ABCD شکل پر مبنی اور سٹاپ لاس ٹریکنگ اور ٹیک پرافٹ ٹریکنگ کے ساتھ ایک نیا مقداری تجارتی حکمت عملی

۱۔ حکمت عملی کا جائزہ

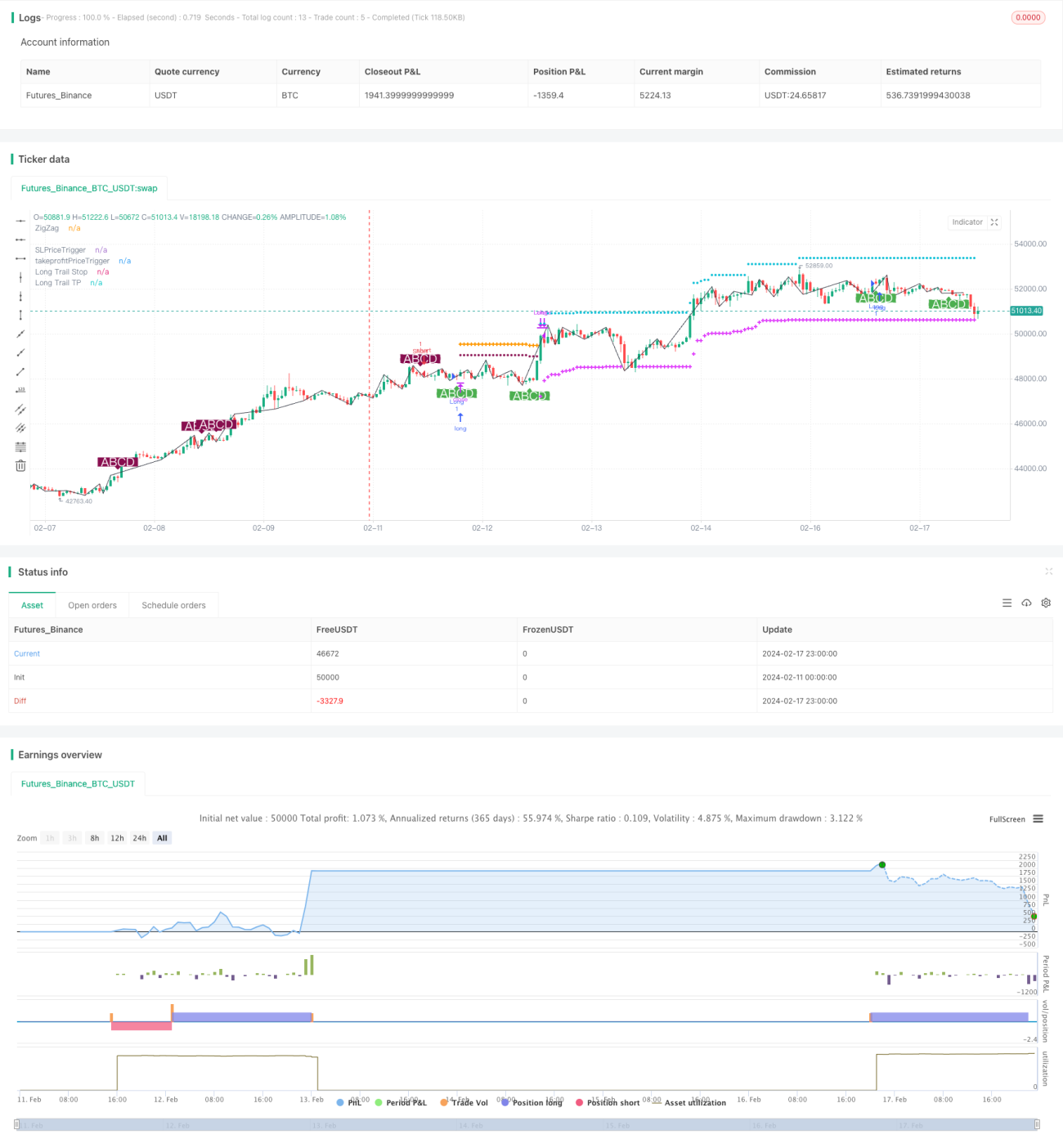

اس حکمت عملی کا نام "بہترین ABCD پیٹرن ٹریڈنگ اسٹریٹیجی (اسٹاپ لاسس ٹریلنگ اور ٹیک پرافٹ ٹریلنگ کے ساتھ)" ہے۔ یہ ایک مقداری حکمت عملی ہے جو واضح ABCD قیمت پیٹرن ماڈل پر مبنی تجارتی کارروائیاں کرتی ہے۔ بنیادی خیال یہ ہے کہ مکمل ABCD پیٹرن ماڈل کی شناخت کے بعد، پیٹرن کی سمت کے مطابق لمبی یا مختصر پوزیشن کھولی جائے، اور پوزیشن کو منظم کرنے کے لیے اسٹاپ لاسس اور ٹیک پرافٹ ٹریلنگ سیٹ کی جائے۔

۲۔ حکمت عملی کا اصول

-

بولنگر بینڈز کی مدد سے قیمت کے اوپر اور نیچے کے تقسیم پوائنٹس کی شناخت کی جاتی ہے، جس سے قیمت کا ZigZag منحنی حاصل ہوتا ہے۔

-

ZigZag منحنی پر مکمل ABCD پیٹرن ماڈل کی شناخت کی جاتی ہے، A, B, C, D چار پوائنٹس کو ایک مخصوص تناسب کے تعلق کو پورا کرنا ہوتا ہے۔ جب اہل ABCD پیٹرن کی شناخت ہو جائے تو لمبی یا مختصر پوزیشن کھولی جاتی ہے۔

-

لمبی یا مختصر پوزیشن کھولنے کے بعد خطرے کو کنٹرول کرنے کے لیے اسٹاپ لاسس ٹریلنگ سیٹ کی جاتی ہے۔ شروع میں ایک مقررہ اسٹاپ لاسس استعمال کیا جاتا ہے، اور جب منافع ایک خاص تناسب تک پہنچ جائے تو کچھ منافع کو بند کرنے کے لیے متحرک اسٹاپ لاسس میں تبدیل کر دیا جاتا ہے۔

-

اسی طرح، ٹیک پرافٹ لائن کے لیے بھی ٹریلنگ سیٹ کی جاتی ہے تاکہ کافی منافع حاصل کرنے کے بعد بروقت منافع لیا جا سکے اور منافع کی واپسی سے بچا جا سکے۔ ٹیک پرافٹ ٹریلنگ بھی دو مراحل پر مشتمل ہے، پہلے ایک مقررہ ٹیک پرافٹ استعمال کیا جاتا ہے تاکہ کچھ منافع حاصل کیا جا سکے، پھر قیمت کی پیروی جاری رکھنے کے لیے متحرک ٹیک پرافٹ میں تبدیل کر دیا جاتا ہے۔

-

جب قیمت متحرک اسٹاپ لاسس یا ٹیک پرافٹ کو متحرک کرتی ہے تو پوزیشن بند کر دی جاتی ہے، اور ایک تجارتی دور مکمل ہو جاتا ہے۔

۳۔ حکمت عملی کے فوائد کا تجزیہ

- ۱. بولنگر بینڈز کی مدد سے ZigZag منحنی کی شناخت کرنا روایتی ZigZag منحنی کی واپسی کے مسئلے سے بچاتا ہے، جس سے تجارتی اشارے زیادہ قابل اعتماد ہوتے ہیں۔

- ۲. ABCD پیٹرن ٹریڈنگ ماڈل پختہ اور مستحکم ہے، اور تجارتی مواقع کافی ہوتے ہیں۔ اس کے علاوہ ABCD پیٹرن کی سمت واضح ہوتی ہے، جس سے داخلے کی سمت کا تعین آسان ہوتا ہے۔

- ۳. دو مرحلوں پر مشتمل اسٹاپ لاسس اور ٹیک پرافٹ ٹریلنگ سیٹ کرنا خطرے کو بہتر طریقے سے کنٹرول کرنے اور منافع حاصل کرنے میں مدد کرتا ہے۔ متحرک اسٹاپ لاسس اور ٹیک پرافٹ حکمت عملی کو زیادہ لچکدار بناتا ہے۔

- ۴. حکمت عملی کے پیرامیٹرز مناسب طریقے سے ڈیزائن کیے گئے ہیں، اسٹاپ لاسس اور ٹیک پرافٹ کے فیصد، اور متحرک آغاز کے فیصد کو اپنی مرضی کے مطابق بنایا جا سکتا ہے، جس سے استعمال میں لچک آتی ہے۔

- ۵. یہ حکمت عملی کسی بھی مصنوع پر استعمال کی جا سکتی ہے، بشمول فاریکس، کریپٹو کرنسی، اور اسٹاک انڈیکس وغیرہ۔

۴۔ حکمت عملی کے خطرات کا تجزیہ

- ۱. اگرچہ ABCD پیٹرن نسبتاً واضح ہے، لیکن تجارتی مواقع نسبتاً محدود ہیں، اور کافی تجارتی تعدد کی ضمانت نہیں دے سکتے۔

- ۲. اتار چڑھاؤ والی مارکیٹ میں، اسٹاپ لاسس اور ٹیک پرافٹ بار بار متحرک ہو سکتے ہیں۔ اس صورت میں مناسب طریقے سے پیرامیٹرز کو ایڈجسٹ کرنے اور اسٹاپ لاسس اور ٹیک پرافٹ کی حد کو بڑھانے کی ضرورت ہے۔

- ۳. تجارتی مصنوع کی لیکویڈٹی پر توجہ دینے کی ضرورت ہے۔ کم لیکویڈیٹی والے اثاثوں میں، اسٹاپ لاسس اور ٹیک پرافٹ کو درست طریقے سے عمل میں لانا مشکل ہوتا ہے۔

- ۴. حکمت عملی تجارتی اخراجات کے لیے حساس ہے، اس لیے کم فیس والے بروکر اور اکاؤنٹ کا انتخاب کرنا ضروری ہے۔

- ۵. کچھ پیرامیٹرز کو مزید بہتر بنایا جا سکتا ہے، جیسے متحرک اسٹاپ لاسس اور ٹیک پرافٹ کے آغاز کی شرائط کے لیے مزید اقدار کی جانچ کر کے بہترین پوائنٹ تلاش کیا جا سکتا ہے۔

۵۔ حکمت عملی کی بہتری کی سمتیں

- ۱. دوسرے اشارے کے ساتھ مل کر مزید فلٹرنگ شرائط سیٹ کی جا سکتی ہیں تاکہ کچھ HW پیٹرن سے بچا جا سکے۔ اس سے غیر موثر تجارت کی تعداد کم ہو سکتی ہے۔

- ۲. مارکیٹ کے تین حصوں والے ڈھانچے کا تعین شامل کیا جا سکتا ہے، اور صرف تیسرے حصے کی مارکیٹ میں تجارتی مواقع تلاش کیے جا سکتے ہیں۔ اس سے حکمت عملی کی جیت کی شرح میں اضافہ ہو سکتا ہے۔

- ۳. شروع کی سرمائے کے سائز کی جانچ اور بہتری کی جا سکتی ہے تاکہ بہترین شروع کی سرمائے کی سطح تلاش کی جا سکے۔ بہت بڑا یا بہت چھوٹا دونوں بہترین منافع کی شرح حاصل کرنے کے لیے نقصان دہ ہیں۔

- ۴. نمونے سے باہر کے ڈیٹا کی جانچ کی جا سکتی ہے تاکہ پیرامیٹرز کی مضبوطی کی تصدیق ہو سکے۔ حکمت عملی کے درمیانی اور طویل مدتی استحکام کو سمجھنے کے لیے یہ بہت ضروری ہے۔

- ۵. متحرک اسٹاپ لاسس/ٹیک پرافٹ کے آغاز کی شرائط اور سلپیج کے سائز کو بہتر بنانا جاری رکھیں تاکہ حکمت عملی کے عمل کی کارکردگی بہتر ہو سکے۔ سیٹنگز کی بہتری کبھی ختم نہیں ہوتی۔

۶۔ حکمت عملی کا خلاصہ

یہ حکمت عملی بنیادی طور پر ABCD قیمت پیٹرن پر انحصار کرتی ہے جس کی بنیاد پر فیصلہ اور داخلہ کیا جاتا ہے۔ خطرے اور منافع کو منظم کرنے کے لیے دو مرحلوں پر مشتمل اسٹاپ لاسس اور ٹیک پرافٹ ٹریلنگ سیٹ کی جاتی ہے۔ حکمت عملی نسبتاً پختہ اور مستحکم ہے، لیکن تجارتی تعدد کم ہو سکتی ہے۔ ہم مزید فلٹرنگ شرائط شامل کر کے زیادہ موثر تجارتی مواقع حاصل کر سکتے ہیں۔ اس کے علاوہ، پیرامیٹرز اور سرمائے کے سائز کو بہتر بنانا جاری رکھنے سے حکمت عملی کی مستحکم منافع بخش صلاحیت میں مزید اضافہ ہو سکتا ہے۔ مجموعی طور پر، یہ حکمت عملی واضح تصورات پر مبنی ہے، سمجھنے اور لاگو کرنے میں آسان ہے، اور یہ ایک قابل قدر مقداری تجارتی حکمت عملی ہے جسے گہرائی سے تحقیق اور استعمال کیا جانا چاہیے۔

- 1