اعلی حجم کے بریک آؤٹ مرکب سود پوزیشن حکمت عملی

جائزہ

اس حکمت عملی کا بنیادی خیال زیادہ تجارتی حجم کی صورت میں بریک آؤٹ کا تعاقب کرنا ہے، اور رسک بجٹ کے فیصد اور 250 گنا مصنوعی لیوریج کے ذریعے کمپاؤنڈ پوزیشنز حاصل کرنا ہے۔ اس کا مقصد زیادہ فروخت کے دباؤ کے بعد ممکنہ ریورسل مواقع کو پکڑنا ہے۔

حکمت عملی کا اصول

جب درج ذیل شرائط پوری ہوں تو لانگ پوزیشن میں داخل ہوں:

- تجارتی حجم صارف کی متعین کردہ حد (volThreshold) سے زیادہ ہو۔

- موجودہ کینڈل کی کم ترین قیمت پچھلی کینڈل کی کم ترین قیمت سے کم ہو (lowLowerThanPrevBar)۔

- موجودہ کینڈل کا اختتامی منفی ہو اور پچھلی کینڈل کے اختتامی سے زیادہ ہو (negativeCloseWithHighVolume)۔

- کوئی کھلی لانگ پوزیشن موجود نہ ہو (strategy.position_size == 0)۔

پوزیشن کے سائز کا حساب:

- اکاؤنٹ ایکویٹی (equity) کے رسک فیصد (riskPercentage) کی بنیاد پر رسک کی رقم کا تعین۔

- رسک کی رقم کو مصنوعی لیوریج (leverage، بطور ڈیفالٹ 250) سے ضرب دے کر کنٹریکٹس کی تعداد حاصل کی جائے۔

باہر نکلنے کا اصول:

لانگ پوزیشن کے منافع/نقصان کا فیصد (posProfitPct) جب اسٹاپ لاس (-0.14%) یا ٹیک پروفٹ (4.55%) کو چھوئے تو پوزیشن بند کر دی جائے۔

فوائد کا تجزیہ

اس حکمت عملی کے فوائد:

- زیادہ تجارتی حجم کی صورت میں رجحان کے ریورسل کے مواقع کو پکڑنا۔

- کمپاؤنڈ پوزیشن مینجمنٹ کی وجہ سے منافع میں تیزی سے اضافہ۔

- اسٹاپ لاس اور ٹیک پروفٹ کی مناسب ترتیب جو رسک کنٹرول میں مددگار ہے۔

رسک کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- 250 گنا لیوریج نقصان کو بڑھا سکتا ہے۔

- سلپیج، فیس اور مارجن جیسے حقیقی تجارتی عوامل کو مدنظر نہیں رکھا گیا۔

- بار بار بیک ٹیسٹنگ اور پیرامیٹرز کی اصلاح کی ضرورت ہے، اور لائیو ٹریڈنگ میں تصدیق درکار ہے۔

خطرات کو کم کرنے کے طریقے:

- لیوریج کے تناسب کو مناسب حد تک کم کرنا۔

- اسٹاپ لاس کی حد کو بڑھانا۔

- حقیقی تجارتی اخراجات کو مدنظر رکھنا۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- لیوریج کے سائز کو متحرک طور پر ایڈجسٹ کرنا۔

- اسٹاپ لاس اور ٹیک پروفٹ کی شرائط کو بہتر بنانا۔

- رجحان کا فلٹر شامل کرنا۔

- اسٹاک کی مخصوص خصوصیات کے مطابق پیرامیٹرز کو ایڈجسٹ کرنا۔

خلاصہ

یہ حکمت عملی مجموعی طور پر سادہ اور براہ راست ہے، جو ریورسل مواقع کو پکڑ کر اضافی منافع حاصل کرتی ہے۔ تاہم اس میں کچھ خطرات بھی ہیں، اس لیے لائیو ٹریڈنگ میں احتیاط سے تصدیق ضروری ہے۔ پیرامیٹرز اور حکمت عملی کے ڈھانچے کو بہتر بنا کر اسے زیادہ مستحکم اور عملی طور پر کارگر بنایا جا سکتا ہے۔

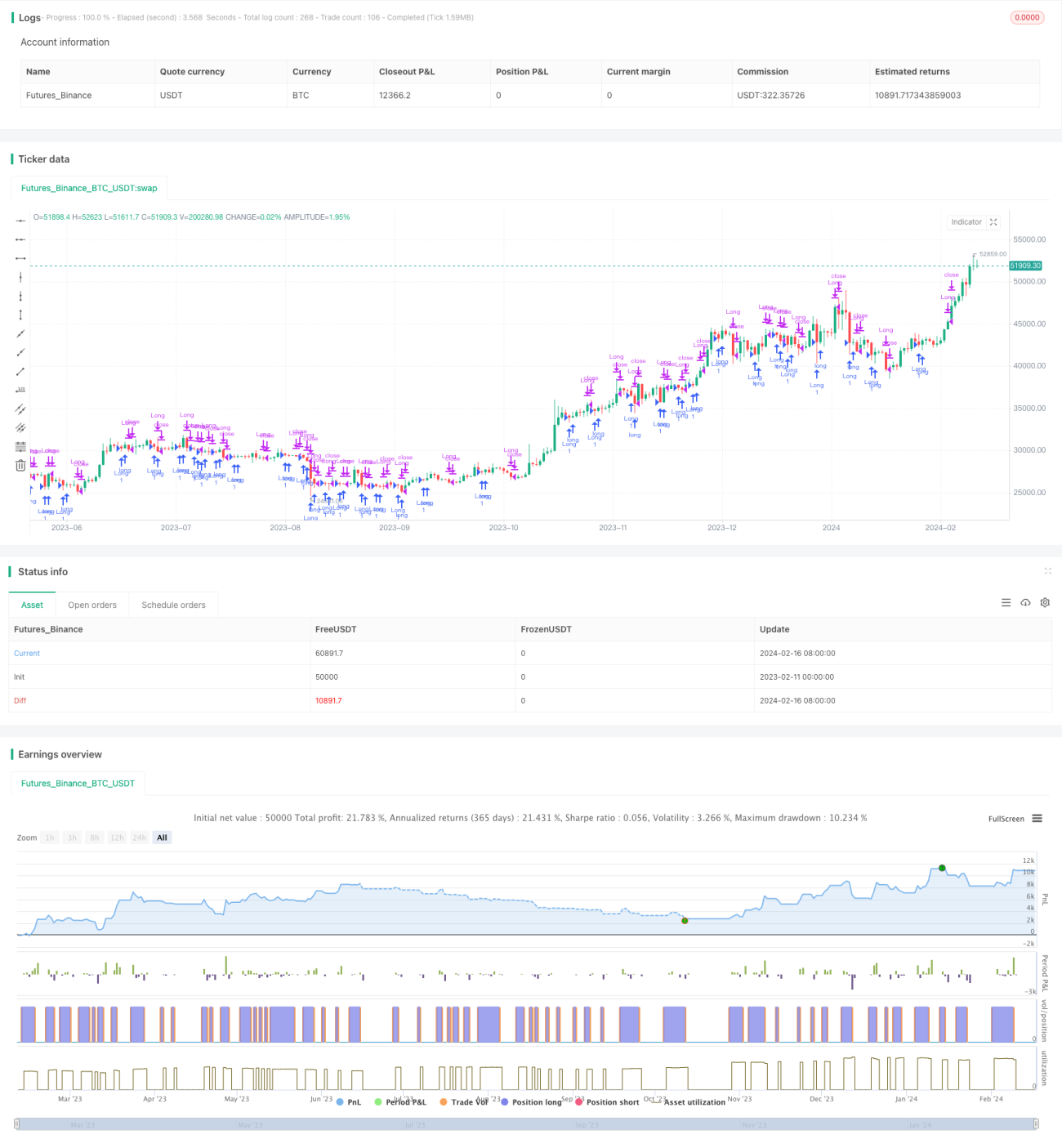

/*backtest

start: 2023-02-11 00:00:00

end: 2024-02-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Volume Low Breakout (Compounded Position Size)", overlay=true, initial_capital=1000)

// Define input for volume threshold- 1