Hull اشارے اور LSMA اشارے پر مبنی رجحان کی پیروی کرنے والی مقداری حکمت عملی

خاکہ

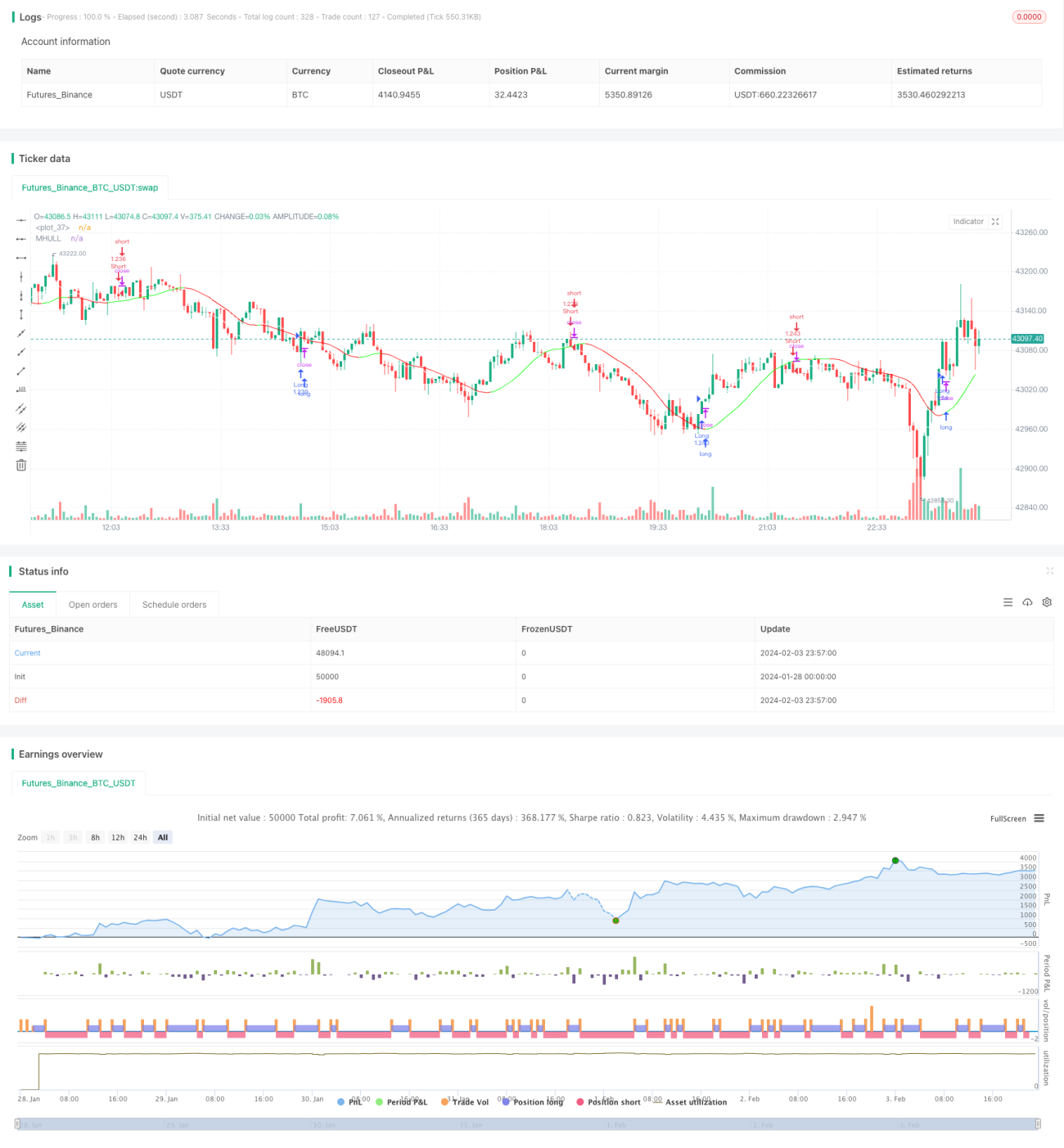

یہ حکمت عملی ہل اشارے اور LSMA (کم سے کم مربع حرکت پذیر اوسط) کے اشارے کو ملا کر رجحان کی سمت اور رجحان کے الٹ پلٹ کے نکات کی نشاندہی کرتی ہے، تاکہ رجحان کی پیروی کی جا سکے۔ جب ہل اشارہ صعودی رجحان دکھاتا ہے اور LSMA اوپر کی طرف ہل اشارے کو عبور کرتا ہے تو خریداری کی جاتی ہے۔ جب ہل اشارہ نزولی رجحان دکھاتا ہے اور LSMA نیچے کی طرف ہل اشارے کو عبور کرتا ہے تو فروخت کی جاتی ہے۔ یہ حکمت عملی درمیانی سے کم تعدد والی تجارت کے لیے موزوں ہے اور 1 منٹ کے ٹائم فریم پر استعمال کی جا سکتی ہے۔

حکمت عملی کا اصول

-

ہل اشارہ قدر کی رجحان سمت کا تعین کرنے کے لیے استعمال ہوتا ہے۔ جب درمیانی لکیر (MHULL) نیچے کی لکیر (LHULL) سے اوپر ہوتی ہے تو صعودی رجحان ظاہر ہوتا ہے۔ اس کے برعکس نزولی رجحان ظاہر ہوتا ہے۔

-

LSMA اشارہ رجحان کے الٹ پلٹ کے نکات کی نشاندہی کرنے کے لیے استعمال ہوتا ہے۔ جب LSMA اشارہ MHULL کو اوپر کی طرف عبور کرتا ہے تو صعودی رجحان کی تشکیل یا تیزرفتاری ظاہر ہوتی ہے۔ جب LSMA اشارہ MHULL کو نیچے کی طرف عبور کرتا ہے تو نزولی رجحان کی تشکیل یا تیزرفتاری ظاہر ہوتی ہے۔

-

دونوں کو ملا کر، جب ہل اشارہ صعودی رجحان دکھاتا ہے (MHULL > LHULL) اور LSMA MHULL کو اوپر کی طرف عبور کرتا ہے تو خریداری کی جاتی ہے۔ جب ہل اشارہ نزولی رجحان دکھاتا ہے (MHULL < LHULL) اور LSMA MHULL کو نیچے کی طرف عبور کرتا ہے تو فروخت کی جاتی ہے۔

-

اسٹاپ لاس کو قریب ترین اتار چڑھاؤ والے نقطے پر رکھا جاتا ہے۔ خریداری کے لیے اسٹاپ لاس حالیہ سب سے کم نقطے پر اور فروخت کے لیے حالیہ سب سے زیادہ نقطے پر رکھا جاتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

-

ہل اشارہ تیزی سے رد عمل ظاہر کرتا ہے اور رجحان کی تبدیلی کو بروقت پکڑ لیتا ہے۔ LSMA میں ہمواریت زیادہ ہوتی ہے اور الٹ پلٹ کے سگنلز کو درست اور قابل اعتماد طور پر پہچانتا ہے۔ دونوں کا مجموعہ موثر ثابت ہوتا ہے۔

-

LSMA کے کراس اوور کے ذریعے ہل اشارے کے جھوٹے سگنلز کو فلٹر کیا جاتا ہے، جس سے غلط تجارت کے امکانات کم ہوتے ہیں۔

-

اتار چڑھاؤ والے نقطوں کو اسٹاپ لاس کے طور پر استعمال کرکے سرمائے کی حفاظت کو زیادہ سے زیادہ یقینی بنایا جاتا ہے۔

-

یہ درمیانی سے کم تعدد والی تجارت کے لیے موزوں ہے اور 1 منٹ یا اس سے بھی کم ٹائم فریم پر استعمال کی جا سکتی ہے، جس سے اس کا اطلاق وسیع ہے۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

-

اتار چڑھاؤ والی مارکیٹ میں، ہل اشارہ اور LSMA متعدد بار کراس اوور کر سکتے ہیں جس سے تجارت بہت زیادہ بار بار ہو سکتی ہے۔ تجارت کی تعدد کو کم کرنے کے لیے مناسب طور پر پیرامیٹرز کو ایڈجسٹ کرنا چاہیے۔

-

اسٹاپ لاس کو اتار چڑھاؤ والے نقطوں پر رکھنا قلیل مدتی قیمت کی ایڈجسٹمنٹ کی وجہ سے متحرک ہو سکتا ہے، لہذا اسٹاپ لاس کے فاصلے کو مناسب طور پر بڑھانا چاہیے۔

-

LSMA اشارے میں تاخیر کی وجہ سے غلط تشخیص کا خطرہ ہو سکتا ہے۔ تصدیق کے لیے کینڈل سٹک پیٹرن جیسے دیگر اشارے استعمال کرنے چاہئیں۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

-

ہل اشارے اور LSMA کے پیرامیٹرز کو بہتر بنانا تاکہ ان کا مجموعہ مختلف مصنوعات اور وقت کے ادوار کے ساتھ زیادہ مطابقت رکھے۔

-

اتار چڑھاؤ، تجارتی حجم وغیرہ پر مبنی فلٹرنگ کی شرائط شامل کرنا تاکہ اتار چڑھاؤ والی مارکیٹ میں غلط تجارت سے بچا جا سکے۔

-

رجحان کے رجحان کا تعین کرنے میں معاون کے طور پر مشین لرننگ الگورتھم کا اضافہ۔

-

اہم سپورٹ اور ریزسٹنس والے علاقوں کا تعین کرنے کے لیے گہری سیکھنے جیسی تکنیکوں کا استعمال تاکہ اسٹاپ لاس زیادہ معقول ہو سکے۔

خلاصہ

یہ حکمت عملی ہل اشارے اور LSMA کے مشترکہ استعمال کے ذریعے رجحان کی سمت میں تبدیلی کا تعین کرتی ہے اور رجحان کی پیروی کرنے والی تجارت کو نافذ کرتی ہے۔ اس کے فوائد میں سادگی، تیز رد عمل، اور درمیانی سے کم تعدد والی مقداری تجارت میں وسیع پیمانے پر اطلاق شامل ہیں۔ فلٹرنگ کی شرائط، معاون تشخیص، اور اسٹاپ لاس الگورتھم وغیرہ میں مزید بہتری کے ذریعے بہتر حکمت عملی کے نتائج حاصل کیے جا سکتے ہیں۔

- 1