چینل بریک آؤٹ ریورسل ٹریڈنگ حکمت عملی

جائزہ

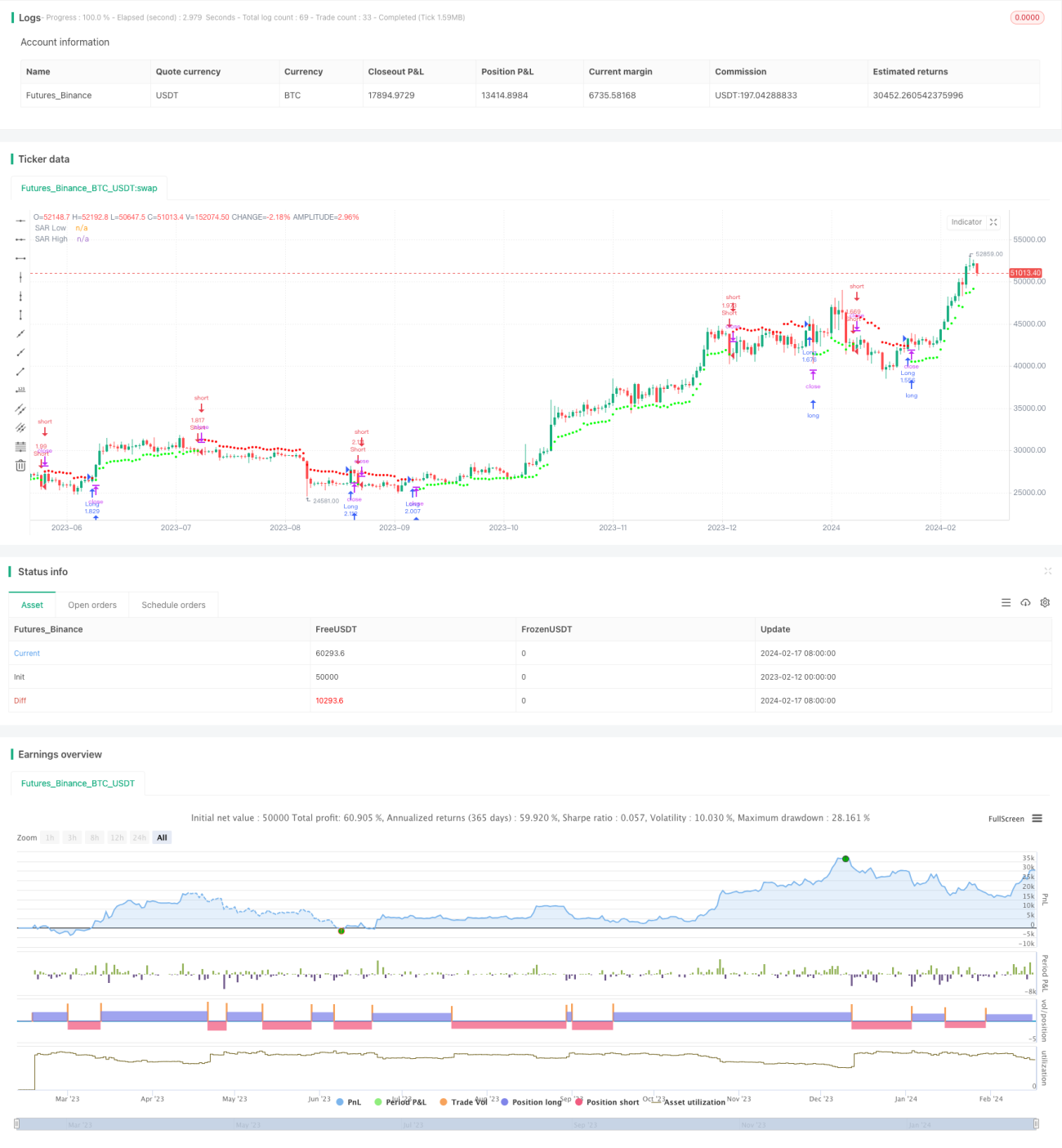

چینل بریک آؤٹ ریورسل ٹریڈنگ کی حکمت عملی ایک ریورسل ٹریڈنگ کا طریقہ ہے جو قیمت کے چینل کی پیروی کرتے ہوئے متحرک منافع اور نقصان کے مقامات طے کرتی ہے۔ یہ وزنی موو ایوریج طریقے سے قیمت کے چینل کا حساب لگاتی ہے اور جب قیمت چینل سے باہر نکلتی ہے تو لانگ یا شارٹ پوزیشن کھولتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی پہلے وائلڈر کے ایوریج ٹرو رینج (ATR) انڈیکیٹر کے ذریعے قیمت کی اتار چڑھاؤ کا حساب لگاتی ہے۔ اس کے بعد ATR کی قدر کی بنیاد پر ایوریج رینج کانسٹینٹ (ARC) نکالا جاتا ہے۔ ARC قیمت کے چینل کی نصف چوڑائی ہوتی ہے۔ پھر چینل کے اوپری اور نچلے کناروں کا حساب لگایا جاتا ہے، جو منافع اور نقصان کے مقامات ہوتے ہیں اور انہیں SAR پوائنٹس کہا جاتا ہے۔ جب قیمت اوپری کنارے سے باہر نکلتی ہے تو شارٹ کیا جاتا ہے، اور جب نچلے کنارے سے باہر نکلتی ہے تو لانگ کیا جاتا ہے۔

تفصیل سے، پہلے حالیہ N کینڈلز کا ATR نکالا جاتا ہے۔ پھر ایک عددی عنصر سے ATR کو ضرب دے کر ARC حاصل کیا جاتا ہے۔ ARC کو عددی عنصر سے ضرب دے کر چینل کی چوڑائی کو کنٹرول کیا جا سکتا ہے۔ ARC کو N کینڈلز کی سب سے زیادہ بند قیمت میں شامل کر کے چینل کا اوپری کنارہ (یعنی ہائی SAR) حاصل ہوتا ہے۔ ARC کو سب سے کم بند قیمت سے گھٹا کر چینل کا نچلا کنارہ (یعنی لو SAR) حاصل ہوتا ہے۔ اگر قیمت کا بند اوپری کنارے سے باہر ہو تو شارٹ کیا جاتا ہے، اور اگر بند نچلے کنارے سے باہر ہو تو لانگ کیا جاتا ہے۔

حکمت عملی کے فوائد

- قیمت کی اتار چڑھاؤ کا استعمال کرتے ہوئے خودکار چینل جو مارکیٹ کی تبدیلیوں کو ٹریک کرتا ہے۔

- ریورسل ٹریڈنگ، جو رجحان کی تبدیلی والی مارکیٹ کے لیے موزوں ہے۔

- متحرک منافع اور نقصان کے مقامات جو منافع کو محفوظ رکھتے ہیں اور خطرے کو کنٹرول کرتے ہیں۔

حکمت عملی کے خطرات

- ریورسل ٹریڈنگ میں نقصان میں پھنسنے کا امکان زیادہ ہوتا ہے، اس لیے پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کرنا ضروری ہے۔

- بڑی اتار چڑھاؤ والی مارکیٹ میں پوزیشنیں جلد بند ہو سکتی ہیں۔

- نامناسب پیرامیٹرز کی وجہ سے بار بار ٹریڈنگ ہو سکتی ہے۔

حل:

- ATR کے دورانیے اور ARC کے عددی عنصر کو بہتر بنائیں تاکہ چینل کی چوڑائی مناسب رہے۔

- داخلے کے وقت کو فلٹر کرنے کے لیے رجحان کے اشارے شامل کریں۔

- ATR کے دورانیے کو بڑھائیں تاکہ ٹریڈنگ کی فریکوئنسی کم ہو۔

حکمت عملی کی بہتری کے شعبے

- ATR کے دورانیے اور ARC کے عددی عنصر کو بہتر بنانا۔

- پوزیشن کھولنے کی شرائط میں اضافہ، مثلاً MACD انڈیکیٹر کا استعمال۔

- نقصان روکنے کی حکمت عملی شامل کرنا۔

خلاصہ

چینل بریک آؤٹ ریورسل ٹریڈنگ کی حکمت عملی قیمت کی تبدیلیوں کی پیروی کے لیے چینل کا استعمال کرتی ہے، اتار چڑھاؤ بڑھنے پر ریورسل پوزیشن کھولتی ہے، اور خودکار متحرک منافع اور نقصان کے مقامات طے کرتی ہے۔ یہ حکمت عملی ان مارکیٹوں کے لیے موزوں ہے جہاں رجحان کی تبدیلی غالب ہو، اور اگر ریورسل پوائنٹس کا درست اندازہ لگایا جائے تو اچھا منافع حاصل کیا جا سکتا ہے۔ تاہم، نقصان کے مقامات کو بہت زیادہ ڈھیلا رکھنے اور پیرامیٹرز کی بہتری پر توجہ دینا ضروری ہے۔

- 1