دو طرفہ ADX تجارتی حکمت عملی

جائزہ

دو طرفہ ADX تجارتی حکمت عملی ایک مقداری حکمت عملی ہے جو اوسط سمتاتی اشاریہ (ADX) کے اشارے کو استعمال کرتے ہوئے دو طرفہ تجارت کو ممکن بناتی ہے۔ یہ حکمت عملی ADX اشارے اور DIPlus اور DIMinus اشارے کے فرق کا حساب لگا کر، تجارتی سگنل پیدا کرنے کے لیے ایک حد مقرر کرتی ہے، اور منافع حاصل کرنے کے لیے لانگ اور شارٹ پوزیشنیں لیتی ہے۔

حکمت عملی کا اصول

- حقیقی اتار چڑھاؤ کی حد (True Range) کا حساب لگائیں۔

- صعودی سمتاتی حرکت (Directional Movement Plus) اور نزولی سمتاتی حرکت (Directional Movement Minus) کا حساب لگائیں۔

- ہموار شدہ حقیقی اتار چڑھاؤ کی حد (Smoothed True Range) کا حساب لگائیں۔

- ہموار شدہ صعودی حرکت (Smoothed Directional Movement Plus) اور ہموار شدہ نزولی حرکت (Smoothed Directional Movement Minus) کا حساب لگائیں۔

- DIPlus، DIMinus، اور ADX اشاروں کا حساب لگائیں۔

- DIPlus اور ADX کے درمیان فرق، اور DIMinus اور ADX کے درمیان فرق کا حساب لگائیں۔

- صعودی اور نزولی تجارت کے لیے فرق کی حدیں مقرر کریں۔

- جب فرق حد سے زیادہ ہو تو تجارتی سگنل پیدا ہونے کا فیصلہ کریں۔

- خرید و فروخت کے آرڈرز پیدا کریں۔

اس حکمت عملی کا بنیادی مقصد یہ ہے کہ سمتاتی اشاریوں جیسے ADX کا استعمال کرتے ہوئے رجحان کی سمت اور طاقت کا تعین کیا جائے، اور فرق کے فیصلے کے اصول کے ساتھ حدیں مقرر کر کے خودکار تجارت کی جائے۔

فوائد کا تجزیہ

- ADX کے ذریعے رجحان کی سمت کا تعین کرنا مارکیٹ کے رجحان کو درست طریقے سے پکڑ سکتا ہے۔

- فرق کے فیصلے کے اصول کا اطلاق جھوٹے سگنلز کو مؤثر طریقے سے فلٹر کر سکتا ہے۔

- دو طرفہ تجارت صعودی اور نزولی مواقع کو پوری طرح سے پکڑ سکتی ہے۔

- مکمل طور پر خودکار تجارت، کسی انسانی مداخلت کی ضرورت نہیں۔

- حکمت عملی کی منطق واضح ہے، جسے سمجھنا اور تبدیل کرنا آسان ہے۔

خطرات کا تجزیہ

- ADX اشارے میں تاخیر ہوتی ہے، جس سے رجحان کے موڑ کے مقامات چھوٹ سکتے ہیں۔

- دو طرفہ تجارت کے خطرات بڑھ جاتے ہیں، نقصان بڑھ سکتا ہے۔

- نامناسب پیرامیٹرز کی ترتیب ضرورت سے زیادہ تجارت کا باعث بن سکتی ہے۔

- بیک ٹیسٹ کا ڈیٹا حقیقی مارکیٹ کی نمائندگی نہیں کر سکتا، لہٰذا حقیقی تجارت میں خطرات موجود ہیں۔

حل کے طریقے:

- تجارتی سگنلز کی تصدیق کے لیے دیگر اشاروں کا استعمال کریں۔

- پیرامیٹرز کو بہتر بنائیں اور تجارتی تعدد کو کنٹرول کریں۔

- پوزیشن سائزنگ (Position Sizing) کو سختی سے منظم کر کے تجارتی پوزیشنوں کو کنٹرول کریں۔

بہتری کے امکانات

- ADX کے پیرامیٹرز کو بہتر بنائیں تاکہ اس کی حساسیت بہتر ہو۔

- سگنلز کو فلٹر کرنے کے لیے مزید اشاروں کا اضافہ کریں۔

- پیرامیٹرز کو بہتر بنانے کے لیے مشین لرننگ الگورتھم کا استعمال کریں۔

- نقصان کے خطرے کو کنٹرول کرنے کے لیے جدید اسٹاپ لاس حکمت عملیوں کا استعمال کریں۔

- ماڈل کی پیش گوئیوں کو شامل کر کے زیادہ درست تجارتی سگنلز حاصل کریں۔

خلاصہ

دو طرفہ ADX تجارتی حکمت عملی مجموعی طور پر ایک بہت ہی عملی مقداری حکمت عملی ہے۔ یہ ADX اشارے کا استعمال کرتے ہوئے رجحان کا تعین کرتی ہے اور دو طرفہ تجارتی مواقع کو پکڑتی ہے۔ ساتھ ہی، فرق کے فیصلے کے اصول کا استعمال سگنلز کی درستگی کو یقینی بناتا ہے۔ اس حکمت عملی کی منطق واضح اور سادہ ہے، جسے تبدیل کرنا اور بہتر بنانا آسان ہے، اور یہ ایک دو طرفہ رجحان پر مبنی تجارتی حکمت عملی ہے۔ مناسب پیرامیٹر کی اصلاح، اسٹاپ لاس حکمت عملیوں کے اطلاق، اور سگنل فلٹرنگ کے ذریعے اس حکمت عملی کے استحکام اور منافع بخش صلاحیت کو مزید بڑھایا جا سکتا ہے۔

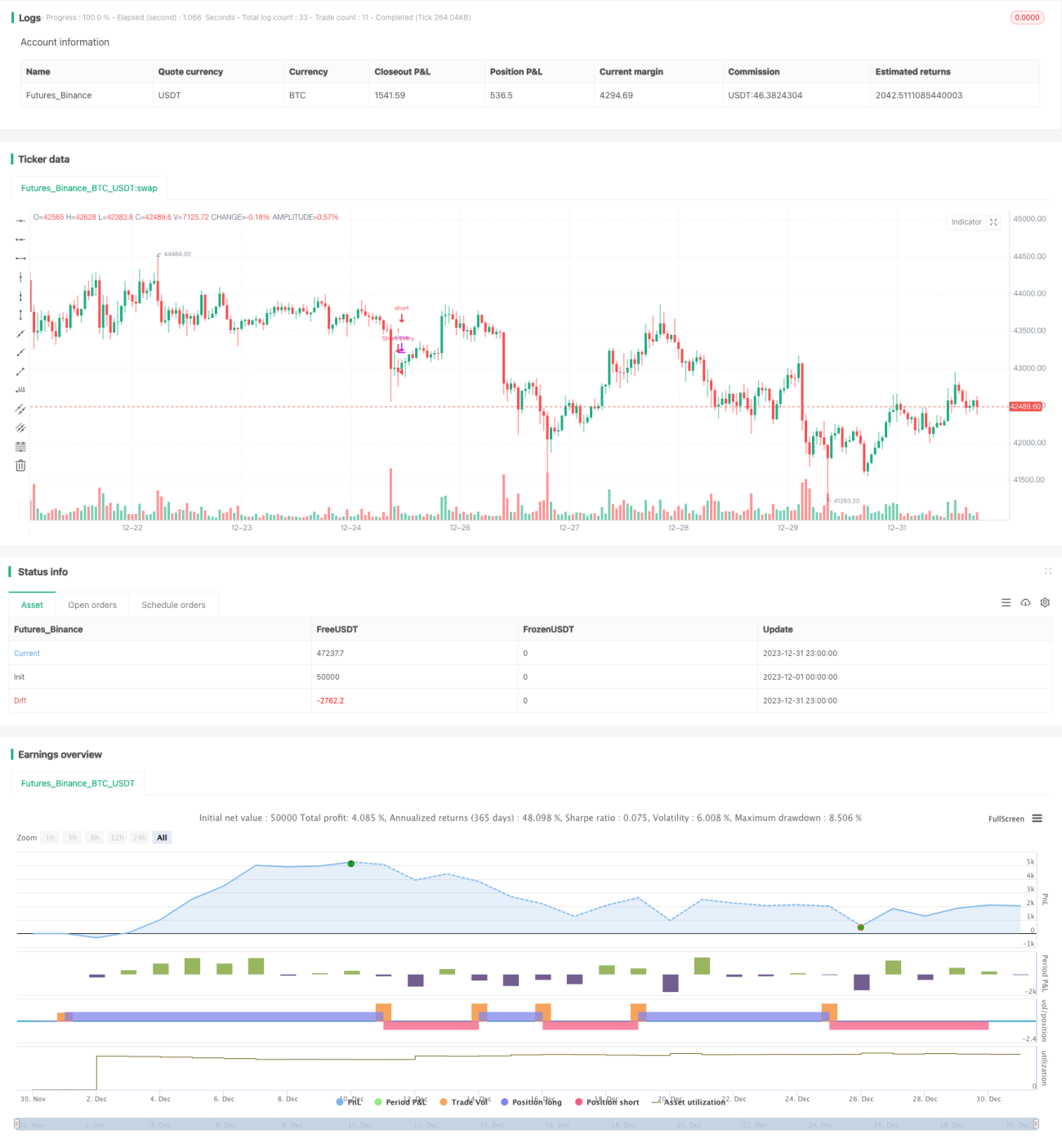

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1