DEMA کراس اوور رجحان کی پیروی کی حکمت عملی

خلاصہ

یہ حکمت عملی دوہری ایکسپونینشل مووِنگ ایوریج (ڈی ای ایم اے) کے کراس پر تجارتی سگنلز پر مبنی ہے، جو رجحان کی پیروی کرتی ہے اور خود بخود نقصان روک اور منافع بند کرنے کے مقررہ نکات مرتب کرتی ہے۔ اس حکمت عملی کے فوائد میں واضح تجارتی سگنل، لچکدار نقصان روک اور منافع بند کے نکات، اور خطرے کو مؤثر طریقے سے قابو کرنے کی صلاحیت شامل ہیں۔

حکمت عملی کا اصول

-

فاسٹ لائن ڈی ای ایم اے (8 دن)، سلو لائن ڈی ای ایم اے (24 دن)، اور ایک معاون لائن ڈی ای ایم اے (کنفیگر ایبل) کا حساب لگائیں۔

-

جب فاسٹ لائن سلو لائن کو اوپر سے عبور کرتی ہے (گولڈن کراس) تو خرید (لانگ) سگنل پیدا ہوتا ہے؛ جب فاسٹ لائن سلو لائن کو نیچے سے عبور کرتی ہے (ڈیتھ کراس) تو فروخت (شارٹ) سگنل پیدا ہوتا ہے۔

-

تجارتی سگنلز کی فلٹریشن شامل کی گئی ہے: صرف اس وقت سگنل پیدا ہوتا ہے جب معاون لائن کی موجودہ دن کی قدر پچھلے دن سے زیادہ ہو، تاکہ جھوٹے بریک آؤٹ سے بچا جا سکے۔

-

رجحان کی پیروی کرنے والا نقصان روک میکانزم استعمال کیا گیا ہے، جس میں نقصان روک لائن قیمت کی حرکت کے ساتھ ایڈجسٹ ہوتی ہے، اس بات کو یقینی بناتے ہوئے کہ نقصان روک کا مقام کچھ منافع کو محفوظ کر لے۔

-

اس کے ساتھ ساتھ فی صد کی بنیاد پر مقررہ نقصان روک اور منافع بند کے نکات بھی مرتب کیے گئے ہیں تاکہ ایک ہی تجارت میں زیادہ سے زیادہ نقصان اور منافع کو کنٹرول کیا جا سکے۔

حکمت عملی کے فوائد

-

تجارتی سگنل واضح ہیں، جس سے داخلے اور خارج ہونے کے اوقات کا تعین آسان ہو جاتا ہے۔

-

ڈبل ڈی ای ایم اے الگورتھم زیادہ ہموار ہے، زیادہ اصلاح سے بچاتا ہے، اور سگنلز زیادہ قابل اعتماد ہیں۔

-

معاون لائن کی فلٹریشن سگنل کی تشخیص کو بڑھاتی ہے اور جھوٹے سگنلز کو کم کرتی ہے۔

-

رجحان کی پیروی کرنے والا نقصان روک کچھ منافع محفوظ کر سکتا ہے اور خطرے کو مؤثر طریقے سے کنٹرول کر سکتا ہے۔

-

مقررہ فی صد کے نقصان روک اور منافع بند کے نکات ایک ہی تجارت میں زیادہ سے زیادہ نقصان کو قابو کرتے ہیں اور خطرے کی حد سے تجاوز سے بچاتے ہیں۔

حکمت عملی کے خطرات

-

اتار چڑھاؤ والی مارکیٹ میں بار بار تجارت ہو سکتی ہے، جس سے پوزیشن کا سائز بڑھ سکتا ہے اور حکمت عملی کو نقصان پہنچ سکتا ہے۔

-

مقررہ نقصان روک کی حد بہت زیادہ مقرر کرنے سے غیر معمولی مارکیٹ کی حرکت میں بڑے نقصان کا سامنا کرنا پڑ سکتا ہے۔

-

ڈی ای ایم اے کراس سگنل میں تاخیر ہوتی ہے، جس کی وجہ سے تیز رفتار مارکیٹ میں خریداری قیمت کی چوٹی کے قریب ہو سکتی ہے، جس سے نقصان کا خطرہ بڑھ جاتا ہے۔

-

لائیو ٹریڈنگ میں سلپیج لاگت منافع پر اثر ڈال سکتی ہے، اس لیے نقصان روک اور منافع بند کے پیرامیٹرز کو ایڈجسٹ کرنے کی ضرورت ہے۔

حکمت عملی کی اصلاح

-

مارکیٹ کے حالات کے مطابق ڈی ای ایم اے پیرامیٹرز کو ایڈجسٹ کیا جا سکتا ہے تاکہ بہترین توازن پایا جا سکے۔

-

لائیو ٹریڈنگ میں سلپیج لاگت کو مدنظر رکھنا چاہیے اور مقررہ نقصان روک کی حد کو مناسب طور پر بڑھانا چاہیے۔

-

دیگر معاون تشخیصی اشارے، جیسے MACD، شامل کیے جا سکتے ہیں تاکہ سگنل کی تاثیر بڑھے۔

-

ٹریلنگ اسٹاپ کے لیے اسٹیپ ویلیو سیٹ کی جا سکتی ہے تاکہ نقصان روک کی منطق کو بہتر بنایا جا سکے۔

خلاصہ

یہ حکمت عملی ڈی ای ایم اے کی رجحان کی تشخیص کی صلاحیت کو استعمال کرتی ہے اور رجحان کی پیروی کرنے والے میکانزم کے ساتھ خطرے کو کنٹرول کرتی ہے، جو رجحان کا تعین کرنے والے تجارتی حکمت عملی کے نظام میں ایک بہت ہی عام نمائندہ ہے۔ مجموعی طور پر، اس حکمت عملی کے سگنل واضح ہیں، نقصان روک اور منافع بند کے نکات معقول ہیں، اور یہ ایک ایسی تجارتی حکمت عملی ہے جسے سمجھنا اور خطرے کے ساتھ کنٹرول کرنا آسان ہے۔ لائیو ٹریڈنگ میں سلپیج لاگت کی اصلاح اور معاون اشارے کی تشخیص کے ساتھ مل کر، اچھا سرمایہ کاری منافع حاصل کیا جا سکتا ہے۔

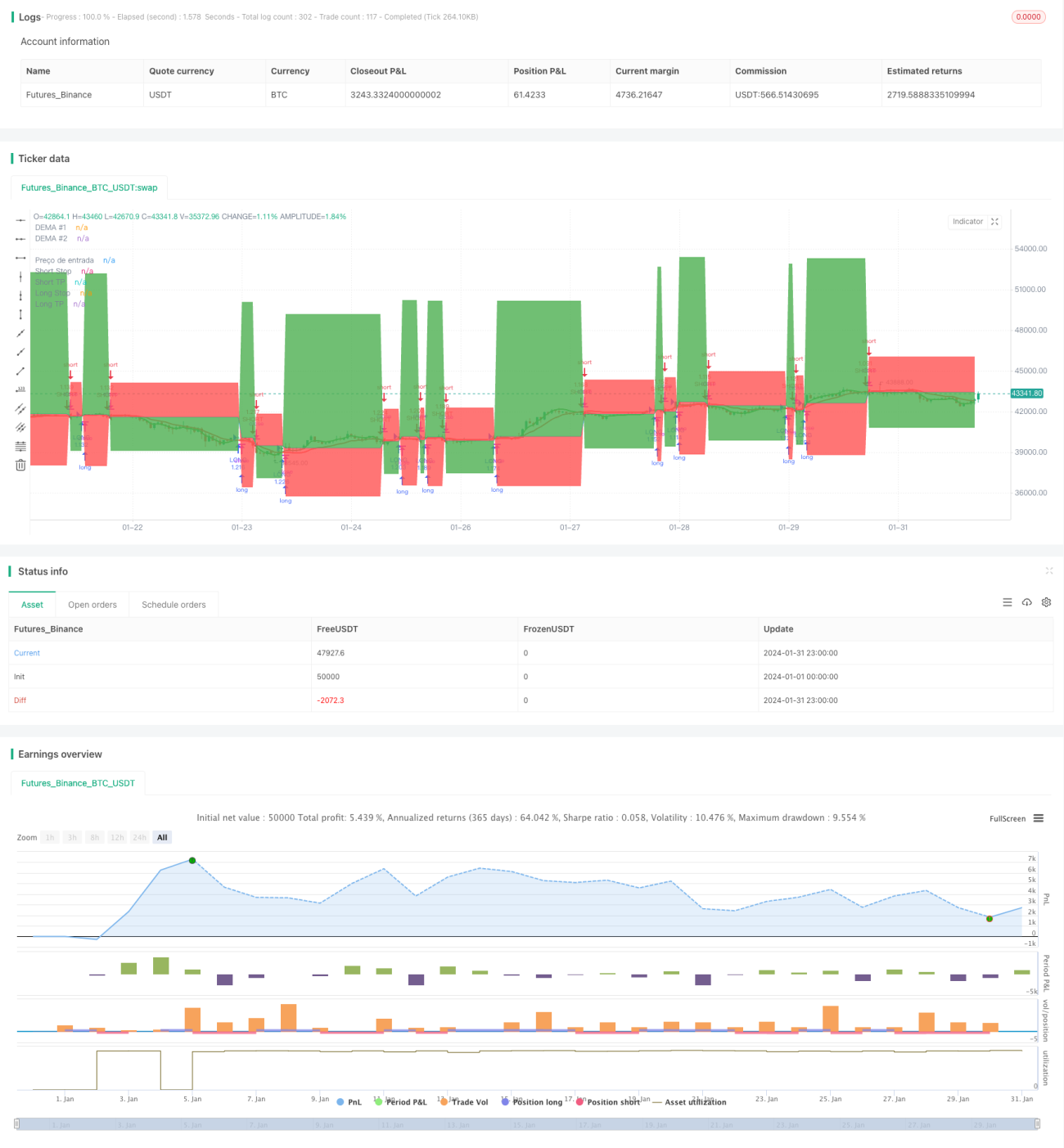

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1