذیل پہلوؤں پر مبنی ہے:

-

EMA اوسط کراس اوور: تیز رفتار لائن EMA1 اور سست رفتار لائن EMA2 کا حساب لگایا جاتا ہے۔ جب تیز رفتار لائن سست رفتار لائن کو اوپر سے عبور کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب تیز رفتار لائن نیچے سے عبور کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

-

VWMA اوسط: VWMA اوسط کا حساب لگایا جاتا ہے۔ جب اختتامی قیمت اس اوسط کو اوپر سے عبور کرتی ہے تو خرید کا سگنل سمجھا جاتا ہے، اور جب نیچے سے عبور کرتی ہے تو فروخت کا سگنل سمجھا جاتا ہے۔

-

SuperTrend اشاریہ: ATR اور multiplier پیرامیٹرز کی بنیاد پر SuperTrend کے اوپری اور نچلے بینڈ کا حساب لگایا جاتا ہے اور رجحان کی سمت کا تعین کیا جاتا ہے۔ بڑھتے ہوئے رجحان میں خرید کا سگنل پیدا ہوتا ہے، جبکہ گرتے ہوئے رجحان میں فروخت کا سگنل پیدا ہوتا ہے۔

-

RSI اشاریہ: RSI اشاریہ کا حساب لگایا جاتا ہے۔ جب RSI اوور باؤٹ لائن سے زیادہ ہو تو فروخت کا سگنل سمجھا جاتا ہے، اور جب RSI اوور سیلڈ زون سے کم ہو تو خرید کا سگنل سمجھا جاتا ہے۔

-

MACD اشاریہ: MACD کی تیز رفتار لائن، سست رفتار لائن اور سگنل لائن کا حساب لگایا جاتا ہے۔ جب تیز رفتار لائن سگنل لائن کو اوپر سے عبور کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب نیچے سے عبور کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

مذکورہ بالا متعدد اشاریوں کے تجارتی سگنلز حاصل کرنے کے بعد، حکمت عملی "AND" منطق کا استعمال کرتے ہوئے فیصلہ کرتی ہے، یعنی جب ایک سے زیادہ اشاریے بیک وقت سگنل خارج کریں تب ہی حتمی خرید اور فروخت کے سگنلز تیار ہوتے ہیں۔

حکمت عملی کے فوائد

یہ حکمت عملی متعدد اشاریوں کو یکجا کر کے مارکیٹ کا جائزہ لیتی ہے، جس سے غلط سگنلز کو کم کیا جا سکتا ہے۔ اہم فوائد میں شامل ہیں:

-

متعدد اشاریوں کا استعمال کرتے ہوئے مرکب فلٹریشن کی وجہ سے ایک اشاریے کی وجہ سے پیدا ہونے والے غلط سگنلز کو کم کیا جا سکتا ہے۔

-

رجحان کے اشاریوں اور اتار چڑھاؤ کے اشاریوں کا امتزاج رجحان والی مارکیٹ میں اضافی منافع حاصل کرنے میں مدد دیتا ہے۔

-

مکمل اسٹاپ لاس منطق کے استعمال سے ایک ہی تجارتی لین دین میں زیادہ سے زیادہ نقصان کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے۔

-

مارٹنگیل منطق کی وجہ سے نقصان کے بعد پوزیشن بڑھا کر نقصان کی وصولی کا موقع ملتا ہے۔

حکمت عملی کے خطرات

اس حکمت عملی میں بنیادی طور پر درج ذیل خطرات موجود ہیں:

-

متعدد اشاریوں کا مجموعہ بہت محتاط ہو سکتا ہے، جس سے کچھ تجارتی مواقع ضائع ہو سکتے ہیں۔ اشاریوں کے مجموعے کو مناسب طریقے سے آسان بنایا جا سکتا ہے۔

-

مارٹنگیل پوزیشن بڑھانے کی منطق نقصان کو بڑھا سکتی ہے۔ پوزیشن بڑھانے کی تعداد پر مناسب حد مقرر کی جانی چاہیے۔

-

اسٹاپ لاس کی غلط پوزیشننگ غیر ضروری اسٹاپ لاس کا سبب بن سکتی ہے۔ خودکار موافق اسٹاپ لاس پوزیشن کا تعین کیا جانا چاہیے۔

-

اشاریوں کے پیرامیٹرز کی غلط ترتیب بہت زیادہ غلط سگنلز پیدا کر سکتی ہے۔ بہترین پیرامیٹرز کا سیٹ حاصل کرنے کے لیے پیرامیٹرز کو بہتر بنایا جانا چاہیے۔

حکمت عملی کی بہتری کے امکانات

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

-

مختلف پیرامیٹرز کے مجموعوں کے اشاریوں کے اثرات کا جائزہ لے کر اشاریوں کے وزن کا انتخاب کرنا۔

-

مختلف اشاریوں کے پیرامیٹرز کی ترتیبات کا تجربہ کرنا۔

-

خودکار موافق اسٹاپ لاس منطق شامل کرنا۔

-

متحرک پوزیشن مینجمنٹ میکانزم شامل کرنا۔

-

مشین لرننگ کے طریقوں کا استعمال کرتے ہوئے پیرامیٹرز اور ماڈل کو بہتر بنانا۔

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک بہت عملی مقداری تجارتی حکمت عملی ہے۔ اس میں متعدد کلاسیکی تکنیکی اشاریوں کی خوبیوں کو یکجا کیا گیا ہے، جس سے مارکیٹ کا مؤثر انداز میں جائزہ لیا جا سکتا ہے۔ پیرامیٹر کی بہتری اور ماڈل کی تکرار کے ذریعے اس حکمت عملی سے بہتر تجارتی نتائج حاصل کیے جا سکتے ہیں۔

- 1