حکمت عملی کے بعد بریک آؤٹ

جائزہ

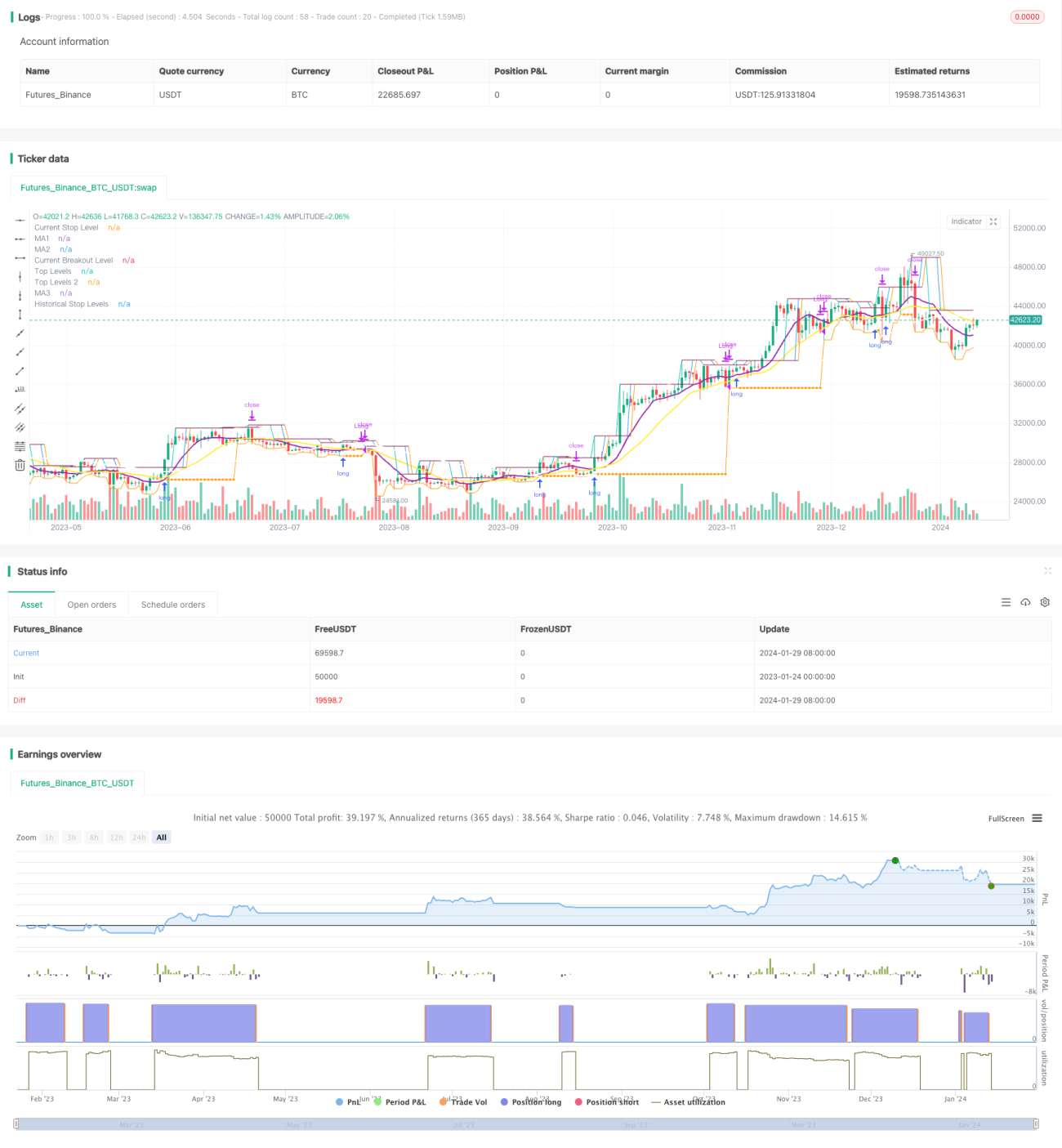

اس حکمت عملی کا بنیادی خیال یہ ہے کہ بڑے ٹائم فریموں پر رجحانات کی سمت کی نشاندہی کی جائے اور چھوٹے ٹائم فریموں پر بریک آؤٹ پوائنٹس کو تلاش کیا جائے ، جبکہ اسٹاپ نقصان سے باہر نکلنے والے بڑے ٹائم فریموں پر چلنے والی اوسط کو ٹریک کیا جائے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر تین اشارے پر مبنی ہے۔

سب سے پہلے ، ایک طویل دورانیے (جیسے سورج کی لکیر) کے X دن کی سادہ حرکت پذیر اوسط کا حساب لگائیں ، اور صرف اس وقت خریدنے کی اجازت دیں جب قیمت اسٹیشن پر ہو۔ اس سے مجموعی طور پر رجحان کی سمت کا تعین کیا جاسکتا ہے ، اور تجارت کے اتار چڑھاؤ کی مدت سے بچا جاسکتا ہے۔

دوسرا ، ایک مختصر مدت (جیسے 5 دن) کے اندر سب سے زیادہ قیمت کی سوئنگ ہائی کا حساب لگائیں ، جب قیمت اس سب سے زیادہ قیمت کو توڑ دیتی ہے تو اس سے خریدنے کا اشارہ ہوتا ہے۔ یہاں ایک جائزہ لینے والے سائیکل پیرامیٹرز کے ساتھ مل کر مناسب نقطہ نظر کی تلاش کریں۔

تیسرا ، ایک اسٹاپ لائن قائم کریں۔ پوزیشن میں داخل ہونے کے بعد ، اسٹاپ لائن ایک خاص دورانیے کے لئے lbStop کی کم سے کم قیمت پر قفل کردی جاتی ہے۔ ایک متحرک اوسط ((جیسے یومیہ 10 دن ای ایم اے) کو ایکسٹٹ میکانزم کے طور پر ترتیب دیتے ہوئے ، جب قیمت اس متحرک اوسط سے کم ہو تو پوزیشن سے باہر نکلیں۔

اس حکمت عملی کے ساتھ ساتھ اے ٹی آر کی قیمت بھی مقرر کی گئی ہے تاکہ پوائنٹس کی خریداری سے بچایا جاسکے۔ اس کے علاوہ ، دیگر معاون شرائط جیسے ریٹرننگ ٹائم رینج ہیں۔

ان تینوں اشارے کا آپس میں تعامل اس حکمت عملی کی بنیادی منطق ہے۔

حکمت عملی کا تجزیہ

یہ ایک ایسی حکمت عملی ہے جس میں درج ذیل فوائد ہیں:

-

دو ٹائم فریموں کا استعمال کرتے ہوئے ، اتار چڑھاؤ کی منڈیوں میں پھنس جانے سے بچیں۔ لمبے وقت کے فریموں میں مجموعی رجحانات کا اندازہ لگایا جاتا ہے ، اور مختصر وقت کے فریموں میں مخصوص داخلے کے مقامات کی تلاش کی جاتی ہے۔

-

سوئنگ ہائی کی تشکیل کے نقطہ نظر کا استعمال کرتے ہوئے، اس طرح کے توڑنے میں کچھ انترج اور آسانی سے ٹریکنگ کی تشکیل ہوتی ہے۔ اس کے ساتھ ساتھ ، سائیکل lb پیرامیٹرز کو دوبارہ دیکھ کر واقعی موثر توڑنے کی تلاش کی جاسکتی ہے۔

-

نقصانات کو روکنے کا طریقہ زیادہ سخت ہے ، حالیہ نچلی سطح کو ٹریک کریں اور کچھ حد تک بچاؤ کا فاصلہ چھوڑ دیں ، تاکہ اس سے بچنے سے بچ سکے۔

-

ایکٹ کے طور پر منتقل اوسط کا استعمال کرتے ہوئے، آپ کو آپ کی مرضی کے مطابق لچکدار روکنے کے کر سکتے ہیں.

-

اے ٹی آر اشارے سے زیادہ مقدار میں ہونے والے خطرات سے بچنے کے لئے۔

-

مختلف پیرامیٹرز کے مجموعے کو جانچنے کے لئے ترتیب دیا جاسکتا ہے ، بہتر بنانے کے لئے زیادہ جگہ ہے۔

خطرے کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

-

جب قیمتوں میں حرکت پذیر اوسط کے قریب اتار چڑھاؤ ہوتا ہے تو ، اس میں بار بار سوئچنگ اور آؤٹ پوزیشن کا خطرہ ہوتا ہے۔ اس وقت اعلی فیسوں کا خطرہ ہوتا ہے۔

-

جب آپ خریدنے کے نقطہ کو منتقل کرنے کے قریب توڑتے ہیں تو آپ کو واپسی کا خطرہ زیادہ ہوتا ہے۔ یہ حکمت عملی کی اپنی خصوصیت ہے۔

-

جب مارکیٹ میں کوئی واضح رجحان نہیں ہوتا ہے تو ، پوزیشن رکھنے میں زیادہ وقت لگ سکتا ہے ، جس سے وقت کا خطرہ ہوتا ہے۔

-

اے ٹی آر پیرامیٹرز کو مناسب طریقے سے ترتیب دینے کی ضرورت ہے۔ اے ٹی آر بہت کم فلٹرنگ کا اثر کمزور ہے ، اور بہت زیادہ داخلے کے امکانات کم ہیں۔

-

نتائج پر مختلف lb پیرامیٹرز کے اثر کو جانچنے کی ضرورت ہے۔ بہت بڑے پیرامیٹرز کچھ مواقع سے محروم ہوجاتے ہیں ، اور بہت چھوٹے پیرامیٹرز جھوٹی پیشرفت کی نشاندہی کرسکتے ہیں۔

خطرے سے نمٹنے کے طریقے:

- فلٹرنگ کو بڑھانے کے لئے منتقل اوسط پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کریں۔

- اے ٹی آر پیرامیٹرز کو بہتر بنائیں اور بصری فیصلے میں مدد کریں۔

- بہترین پیرامیٹرز کو تلاش کرنے کے لئے واپس سائیکل lb کو ایڈجسٹ کریں۔

- زلزلے کے دوران تجارت معطل کرنا۔

حکمت عملی کی اصلاح کی سمت

اس حکمت عملی کو مندرجہ ذیل جہتوں سے بھی بہتر بنایا جاسکتا ہے:

-

متحرک اوسط کے مختلف پیرامیٹرز کے مجموعے کی جانچ کریں اور بہترین پیرامیٹرز تلاش کریں۔

-

مختلف اے ٹی آر پیرامیٹرز کی ترتیبات کو آزمائیں ، جو داخلے کے مواقع اور خطرے کو کنٹرول کرنے میں توازن رکھتے ہیں۔

-

زیادہ موثر کامیابیوں کی شناخت کے لئے LB پیرامیٹرز کا جائزہ لینے کے لئے سائیکل کو بہتر بنائیں

-

متحرک اسٹاپ نقصان قائم کرنے کی کوشش کریں ، اتار چڑھاؤ اور واپسی کے حساب سے خطرے کو کنٹرول کریں۔

-

ٹرانزیکشن حجم کے اشارے جیسے دیگر عوامل کے ساتھ مل کر ، کامیابی کی تاثیر کا اندازہ لگایا گیا ہے۔

-

<!ENTITY prefixed with "/",</,><<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

-

مشین لرننگ کے ساتھ پیرامیٹرز کی تربیت کرنے کی کوشش کریں تاکہ آپ کو بہترین پیرامیٹرز مل سکیں۔

خلاصہ کریں۔

یہ حکمت عملی مجموعی طور پر ایک مثالی بریک ٹریکنگ حکمت عملی ہے۔ ڈبل ٹائم فریم کا فیصلہ ، سوئنگ ہائی نے اندراج کے وقت ، اسٹاپ نقصان کی لائن اور منتقل اوسط ڈبل انشورنس سے باہر نکلنے کا طریقہ کار کی نشاندہی کی ، جس سے ایک مکمل منطقی نظام تشکیل دیا گیا۔ اس حکمت عملی کے خطرات اور فوائد کی خصوصیات واضح ہیں ، جو درمیانی اور لمبی لائنوں کی پیروی کرنے والے سرمایہ کاروں کے لئے موزوں ہیں۔ اگرچہ کچھ خطرات موجود ہیں ، لیکن پیرامیٹرز کی اصلاح اور قواعد کی اصلاح کے ذریعہ اس خطرے کی سطح کو کم کیا جاسکتا ہے۔ اس حکمت عملی میں بہتری کی گنجائش ہے ، اور اگر اس میں مزید پیمائش کے فیصلے شامل ہوں تو اس حکمت عملی کی تاثیر کو مزید بڑھا سکتا ہے۔

/*backtest

start: 2023-01-24 00:00:00

end: 2024-01-30 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1