دو طرفہ گرڈ کینڈل اسٹک ٹریکنگ ٹریڈنگ حکمت عملی

خلاصہ

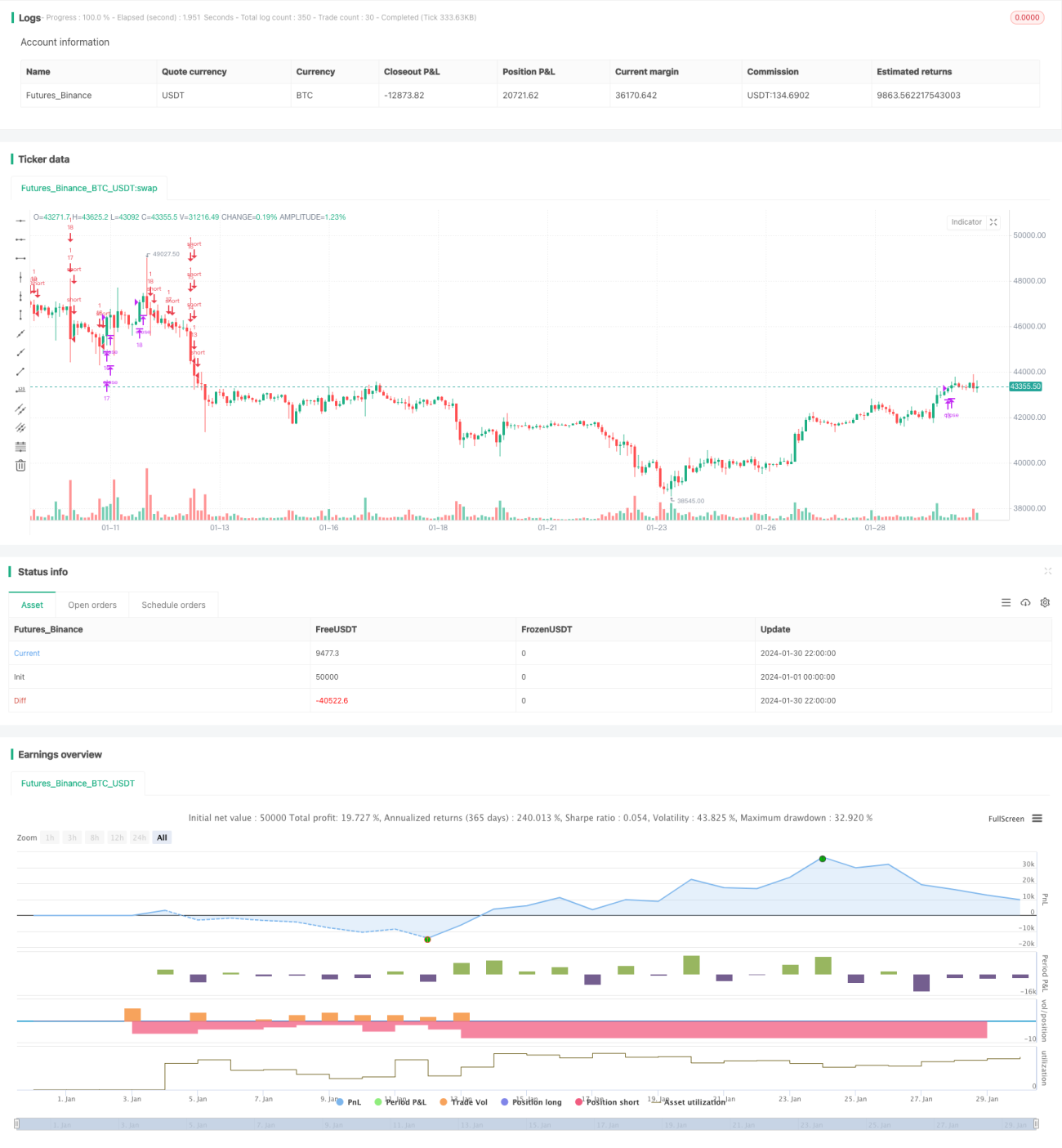

یہ حکمت عملی K لائن کی ریئل ٹائم تبدیلیوں پر مبنی دو طرفہ ٹریکنگ گرڈ ٹریڈنگ کی حکمت عملی ہے۔ یہ تیزی اور مندی دونوں بازاروں میں مستحکم منافع حاصل کر سکتی ہے۔

حکمت عملی کا اصول

-

صارف کی متعین کردہ گرڈوں کی تعداد کے مطابق، خود بخود قیمت کے گرڈ کے وقفے اور ہر گرڈ کی قیمت کا حساب لگایا جاتا ہے۔

-

جب قیمت گرڈ کی قیمت کو عبور کرتی ہے تو ایک مقررہ تعداد میں لانگ پوزیشن کھولی جاتی ہے؛ جب قیمت گرڈ کی قیمت سے نیچے آتی ہے تو لانگ پوزیشن بند کر کے شارٹ پوزیشن کھولی جاتی ہے۔

-

اس طرح، جب قیمت گرڈ کے وقفے میں اتار چڑھاؤ کرتی ہے تو قیمت کی تبدیلیوں کو ٹریک کر کے منافع حاصل کیا جا سکتا ہے۔

فوائد کا تجزیہ

-

معقول گرڈ کے وقفوں کا خودکار حساب، دستی طور پر سپورٹ اور ریزسٹنس متعین کرنے کی ضرورت نہیں۔

-

دو طرفہ ٹریڈنگ، مارکیٹ کے مختلف حالات میں ڈھل سکتی ہے۔

-

مقررہ پوزیشن کھولنے کی تعداد، رسک کنٹرول میں معاون ہے۔

-

کوڈ سیدھا اور سادہ، سمجھنے اور تبدیل کرنے میں آسان ہے۔

خطرات کا تجزیہ

-

شدید اتار چڑھاؤ نقصان کو بڑھا سکتا ہے۔

-

ٹریڈنگ فیسوں کا جمع ہونا بھی حتمی منافع کو متاثر کر سکتا ہے۔

-

گرڈوں کی تعداد کو معقول طریقے سے متعین کرنا ضروری ہے، زیادہ گرڈوں سے ٹریڈ کی تعداد بڑھ جاتی ہے لیکن ہر بار منافع محدود ہوتا ہے۔

بہتری کے راستے

-

اسٹاپ لاس کی حکمت عملی شامل کرنا تاکہ نقصان کو بڑھنے سے روکا جا سکے۔

-

گرڈوں کی تعداد میں متحرک تبدیلی کی فعالیت شامل کرنا۔

-

لیوریج شامل کرنے پر غور کرنا تاکہ ٹریڈنگ والیوم بڑھایا جا سکے۔

خلاصہ

یہ حکمت عملی مجموعی طور پر واضح اور سادہ ہے، دو طرفہ ٹریکنگ گرڈ ٹریڈنگ کے ذریعے مستحکم منافع حاصل کرتی ہے، تاہم اس میں کچھ ٹریڈنگ خطرات بھی موجود ہیں۔ مسلسل بہتری کے ذریعے بہتر نتائج حاصل کیے جا سکتے ہیں۔

- 1