تین K-لائنوں پر مبنی رجحان الٹنے کی حکمت عملی

تعارف

تین کینڈل ریورسل ٹرینڈ اسٹریٹیجی (Three Candle Reversal Trend Strategy) ایک مختصر مدت کی تجارتی حکمت عملی ہے جو تین مسلسل سبز یا سرخ کینڈلز اور اس کے بعد آنے والی ایک نگلنے والی کینڈل کی شناخت کے ذریعے قلیل مدتی رجحان کے الٹ جانے کا تعین کرتی ہے، اور مختلف تکنیکی اشاریوں کی مدد سے داخلے کے مواقع کو فلٹر کرتی ہے۔ یہ حکمت عملی 1:3 کے اسٹاپ لاس اور ٹیک پروفٹ تناسب کے ساتھ تجارت کرتی ہے، جس سے اضافی منافع حاصل کرنے میں مدد ملتی ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی منطق تین مسلسل سبز یا سرخ کینڈلز کے پیٹرن کی پہچان ہے، جو عام طور پر قلیل مدتی رجحان کے الٹ جانے کا اشارہ دیتا ہے۔ جب تین سرخ کینڈلز کا پتہ چلتا ہے، تو اگلی نگلنے والی سبز کینڈل کے ظاہر ہونے پر لمبی (لانگ) پوزیشن لی جاتی ہے؛ اس کے برعکس، جب تین سبز کینڈلز کا پتہ چلتا ہے، تو اگلی نگلنے والی سرخ کینڈل کے ظاہر ہونے پر چھوٹی (شارٹ) پوزیشن لی جاتی ہے۔ اس طرح مختصر مدت کے رجحان کے الٹ جانے کے مواقع کو بروقت پکڑا جا سکتا ہے۔

اس کے علاوہ، حکمت عملی میں داخلے کے مواقع کو فلٹر کرنے کے لیے متعدد تکنیکی اشاریے شامل کیے گئے ہیں۔ دو مختلف پیرامیٹرز کے ساتھ SMA اوسطی لکیریں استعمال کی جاتی ہیں، اور صرف اس وقت داخلے پر غور کیا جاتا ہے جب تیز رفتار لکیر سست رفتار لکیر کو اوپر سے عبور کرے۔ نیز، لکیری رجعت (Linear Regression) اشاریے کے ذریعے مارکیٹ کی اتار چڑھاؤ اور رجحان کی حالت کا تعین کیا جاتا ہے، اور صرف رجحانی حالت میں تجارت کی جاتی ہے۔ حکمت عملی میں ایک سوئچ بھی فراہم کیا گیا ہے جس کے ذریعے یہ انتخاب کیا جا سکتا ہے کہ آیا اوسطی خطوط کے سنہری کراس (Golden Cross) ہونے پر کینڈل پیٹرن کے ساتھ داخل ہوا جائے۔ ان اشاریوں کے مشترکہ تجزیے سے زیادہ تر شور کو فلٹر کیا جا سکتا ہے اور داخلے کی درستگی بڑھائی جا سکتی ہے۔

اسٹاپ لاس اور ٹیک پروفٹ کی ترتیب میں، حکمت عملی میں خطرہ منافع کا تناسب کم از کم 1:3 رکھنے کی شرط ہے۔ حالیہ N کینڈلز کے اتار چڑھاؤ کی بنیاد پر ATR اشاریہ کا حساب لگا کر، اتار چڑھاؤ کے فیصد کے ساتھ اسٹاپ لاس کی سطح مقرر کی جاتی ہے، اور پھر ٹیک پروفٹ کی سطح کا تعین کیا جاتا ہے۔ اس طرح ایک خاص حد کے خطرے کو قبول کرتے ہوئے مناسب اضافی منافع حاصل کیا جا سکتا ہے۔

حکمت عملی کے فوائد

- قلیل مدتی رجحان کے الٹ جانے کے نکات کی شناخت اور بروقت مواقع سے فائدہ اٹھانا

- متعدد اشاریوں سے فلٹرنگ، داخلے کی درستگی میں اضافہ

- اسٹاپ لاس اور ٹیک پروفٹ کا معقول نظام، خطرہ منافع کا مناسب تناسب

- سادہ پیرامیٹر کی ترتیب، سمجھنے اور چلانے میں آسان

حکمت عملی کے خطرات

- قلیل مدتی الٹ جانا ہمیشہ طویل مدتی رجحان کے الٹ جانے کی نمائندگی نہیں کرتا، اس لیے اعلیٰ وقت کے فریموں کے رجحان پر توجہ دینے کی ضرورت ہے۔ طویل مدت کی اوسطی لکیروں کو فلٹر کے طور پر سیٹ کیا جا سکتا ہے۔

- ایک ہی کینڈل پیٹرن کا سگنل غلط ہو سکتا ہے، لہٰذا دیگر معاون فیصلہ کن سگنلز شامل کرنے پر غور کیا جا سکتا ہے۔

- اسٹاپ لاس کی ترتیب حد سے زیادہ پر امید ہو سکتی ہے، اس لیے اسٹاپ لاس کی حد کو مناسب طور پر تنگ کیا جا سکتا ہے۔

- بیک ٹیسٹنگ کا ڈیٹا ناکافی ہے، لائیو ٹریڈنگ میں کچھ غیر یقینی صورتحال موجود ہے۔

حکمت عملی کی بہتری کے راستے

- اوسطی خطوط اور لکیری رجعت کے پیرامیٹرز کو ایڈجسٹ کرنا، رجحان کی حالت کے تعین کے اثر کو بہتر بنانا

- Stochastic جیسے دیگر معاون اشاریوں کو شامل کرنا، سگنلز کی درستگی کو بہتر بنانا

- ATR پیرامیٹرز اور اسٹاپ لاس کی حدود کے پیرامیٹرز کی ترتیب کو بہتر بنانا، خطرے اور منافع کو متوازن کرنا

- رجحان کے بریک آؤٹ پوائنٹس کو ٹریک کرنے کا طریقہ کار شامل کرنا، منافع کمانے کی صلاحیت بڑھانا

- زیادہ سخت فنڈ مینجمنٹ کی حکمت عملی تشکیل دینا، تجارتی خطرے کو کنٹرول کرنا

خلاصہ

مجموعی طور پر، تین کینڈل ریورسل ٹرینڈ اسٹریٹیجی ایک سادہ قیمت کے پیٹرن کو متعدد معاون اشاریوں کے ساتھ ملا کر، مناسب خطرہ منافع کے توازن پر مبنی قلیل مدتی تجارتی حکمت عملی ہے۔ یہ کم پیچیدگی کے ساتھ اچھی کارکردگی فراہم کرتی ہے، سرمایہ کاروں کی توجہ اور جانچ کے لائق ہے، اور اس میں بہتری کی بہت گنجائش بھی ہے۔ پیرامیٹر کی اصلاح اور قواعد کی تکمیل کے ذریعے، یہ ایک مستحکم اور موثر مقداری تجارتی حکمت عملی بن سکتی ہے۔

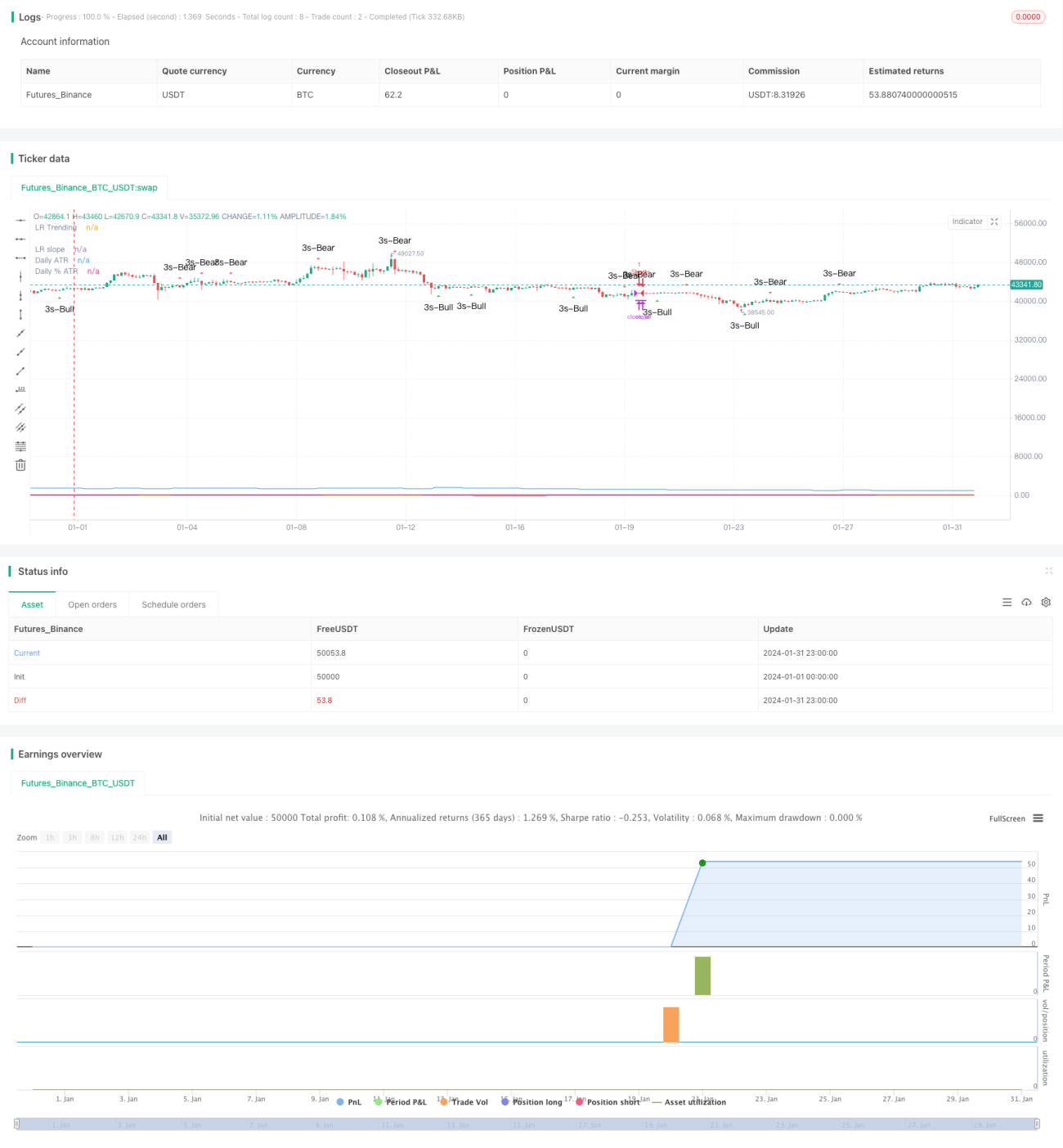

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1