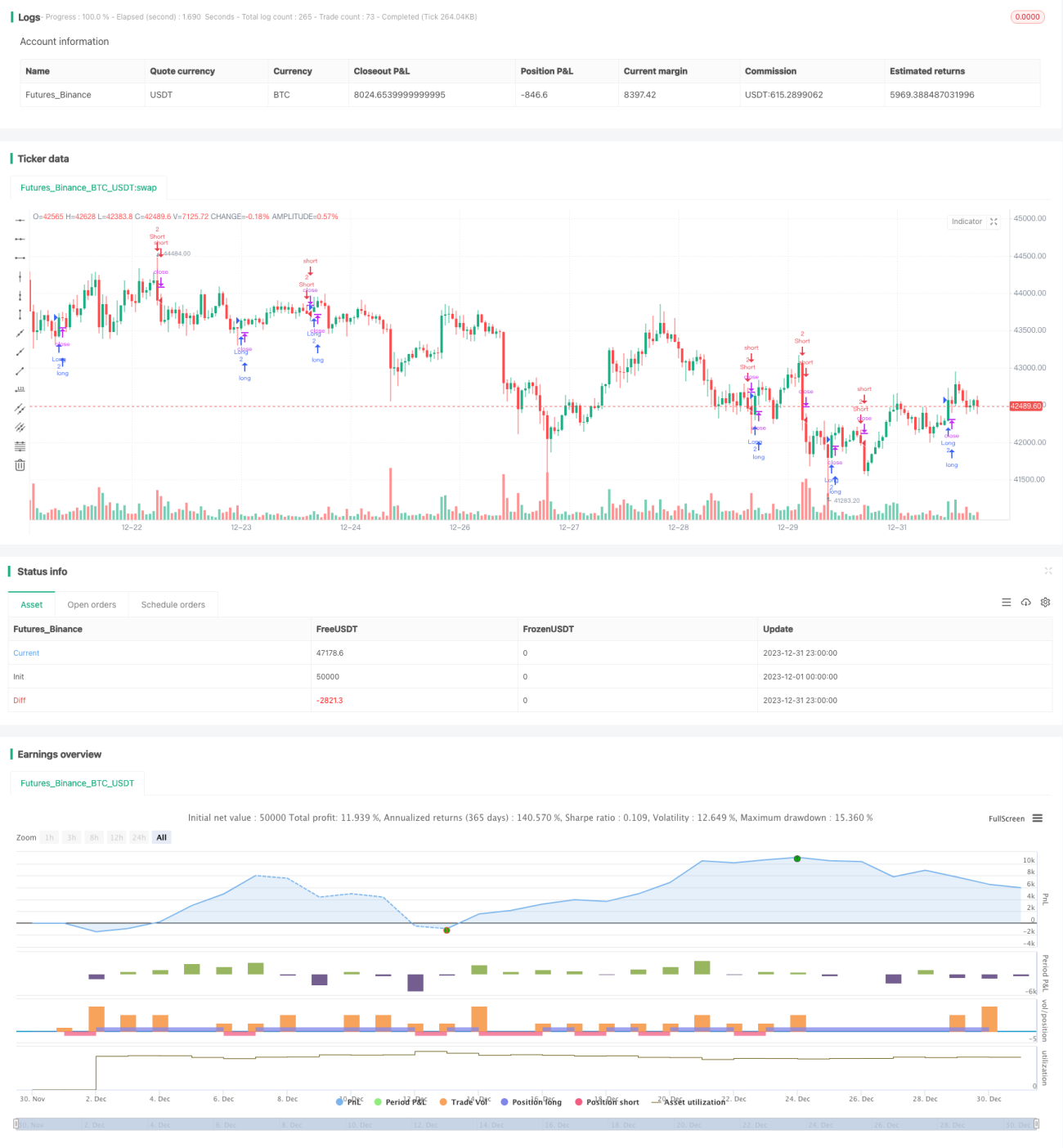

K-لائن پر مبنی دو طرفہ بریک آؤٹ ٹریڈنگ حکمت عملی

جائزہ

یہ ایک کینڈل سٹک پر مبنی دو طرفہ بریک آؤٹ ٹریڈنگ حکمت عملی ہے۔ جب موجودہ کینڈل سٹک کی اختتامی قیمت پچھلی دو کینڈل سٹکس کی بلند ترین اور پست ترین قیمتوں سے بریک آؤٹ ہوتی ہے تو یہ ٹریڈنگ سگنل پیدا کرتی ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی منطق یہ ہے:

-

بل سگنل کی تعریف:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]یعنی موجودہ کینڈل سٹک کی اختتامی قیمت اس کی افتتاحی قیمت سے زیادہ ہے، اور پچھلی دو کینڈل سٹکس کی بلند ترین قیمت سے بھی زیادہ ہے، جبکہ موجودہ کینڈل سٹک کی پست ترین قیمت پچھلی کینڈل سٹک کی پست ترین قیمت سے کم ہے۔ -

بیئر سگنل کی تعریف:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]یعنی موجودہ کینڈل سٹک کی اختتامی قیمت اس کی افتتاحی قیمت سے کم ہے، اور پچھلی دو کینڈل سٹکس کی پست ترین قیمت سے بھی کم ہے، جبکہ موجودہ کینڈل سٹک کی بلند ترین قیمت پچھلی کینڈل سٹک کی بلند ترین قیمت سے زیادہ ہے۔ -

جب بل سگنل متحرک ہو تو لانگ کھولیں؛ جب بیئر سگنل متحرک ہو تو شارٹ کھولیں۔

-

سٹاپ لاس اور ٹیک پروفٹ کی پوزیشنیں سیٹ کی جا سکتی ہیں۔

یہ حکمت عملی دو طرفہ بریک آؤٹ کی خصوصیت کا استعمال کرتے ہوئے اہم قیمت کے وقفوں سے بریک آؤٹ کے ذریعے رجحان میں تبدیلی کا تعین کرتی ہے اور اس طرح ٹریڈنگ سگنل پیدا کرتی ہے۔

فوائد کا تجزیہ

یہ نسبتاً سادہ اور بدیہی بریک آؤٹ حکمت عملی ہے، جس کے درج ذیل فوائد ہیں:

- منطق واضح، سمجھنے اور نافذ کرنے میں آسان، کم پیچیدہ۔

- بریک آؤٹ عام ٹریڈنگ سگنل ہیں، آسانی سے رجحان تشکیل دیتے ہیں۔

- بیک وقت لانگ اور شارٹ ٹریڈنگ ممکن ہوتی ہے، جس سے منافع کے مواقع بڑھ جاتے ہیں۔

- سٹاپ لاس اور ٹیک پروفٹ کو لچکدار طریقے سے سیٹ کیا جا سکتا ہے تاکہ خطرے کو کنٹرول کیا جا سکے۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- دو طرفہ ٹریڈنگ میں خطرہ زیادہ ہوتا ہے، جس کے لیے قریبی نگرانی ضروری ہے۔

- بریک آؤٹ پھنسنے کا امکان رہتا ہے، جھوٹے سگنلز پیدا ہو سکتے ہیں۔

- پیرامیٹرز کی غلط ترتیب سے ضرورت سے زیادہ ٹریڈنگ ہو سکتی ہے۔

- سٹاپ لاس اور ٹیک پروفٹ کی غلط ترتیب منافع کی گنجائش کو متاثر کر سکتی ہے۔

پیرامیٹرز کو بہتر بنا کر اور مناسب مصنوعات کا انتخاب کر کے خطرے کو کم کیا جا سکتا ہے۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- پیرامیٹرز کو بہتر بنانا، جیسے بریک آؤٹ مدت کے پیرامیٹرز، سٹاپ لاس/ٹیک پروفٹ کی مقدار وغیرہ۔

- فلٹر کی شرائط شامل کرنا تاکہ غلط سگنلز سے بچا جا سکے، جیسے کہ پھنسنے یا اتار چڑھاؤ والی مارکیٹ میں۔

- رجحان کے اشاریوں کے ساتھ ملا کر استعمال کرنا، تاکہ رینج والے حصوں سے بچا جا سکے۔

- سرمایہ کے انتظام کو بہتر بنانا، پوزیشن کے حساب کتاب کے طریقے کو بہتر کرنا۔

- مختلف مصنوعات کے پیرامیٹرز مختلف ہوتے ہیں، انہیں الگ الگ ٹیسٹ اور بہتر کیا جا سکتا ہے۔

خلاصہ

یہ دو طرفہ بریک آؤٹ کے تصور پر مبنی ایک سادہ حکمت عملی ہے۔ اس میں واضح منطق اور آسان نفاذ کی خوبیاں ہیں، جبکہ نگرانی کے کچھ خطرات بھی موجود ہیں۔ پیرامیٹرز اور شرائط کو بہتر بنا کر اچھے حکمت عملی کے نتائج حاصل کیے جا سکتے ہیں۔

- 1