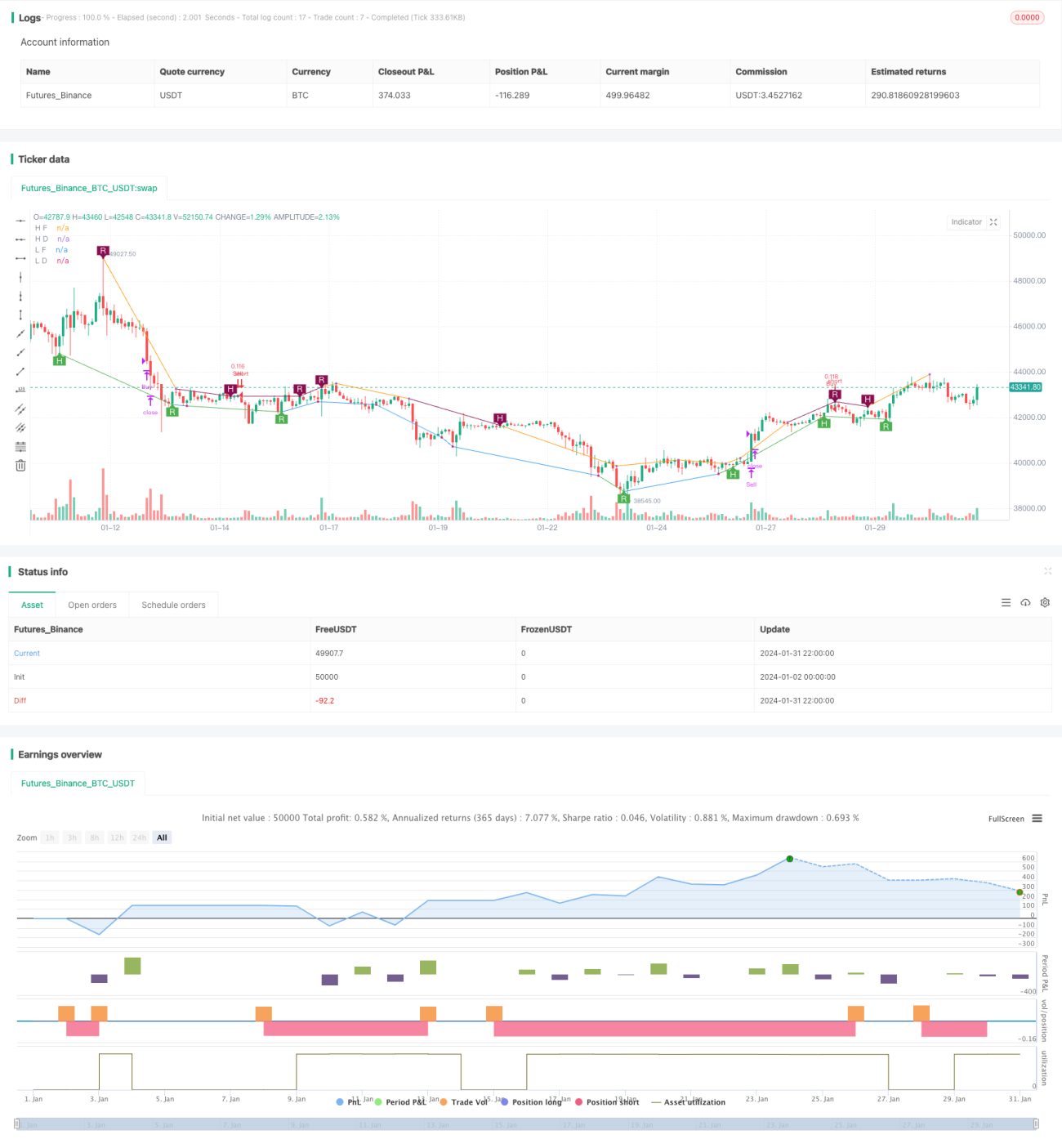

قیمت کی تفاوت پر مبنی رجحان کی تجارت کی حکمت عملی

خلاصہ

یہ حکمت عملی قیمت کی انحراف کے اشاروں پر مبنی ایک رجحان پر تجارت کی حکمت عملی ہے۔ یہ مختلف اشارے جیسے RSI، MACD، Stochastics وغیرہ کا استعمال کرتے ہوئے قیمت کے انحراف کے اشاروں کا پتہ لگاتی ہے اور مرے میتھ آسکیلیٹر کے ذریعے تصدیق کرتی ہے۔ جب قیمت کا انحراف کا اشارہ ظاہر ہوتا ہے اور آسکیلیٹر بھی موجودہ رجحان کی سمت کی تصدیق کرتا ہے تو اندراج کیا جاتا ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا مرکز قیمت کے انحراف کا نظریہ ہے۔ جب قیمت نئی بلندی بناتی ہے لیکن اشارہ نیا اونچا نہیں بناتا تو اسے ریچھ کی قیمت کا انحراف کہا جاتا ہے؛ جب قیمت نئی پستی بناتی ہے لیکن اشارہ نیا نیچا نہیں بناتا تو اسے بیل کی قیمت کا انحراف کہا جاتا ہے۔ یہ ظاہر کرتا ہے کہ رجحان میں تبدیلی ممکن ہے۔ حکمت عملی چوٹی اور تہہ کے پیٹرن کو آسکیلیٹر کے ساتھ ملا کر تجارتی اشاروں کی تصدیق کرتی ہے۔

خاص طور پر، حکمت عملی کے اندراج کی شرائط یہ ہیں:

- قیمت کے انحراف کا اشارہ ملنا، جس میں عام اور پوشیدہ انحراف شامل ہیں

- مرے میتھ آسکیلیٹر متعلقہ رجحانی علاقے میں ہو

باہر نکلنے کی شرط آسکیلیٹر کا وسط لائن کو واپس عبور کرنا ہے۔

فوائد کا تجزیہ

یہ حکمت عملی قیمت کے انحراف کے نظریے اور رجحان کی تصدیق کو یکجا کرتی ہے، جس کے درج ذیل فوائد ہیں:

- قیمت کے انحراف کے اشاروں سے ممکنہ رجحان کی تبدیلی کے نکات کا پتہ لگانا

- آسکیلیٹر کا استعمال موجودہ رجحان کی تصدیق کے لیے، جھوٹی بریک آؤٹ سے بچنا

- متعدد اشارے اور پیرامیٹرز کا مجموعہ، جسے لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے

- رجحان کی پیروی اور نقصان سے بچاؤ کا توازن

- منطقی اصول واضح ہیں، کوڈ کو بہتر بنانے کی کافی گنجائش ہے

خطرات کا تجزیہ

بنیادی خطرات درج ذیل پہلوؤں سے آتے ہیں:

- قیمت کے انحراف کے اشارے جھوٹے ہو سکتے ہیں، رجحان کی تبدیلی کی مکمل تصدیق نہیں کرتے

- آسکیلیٹر کے پیرامیٹرز کی غلط ترتیب سے تجارتی مواقع چھوٹ سکتے ہیں

- لمبی اور چھوٹی پوزیشنوں کا زیادہ جھکاؤ بڑے نقصان کا خطرہ لاتا ہے

- شدید اتار چڑھاؤ کے دوران تجارتی اخراجات اور سلپیج میں اضافہ ہو سکتا ہے

خطرات کم کرنے کے لیے اسٹاپ لاس، پوزیشن سائز ایڈجسٹمنٹ، اور پیرامیٹرز کی اصلاح کی سفارش کی جاتی ہے۔

بہتری کے راستے

اس حکمت عملی میں مزید بہتری کی گنجائش ہے:

- مشین لرننگ الگورتھم شامل کر کے پیرامیٹرز کی حقیقی وقت میں اصلاح

- خودکار اسٹاپ لاس تکنیکیں جیسے ٹریلنگ اسٹاپ، اوسط اسٹاپ شامل کرنا

- مزید اشارے اور فلٹر کی شرائط شامل کر کے سگنل ٹو شوٹ تناسب بہتر بنانا

- آسکیلیٹر کے پیرامیٹرز کو متحرک طور پر ایڈجسٹ کر کے رجحان کی تشخیص بہتر بنانا

- رسک مینجمنٹ کو بہتر بنانا، زیادہ سے زیادہ ڈرا ڈاؤن جیسی حدود مقرر کرنا

خلاصہ

یہ حکمت عملی قیمت کے انحراف کے نظریے اور رجحان کے تجزیے کے اشاروں کو یکجا کر کے ممکنہ رجحان کی تبدیلی کے نکات کو مؤثر طریقے سے دریافت کرتی ہے۔ بہتر رسک مینجمنٹ کے اقدامات کے ساتھ، اس حکمت عملی سے اچھی منافع کی شرح حاصل کی جا سکتی ہے۔ مستقبل میں مشین لرننگ جیسے اعلیٰ طریقوں سے اصلاح کر کے مستحکم اضافی منافع حاصل کیا جا سکتا ہے۔

- 1