دوہرا ریورسل مومینٹم انڈیکس حکمت عملی

جائزہ

دوہری ریورسل مومینٹم انڈیکس حکمت عملی ایک ایسی مشترکہ حکمت عملی ہے جو 123 ریورسل حکمت عملی اور ریلٹیو مومینٹم انڈیکس (RMI) حکمت عملی کو یکجا کرتی ہے۔ اس کا مقصد دوہرے سگنلز کے ذریعے تجارتی فیصلوں کی درستگی کو بڑھانا ہے۔

حکمت عملی کا اصول

یہ حکمت عملی دو حصوں پر مشتمل ہے:

-

123 ریورسل حکمت عملی

- جب کل کی بند قیمت پرسوں سے کم ہو، آج کی بند قیمت پرسوں سے زیادہ ہو، اور 9 دن کی Slow K لائن 50 سے نیچے ہو، تو لمبی پوزیشن لی جائے۔

- جب کل کی بند قیمت پرسوں سے زیادہ ہو، آج کی بند قیمت پرسوں سے کم ہو، اور 9 دن کی Fast K لائن 50 سے اوپر ہو، تو چھوٹی پوزیشن لی جائے۔

-

ریلٹیو مومینٹم انڈیکس (RMI) حکمت عملی

- RMI، RSI کی بنیاد پر مومینٹم عنصر شامل کرکے بنایا گیا ایک متغیر ہے۔ اس کا حساب کتاب یہ ہے: RMI = (اوپر کی طرف مومینٹم کا SMA) / (نیچے کی طرف مومینٹم کا SMA) * 100

- جب RMI اوور باؤٹ لائن سے نیچے ہو تو لمبی پوزیشن لی جائے؛ جب RMI اوور سولڈ لائن سے اوپر ہو تو چھوٹی پوزیشن لی جائے۔

یہ مشترکہ حکمت عملی صرف اس وقت تجارتی سگنل پیدا کرتی ہے جب 123 ریورسل اور RMI کے دوہرے سگنل ایک ہی سمت میں ہوں۔ اس سے غلط تجارتی مواقع کو مؤثر طریقے سے کم کیا جا سکتا ہے۔

حکمت عملی کے فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- دوہرے انڈیکیٹرز کا امتزاج سگنل کی درستگی بڑھاتا ہے۔

- ریورسل حکمت عملی کا استعمال، جو رینج مارکیٹ کے لیے موزوں ہے۔

- RMI انڈیکیٹر حساس ہے، مضبوط رجحان کے موڑ کو پہچان سکتا ہے۔

حکمت عملی کے خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- دوہری فلٹریشن کی وجہ سے کچھ تجارتی مواقع چھوٹ سکتے ہیں۔

- ریورسل سگنلز میں غلط تشخیص ممکن ہے۔

- RMI پیرامیٹرز کی غلط ترتیب اثر کو متاثر کر سکتی ہے۔

پیرامیٹرز کے امتزاج کو ایڈجسٹ کرکے اور انڈیکیٹر کے حساب کتاب کے طریقوں کو بہتر بنا کر ان خطرات کو کم کیا جا سکتا ہے۔

حکمت عملی کی اصلاح کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- مختلف پیرامیٹرز کے امتزاج کی جانچ، بہترین پیرامیٹرز تلاش کرنا۔

- مختلف ریورسل انڈیکیٹرز کے امتزاج جیسے KDJ، MACD وغیرہ آزمانا۔

- RMI فارمولے میں تبدیلی کرنا تاکہ یہ زیادہ حساس ہو۔

- سٹاپ لاس میکانزم شامل کرنا تاکہ ایک تجارت میں نقصان کو کنٹرول کیا جا سکے۔

- تجارتی حجم کو شامل کرنا تاکہ جعلی سگنلز سے بچا جا سکے۔

خلاصہ

دوہری ریورسل مومینٹم انڈیکس حکمت عملی دوہرے سگنل فلٹریشن اور پیرامیٹر کی اصلاح کے ذریعے تجارتی فیصلوں کی درستگی کو مؤثر طریقے سے بڑھا سکتی ہے اور غلط سگنلز کے امکان کو کم کر سکتی ہے۔ یہ رینج مارکیٹ کے لیے موزوں ہے اور ریورسل مواقع تلاش کر سکتی ہے۔ اس حکمت عملی کو پیرامیٹرز کو ایڈجسٹ کرکے اور انڈیکیٹر کے حساب کتاب کے طریقوں کو بہتر بنا کر مزید بہتر بنایا جا سکتا ہے اور لپس کے خطرے کو کم کیا جا سکتا ہے۔

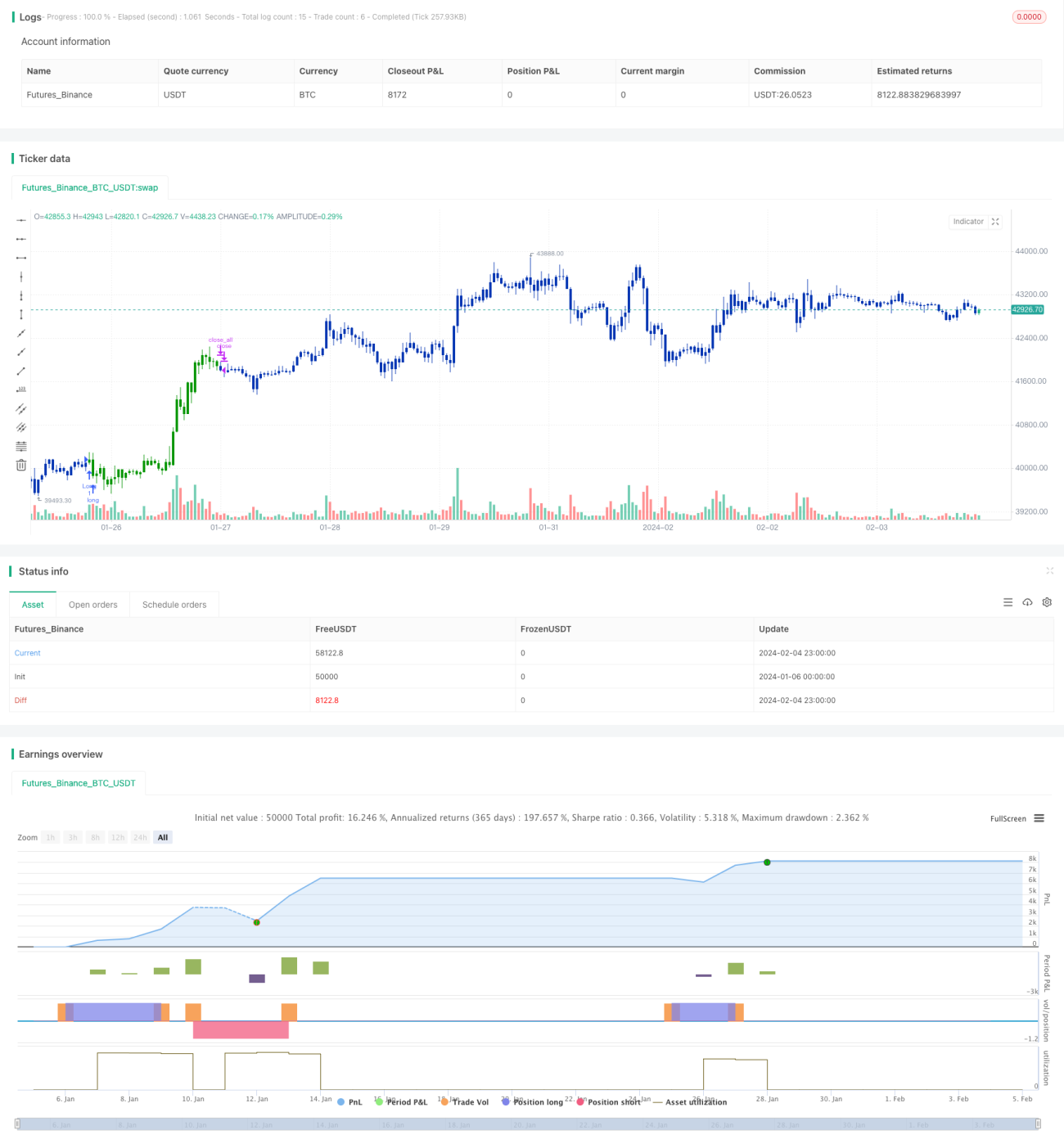

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. - 1