دوہری موونگ ایوریج چان تھیوری حکمت عملی

جائزہ

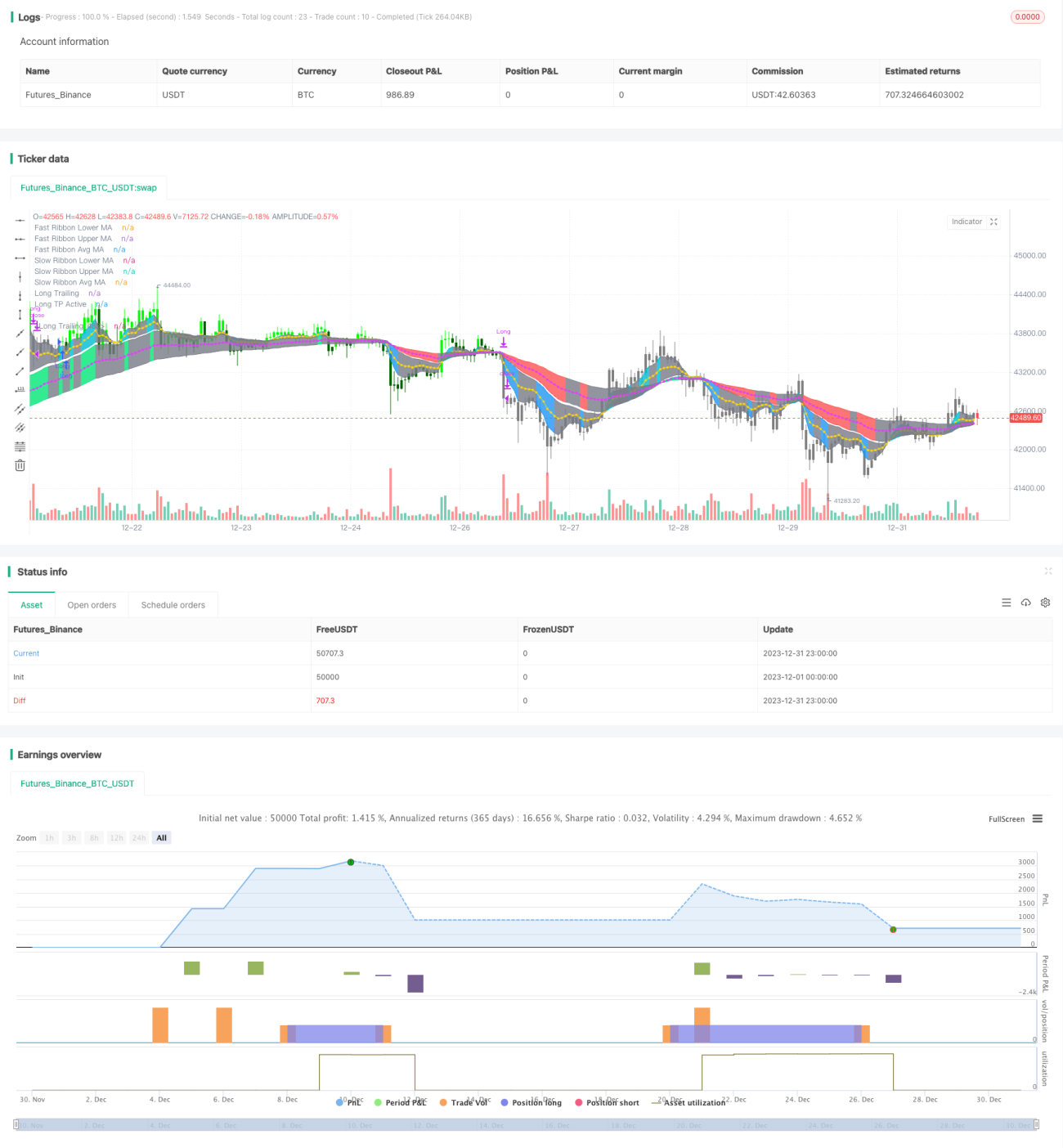

دو اوسط لکیروں پر مبنی چان لون حکمت عملی ایک رجحان پر عمل کرنے والی حکمت عملی ہے۔ یہ دو گروپوں میں متحرک اوسط کا حساب لگا کر تیز رفتار اور سست رفتار لکیروں کے گروپ تشکیل دیتی ہے، اور قیمت اور اوسط لکیروں کے درمیان تعلق کی بنیاد پر رجحان کی سمت کا تعین کرتی ہے۔

جب تیز رفتار لکیر سست رفتار لکیر کو اوپر سے عبور کرتی ہے تو یہ تیزی کا اشارہ ہے۔ جب تیز رفتار لکیر سست رفتار لکیر کو نیچے سے عبور کرتی ہے تو یہ مندی کا اشارہ ہے۔ یہ حکمت عملی تیز اور سست اوسط لکیروں کی سمت، قیمت کی بریک آؤٹ کے لیے موم بتیوں کی تعداد جیسی شرائط کو ملا کر داخلے اور خارج ہونے کے مخصوص اوقات کا تعین کرتی ہے۔

حکمت عملی کا اصول

دو اوسط لکیروں پر مبنی چان لون حکمت عملی دو گروپوں میں متحرک اوسط کا حساب لگا کر ترتیب دیتی ہے، جو بالترتیب قلیل مدتی اور طویل مدتی رجحان کے معیار کی نمائندگی کرتی ہیں۔ خاص طور پر، حکمت عملی میں مندرجہ ذیل تعریف کی گئی ہے:

- تیز رفتار اوسط لکیروں کا گروپ، جس میں تیز رفتار نچلی اوسط لکیر اور تیز رفتار بالائی اوسط لکیر شامل ہیں، قلیل مدتی رجحان کی نمائندگی کرتی ہیں۔

- سست رفتار اوسط لکیروں کا گروپ، جس میں سست رفتار نچلی اوسط لکیر اور سست رفتار بالائی اوسط لکیر شامل ہیں، طویل مدتی رجحان کی نمائندگی کرتی ہیں۔

یہ حکمت عملی تیز رفتار اور سست رفتار اوسط لکیروں کے گروپوں کے درمیان قیمت کے تعلق کے ذریعے قلیل مدتی اور طویل مدتی رجحان کی معقولیت، اور داخلے اور خارج ہونے کے مخصوص اوقات کا تعین کرتی ہے۔

داخلے کی شرائط درج ذیل ہیں:

- جب تیز رفتار بالائی لکیر سست رفتار بالائی لکیر کو 2 یا اس سے زیادہ موم بتیوں کے لیے اوپر سے عبور کرتی ہے تو یہ تیزی کی پوزیشن میں داخل ہونے کا اشارہ ہے۔

- جب تیز رفتار نچلی لکیر سست رفتار نچلی لکیر کو 2 یا اس سے زیادہ موم بتیوں کے لیے نیچے سے عبور کرتی ہے تو یہ مندی کی پوزیشن میں داخل ہونے کا اشارہ ہے۔

خارج ہونے کی شرائط درج ذیل ہیں:

- تیزی کی پوزیشن کے دوران، جب تیز رفتار اوسط لکیر سست رفتار اوسط لکیر کو نیچے سے عبور کرتی ہے تو یہ تیزی کی پوزیشن سے خارج ہونے کا اشارہ ہے۔

- مندی کی پوزیشن کے دوران، جب تیز رفتار اوسط لکیر سست رفتار اوسط لکیر کو اوپر سے عبور کرتی ہے تو یہ مندی کی پوزیشن سے خارج ہونے کا اشارہ ہے۔

اس کے علاوہ، حکمت عملی میں منافع کی حد، نقصان کی حد، اور ٹریلنگ اسٹاپ جیسے خطرے پر قابو پانے کے اقدامات بھی شامل ہیں۔

فوائد کا تجزیہ

دو اوسط لکیروں پر مبنی چان لون حکمت عملی کے اہم فوائد یہ ہیں:

- دوہری اوسط لکیروں کے ذریعے فیصلہ کرنے سے مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے اور رجحان کی سمت کو درست کیا جا سکتا ہے۔

- تیز اور سست اوسط لکیروں اور قیمت کے تعلق کو ملا کر، سگنلز کی قابل اعتمادی زیادہ ہوتی ہے۔

- حکمت عملی کے اصول سادہ اور واضح ہیں، سمجھنے اور نافذ کرنے میں آسان ہیں، اور مقداری تجارت کے لیے موزوں ہیں۔

- منافع کی حد، نقصان کی حد، ٹریلنگ اسٹاپ جیسے خطرے پر قابو پانے کے اقدامات شامل ہیں، جو تجارتی خطرے کو مؤثر طریقے سے کنٹرول کر سکتے ہیں۔

خطرے کا تجزیہ

دو اوسط لکیروں پر مبنی چان لون حکمت عملی میں کچھ خطرات بھی ہیں، جو درج ذیل ہیں:

- اتار چڑھاؤ والی مارکیٹ میں، جھوٹے سگنل پیدا ہو سکتے ہیں، جس سے غیر ضروری تجارت ہو سکتی ہے۔

- اوسط لکیروں کا نظام اچانک واقعات (جیسے بڑی منفی/مثبت خبروں کے منظر عام پر آنے) پر سست ردعمل ظاہر کرتا ہے، جس سے بڑا نقصان ہو سکتا ہے۔

- ٹریلنگ اسٹاپ مخصوص مارکیٹ حالات میں ٹوٹ سکتا ہے، جس سے نقصان بڑھ سکتا ہے۔

مذکورہ خطرات پر قابو پانے کے لیے، متحرک اوسط کے پیرامیٹرز کو بہتر بنا کر، یا دیگر اشاریوں کے ساتھ فلٹر کر کے بہتری لائی جا سکتی ہے۔

بہتری کی سمت

دو اوسط لکیروں پر مبنی چان لون حکمت عملی کو درج ذیل جہتوں سے بہتر بنایا جا سکتا ہے:

- متحرک اوسط کے پیرامیٹرز کو بہتر بنانا، اوسط کی مدت کو مختلف ادوار کی مارکیٹ کے مطابق ایڈجسٹ کرنا۔

- دیگر اشاریوں کے فلٹرز شامل کرنا، کثیر اشاریوں کی مشترکہ حکمت عملی تشکیل دینا، اور سگنلز کی درستگی بڑھانا۔

- نقصان کی حد اور منافع کی حد کی ترتیبات کو بہتر بنانا، ڈرا ڈاؤن کی حد مقرر کرنا، اور زیادہ سے زیادہ نقصان کو کنٹرول کرنا۔

- رجحان کی پیش گوئی کے لیے مشین لرننگ ماڈل متعارف کرانا، داخلے کے وقت کا تعین کرنے میں مدد فراہم کرنا۔

خلاصہ

دو اوسط لکیروں پر مبنی چان لون حکمت عملی مجموعی طور پر ایک بہت ہی عملی رجحان پر عمل کرنے والی حکمت عملی ہے۔ اس کے فیصلے کے اصول سادہ ہیں، منطق واضح ہے، یہ دوہری اوسط لکیروں کے نظام کے ذریعے خطرے کو کنٹرول کرتی ہے، اور اس کی نظریاتی بنیاد مضبوط ہے۔ اگلے مرحلے میں پیرامیٹر کی بہتری، خطرے کے کنٹرول وغیرہ کے ذریعے مزید بہتری لائی جا سکتی ہے تاکہ حکمت عملی کے منافع اور استحکام کو مزید بڑھایا جا سکے۔

- 1