متعدد اشاروں پر مبنی رجحان کی پیروی کی حکمت عملی

جائزہ

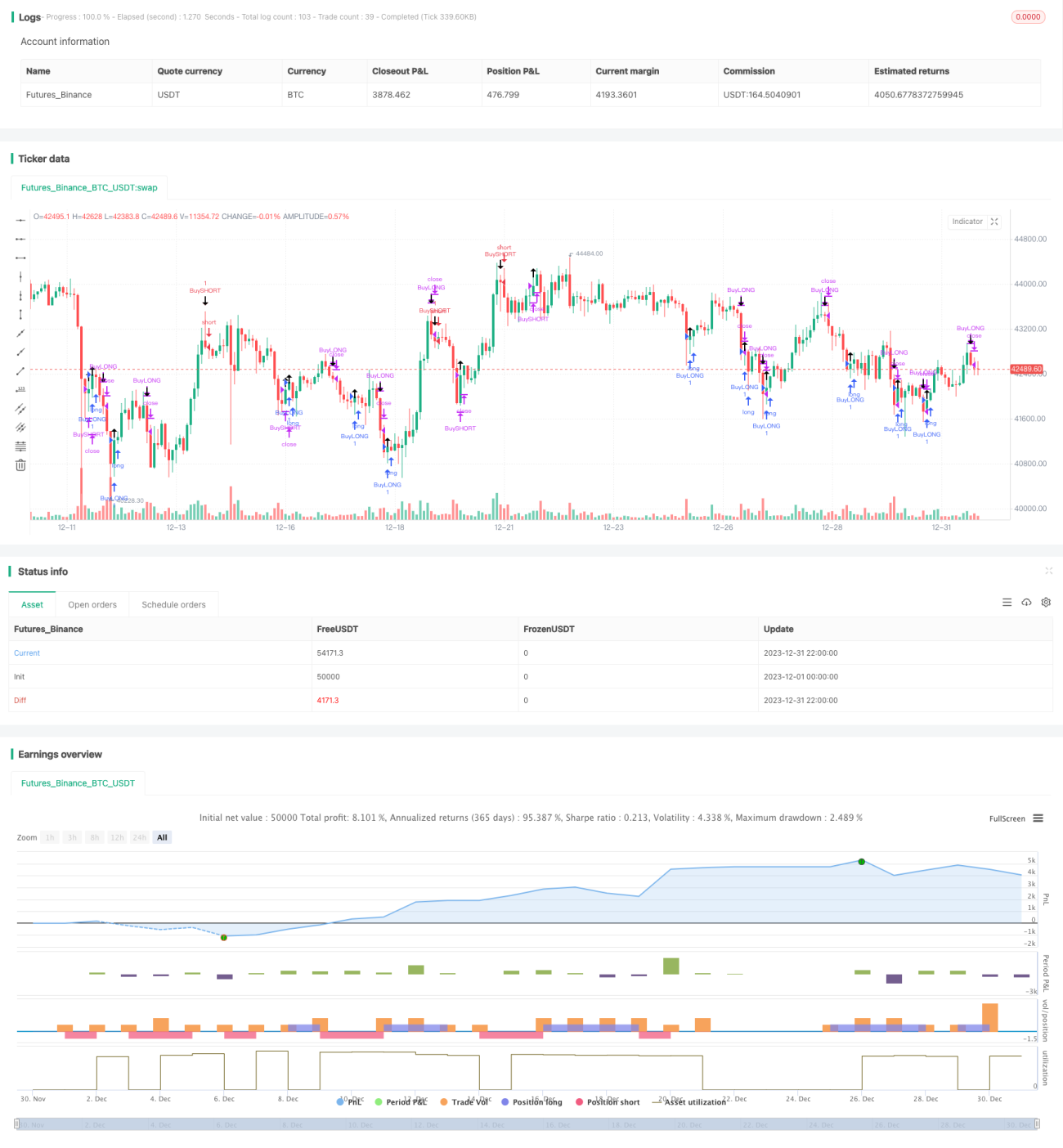

یہ حکمت عملی متعدد انڈیکیٹرز کو ملا کر رجحان (ٹرینڈ) کی شناخت کرتی ہے، اور منافع کو محفوظ رکھنے کے لیے ٹرینڈ ٹریکنگ اسٹاپ لاس مقرر کرتی ہے۔ بنیادی طور پر Bollinger Bands، RSI، ADX جیسے انڈیکیٹرز داخلے کے مواقع کا تعین کرنے کے لیے استعمال ہوتے ہیں، جبکہ ATR اور Bollinger Bands اسٹاپ لاس کے لیے استعمال ہوتے ہیں۔

حکمت عملی کا اصول

حکمت عملی کے بنیادی فیصلہ کن انڈیکیٹرز Bollinger Bands، RSI اور ADX ہیں۔ جب قیمت Bollinger Bands کے نچلے بینڈ کے قریب پہنچتی ہے اور RSI 30 سے کم ہوتی ہے تو اسے زیادہ فروخت (اوور سولڈ) سمجھا جاتا ہے اور لانگ (خرید) کیا جاتا ہے۔ جب قیمت Bollinger Bands کے اوپری بینڈ کے قریب پہنچتی ہے اور RSI 70 سے زیادہ ہوتی ہے تو اسے زیادہ خریدا (اوور باؤٹ) سمجھا جاتا ہے اور شارٹ (فروخت) کیا جاتا ہے۔ اس کے علاوہ، جب ADX 25 سے زیادہ ہوتا ہے تو رجحان (ٹرینڈ) کی تشکیل سمجھی جاتی ہے، جس کی صورت میں خرید/فروخت کے سگنلز زیادہ مؤثر ہوتے ہیں۔

پوزیشن کھولنے کے بعد، حکمت عملی ATR انڈیکیٹر اور Bollinger Bands کے اوپری/نچلے بینڈز کو اسٹاپ لاس کے لیے استعمال کرتی ہے۔ خاص طور پر، ATR زیادہ سے زیادہ اسٹاپ لاس کے حجم کے لیے استعمال ہوتا ہے، جب قیمت زیادہ سے زیادہ اسٹاپ لاس پوائنٹ کو چھو لے تو پوزیشن بند کر دی جاتی ہے۔ Bollinger Bands کے اوپری/نچلے بینڈز ٹریلنگ اسٹاپ لاس پوائنٹس ترتیب دینے کے لیے استعمال ہوتے ہیں، جو قیمت کی حرکت کے مطابق حقیقی وقت میں اپ ڈیٹ ہوتے ہیں۔

فوائد کا تجزیہ

یہ حکمت عملی متعدد انڈیکیٹرز کو ملا کر رجحان (ٹرینڈ) کی مؤثر شناخت کرتی ہے، اور اسٹاپ لاس میکانزم کے ذریعے منافع کو محفوظ رکھتی ہے اور نقصان کے خطرے کو کم کرتی ہے، جو اسے ایک معقول اور مستحکم حکمت عملی بناتی ہے۔ مخصوص فوائد درج ذیل ہیں:

- Bollinger Bands کا استعمال اوور باؤٹ/اوور سولڈ حالات کا تعین کرنے کے لیے، جو ریورسل مواقع کی نشاندہی کرتا ہے

- RSI انڈیکیٹر کے ساتھ اس کا امتزاج فیصلوں کی درستگی بڑھاتا ہے

- ADX انڈیکیٹر رجحان (ٹرینڈ) کی تشکیل کا تعین کرتا ہے، جس سے تجارت کی صحیح سمت یقینی بنتی ہے

- ATR اور Bollinger Bands پر مبنی ٹریلنگ اسٹاپ لاس، منافع کو زیادہ سے زیادہ محفوظ رکھتا ہے

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی موجود ہیں:

- متعدد انڈیکیٹرز کا استعمال، پیرامیٹرز کو اوور آپٹمائز کرنا آسان ہے

- جب Bollinger Bands کا وقفہ بہت وسیع ہو تو اوور باؤٹ/اوور سولڈ سگنلز کی کارکردگی کم ہو جاتی ہے

- اسٹاپ لاس ٹریکنگ کی غلط ترتیب نقصان کو بڑھا سکتی ہے

ان خطرات سے نمٹنے کے لیے درج ذیل اقدامات کیے جا سکتے ہیں:

- متعدد پیرامیٹر مجموعوں کی بہتر کاری، اوور آپٹمائزیشن سے بچنے کے لیے

- مارکیٹ کے اتار چڑھاؤ کے مطابق Bollinger Bands کے پیرامیٹرز کو ایڈجسٹ کرنا

- اسٹاپ لاس کے فاصلے کے پیرامیٹرز کو جانچنا تاکہ عام اتار چڑھاؤ کو برداشت کیا جا سکے

بہتر بنانے کے پہلو

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

- پوزیشن سائز کے کنٹرول کا اضافہ، اسٹاپ لاس کے ضرب کے مطابق پوزیشن کا حجم ایڈجسٹ کرنا

- منی مینجمنٹ ماڈیول کا اضافہ، ایک ہی تجارت میں اسٹاپ لاس کی مقدار پر سخت کنٹرول

- دیگر اسٹاپ لاس انڈیکیٹرز جیسے DMI، Envelopes وغیرہ کی جانچ

- مشین لرننگ ماڈل کا اضافہ، رجحان (ٹرینڈ) کے امکانات کا تعین کرنے کے لیے، جس سے تاثیر بہتر ہوتی ہے

خلاصہ

مجموعی طور پر یہ حکمت عملی ایک نسبتاً مستحکم ٹرینڈ ٹریکنگ حکمت عملی ہے۔ یہ متعدد انڈیکیٹرز کے ذریعے رجحان کی سمت کا تعین کرتی ہے، اور اسٹاپ لاس کے اقدامات کے ساتھ خطرے پر قابو پاتی ہے، جس سے منافع کی اچھی شرح حاصل کی جا سکتی ہے۔ ہم نے بہتری کے کئی ممکنہ پہلو بھی بتائے ہیں، جن پر مزید کام کرنے سے بہتر نتائج حاصل کیے جا سکتے ہیں۔

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1