متحرک ڈھلوان ٹرینڈ لائن ٹریڈنگ اسٹریٹیجی

جائزہ

اس حکمت عملی کا بنیادی خیال متحرک ڈھلوان (Dynamic Slope) کے ذریعے قیمت کے رجحان کی سمت کا تعین کرنا ہے، اور بریک آؤٹ (Breakout) کی بنیاد پر تجارتی سگنل تیار کرنا ہے۔ خاص طور پر، یہ ریئل ٹائم میں قیمت کی نئی اونچائیوں اور نئی نیچائیوں کو ٹریک کرتا ہے، مختلف وقت کے وقفوں میں قیمت کی تبدیلی کی بنیاد پر متحرک ڈھلوان کا حساب لگاتا ہے، اور پھر قیمت کے ٹرینڈ لائن کو توڑنے کی بنیاد پر لانگ اور شارٹ سگنلز کا فیصلہ کرتا ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر درج ذیل مراحل پر مشتمل ہے:

-

زیادہ سے زیادہ اور کم سے کم قیمت کا تعین: ایک خاص مدت (مثلاً 20 کینڈل) کے اندر زیادہ سے زیادہ اور کم سے کم قیمت کو ٹریک کرنا، اور یہ دیکھنا کہ آیا نئی اونچائی یا نئی نیچائی بنی ہے۔

-

متحرک ڈھلوان کا حساب: نئی اونچائی یا نئی نیچائی بنانے والی کینڈل کے نمبر کو ریکارڈ کرنا، اور اس نقطہ سے ایک خاص مدت (مثلاً 9 کینڈل) بعد کے اونچے/نیچے نقطہ تک متحرک ڈھلوان کا حساب لگانا۔

-

ٹرینڈ لائنز کا خاکہ: متحرک ڈھلوان کی بنیاد پر اوپر اور نیچے کی طرف ٹرینڈ لائنز کھینچنا۔

-

ٹرینڈ لائنز کو بڑھانا اور اپ ڈیٹ کرنا: جب قیمت ٹرینڈ لائن کو توڑتی ہے تو، ٹرینڈ لائن کو بڑھایا اور اپ ڈیٹ کیا جاتا ہے۔

-

تجارتی سگنل: قیمت کے ٹرینڈ لائن کو توڑنے کی بنیاد پر لانگ اور شارٹ سگنلز کا فیصلہ کرنا۔

حکمت عملی کے فوائد

اس حکمت عملی کے درج ذیل فوائد ہیں:

-

رجحان کی سمت کا متحرک اندازہ، مارکیٹ کی تبدیلیوں سے نمٹنے میں لچک۔

-

نقصان کو روکنے کا معقول کنٹرول، ڈرا ڈاؤن (Drawdown) کم۔

-

بریک آؤٹ کے سگنل واضح، نفاذ آسان۔

-

پیرامیٹرز کو حسب ضرورت ترتیب دیا جا سکتا ہے، موافقت کی صلاحیت زیادہ۔

-

کوڈ کا ڈھانچہ واضح، سمجھنے اور دوبارہ ترقی دینے میں آسان۔

خطرات اور حل

اس حکمت عملی میں کچھ خطرات بھی ہیں:

-

جب رجحان میں اتار چڑھاؤ ہو تو نقصان کا امکان، فلٹر کی شرائط شامل کرنے کی سفارش کی جاتی ہے۔

-

جھوٹے بریک آؤٹ سگنلز زیادہ ہو سکتے ہیں، پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کیا جا سکتا ہے یا فلٹر کی شرائط شامل کی جا سکتی ہیں۔

-

مارکیٹ میں شدید اتار چڑھاؤ کے وقت نقصان روکنے کا خطرہ، نقصان روکنے کی حد بڑھائی جا سکتی ہے۔

-

بہتری کی گنجائش محدود، منافع کی صلاحیت محدود، مختصر مدت کی تجارت کے لیے موزوں۔

بہتری کی سمت

اس حکمت عملی میں بہتری کے لیے درج ذیل پہلوؤں پر کام کیا جا سکتا ہے:

-

مزید تکنیکی اشارے شامل کر کے سگنلز کو فلٹر کرنا۔

-

پیرامیٹرز کے امتزاج کو بہتر بنانا، بہترین پیرامیٹرز تلاش کرنا۔

-

نقصان روکنے کی حکمت عملی کو بہتر بنا کر خطرہ کم کرنا۔

-

داخلے کے وقفے کو خودکار طور پر ایڈجسٹ کرنے کی صلاحیت شامل کرنا۔

-

دوسری حکمت عملیوں کے ساتھ ملا کر مزید مواقع تلاش کرنا۔

خلاصہ

مجموعی طور پر یہ حکمت عملی متحرک ڈھلوان کی بنیاد پر رجحان کا اندازہ لگانے اور بریک آؤٹ ٹریڈ کرنے والی ایک موثر مختصر مدت کی حکمت عملی ہے۔ یہ درست اندازہ لگاتی ہے، خطرہ قابل کنٹرول ہے، اور مارکیٹ میں مختصر مدت کے مواقع حاصل کرنے کے لیے موزوں ہے۔ مزید پیرامیٹرز کو بہتر بنا کر اور فلٹر کی شرائط شامل کر کے اس حکمت عملی کی جیت کی شرح اور منافع کی سطح کو بہتر بنایا جا سکتا ہے۔

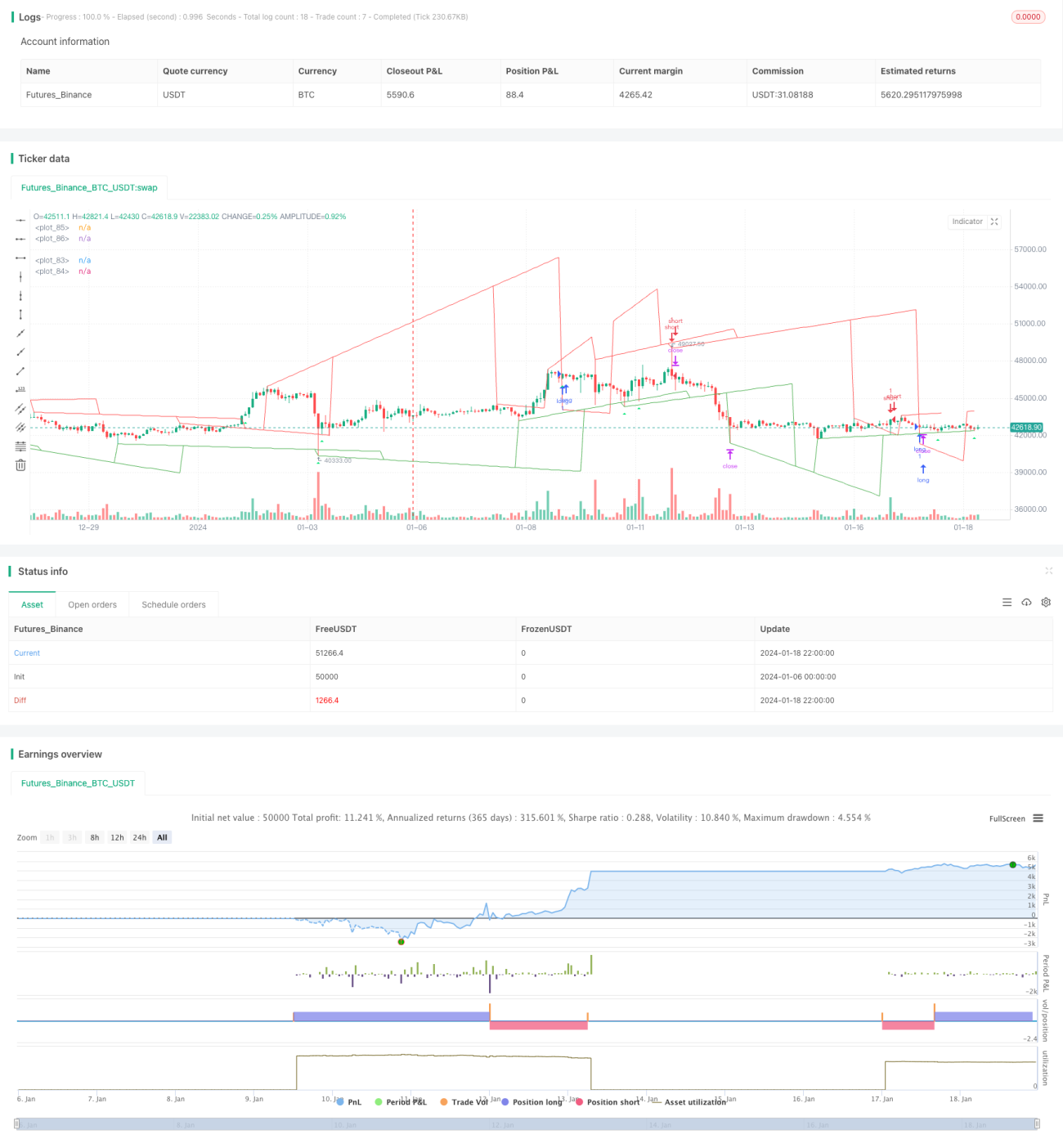

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1