کاماریلا پیوٹ اور بولنگر بینڈز پر مبنی مقداری حکمت عملی

1

Follow

1802

Followers

جائزہ

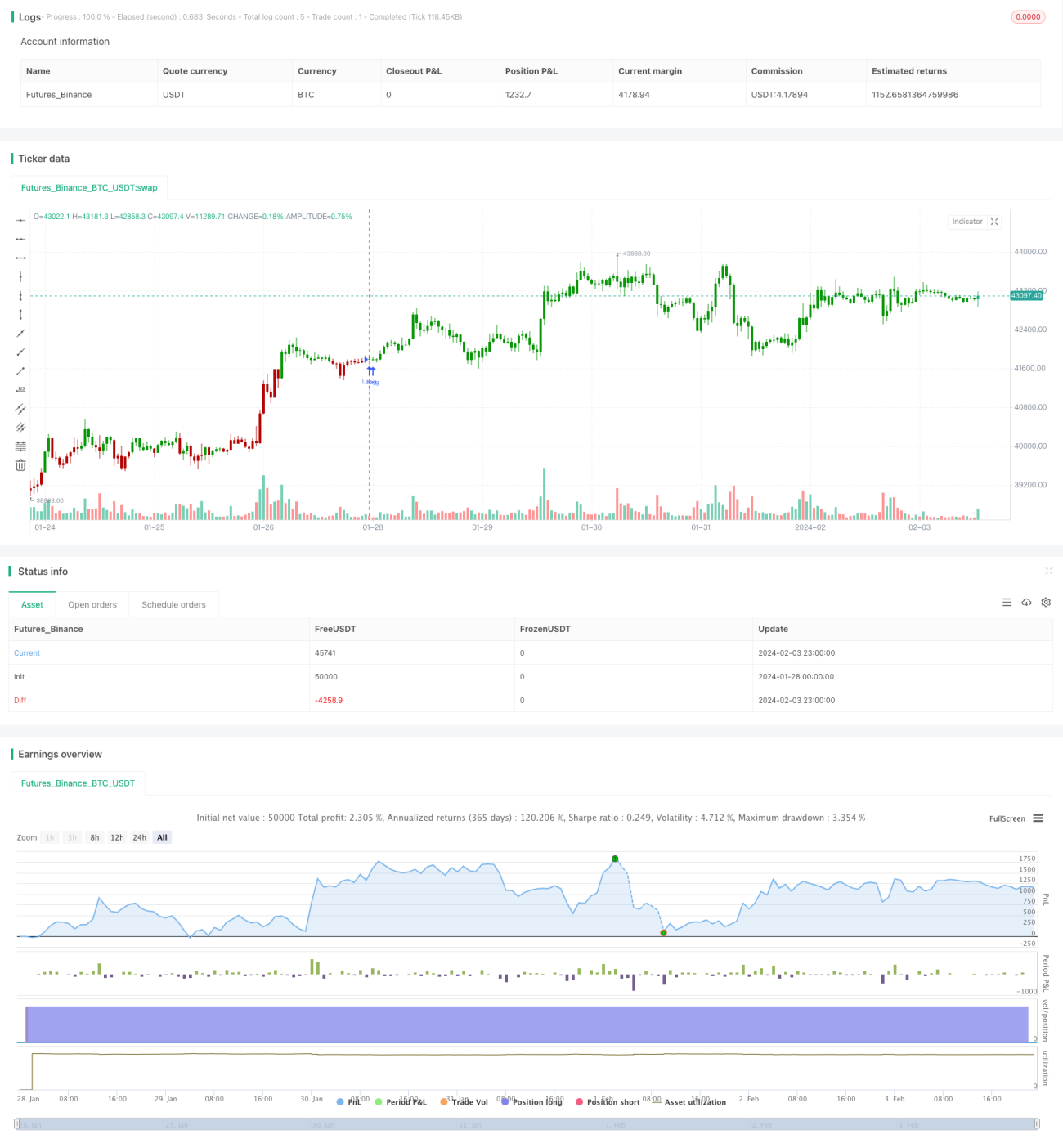

یہ حکمت عملی پہلے پچھلے تجارتی دن کی بلند ترین قیمت، کم ترین قیمت اور اختتامی قیمت کی بنیاد پر کاماچیلا پیوٹ پوائنٹس کا حساب لگاتی ہے۔ پھر بولنگر بینڈز انڈیکیٹر کے ساتھ قیمت کو فلٹر کیا جاتا ہے، اور جب قیمت پیوٹ پوائنٹ کو توڑتی ہے تو ٹریڈنگ سگنل پیدا ہوتے ہیں۔

حکمت عملی کا اصول

- پچھلے تجارتی دن کی بلند ترین قیمت، کم ترین قیمت اور اختتامی قیمت کا حساب لگائیں۔

- فارمولے کے مطابق کاماچیلا پیوٹ لائنز کا حساب لگائیں، جس میں اوپری بینڈ H4, H3, H2, H1 اور نچلے بینڈ L1, L2, L3, L4 شامل ہیں۔

- 20 دنوں کے بولنگر بینڈ کے اوپری اور نچلے بینڈ کا حساب لگائیں۔

- جب قیمت نچلے بینڈ کو اوپر سے عبور کرے تو لمبی پوزیشن لیں، اور جب اوپری بینڈ کو نیچے سے عبور کرے تو چھوٹی پوزیشن لیں۔

- سٹاپ لاس پوائنٹ بولنگر بینڈ کے اوپری یا نچلے بینڈ کے قریب رکھا جائے۔

فوائد کا تجزیہ

- کاماچیلا پیوٹ لائنز میں کئی اہم سپورٹ اور ریزسٹنس لیولز شامل ہیں، جس سے ٹریڈنگ سگنلز کی وشوسنییتا میں اضافہ ہوتا ہے۔

- بولنگر بینڈز انڈیکیٹر کے ساتھ ملا کر جھوٹے بریک آؤٹس کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے۔

- پیرامیٹرز کے متعدد امتزاج کی وجہ سے تجارت میں لچک ہے۔

خطرے کا تجزیہ

- بولنگر بینڈز کے پیرامیٹرز کی نامناسب ترتیب سے ٹریڈنگ سگنلز میں غلطی ہو سکتی ہے۔

- کاماچیلا پیوٹ پوائنٹس کے اہم لیولز کا حساب پچھلے دن کی قیمتوں پر انحصار کرتا ہے، جو راتوں رات جمپ سے متاثر ہو سکتے ہیں۔

- طویل اور مختصر دونوں پوزیشنوں میں نقصان کا خطرہ ہے۔

بہتری کے امکانات

- بولنگر بینڈز کے پیرامیٹرز کو بہتر بنائیں، بہترین پیرامیٹر امتزاج تلاش کریں۔

- جھوٹے بریک آؤٹ سگنلز کو فلٹر کرنے کے لیے دیگر انڈیکیٹرز کے ساتھ ملا کر استعمال کریں۔

- سٹاپ لاس کی حکمت عملی شامل کریں تاکہ فی ٹریڈ نقصان کو کم کیا جا سکے۔

خلاصہ

یہ حکمت عملی کاماچیلا پیوٹ لائنز اور بولنگر بینڈز انڈیکیٹر کو ملا کر استعمال کرتی ہے، اور جب قیمت اہم سپورٹ یا ریزسٹنس لیولز کو توڑتی ہے تو ٹریڈنگ سگنل پیدا کرتی ہے۔ پیرامیٹر آپٹیمائزیشن اور سگنل فلٹریشن کے ذریعے حکمت عملی کے منافع اور استحکام کو بہتر بنایا جا سکتا ہے۔ مجموعی طور پر، یہ حکمت عملی واضح تجارتی منطق پر مبنی ہے اور عملی طور پر لاگو کرنے کے قابل ہے، جو حقیقی تجارت میں آزمائش کے قابل ہے۔

Source

Pine

/*backtest

start: 2024-01-28 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/05/2020

// Camarilla pivot point formula is the refined form of existing classic pivot point formula. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1