تجارتی نفسیاتی توازن کنٹرول کی حکمت عملی

جائزہ

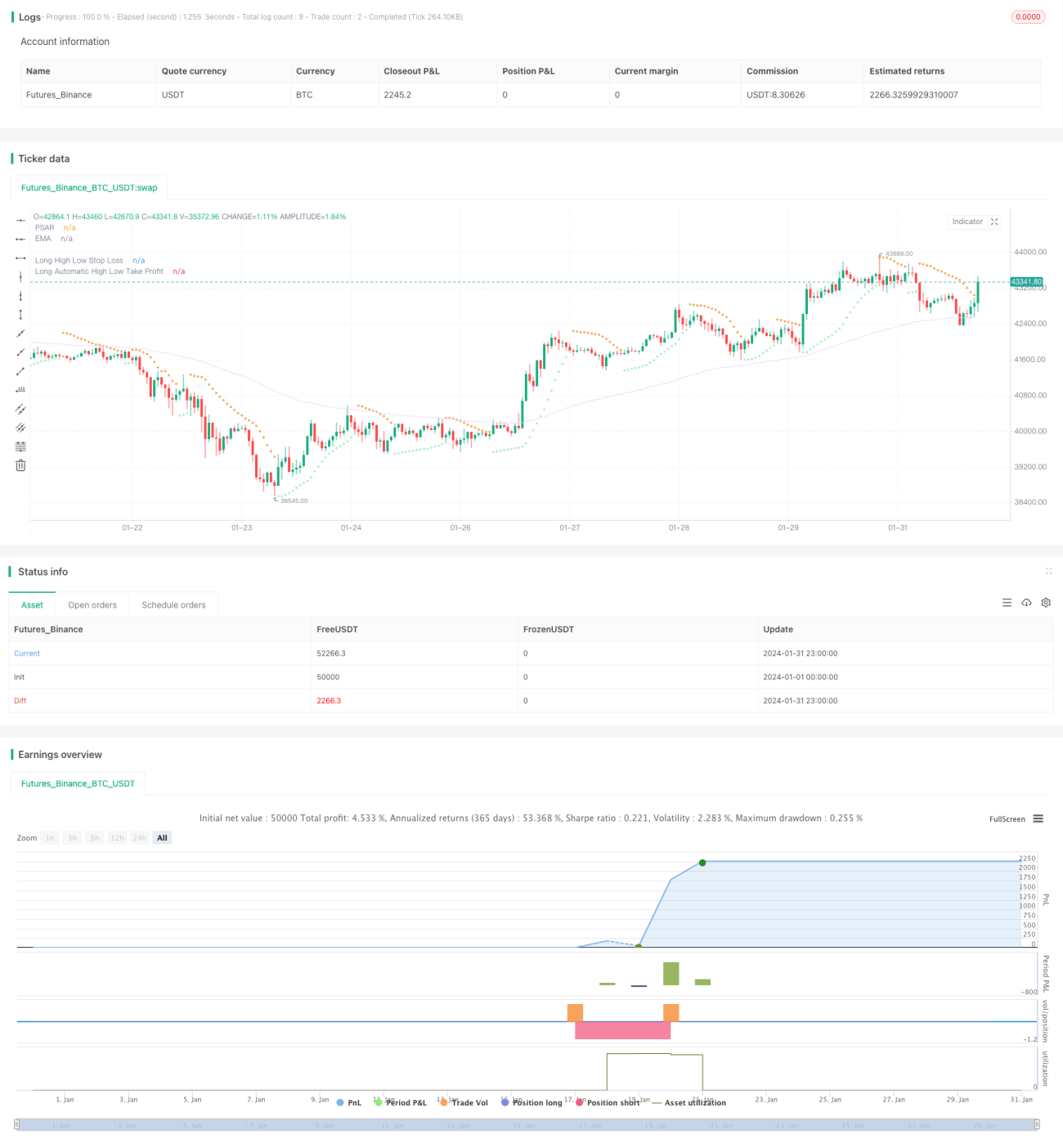

اس حکمت عملی کا مقصد مختلف پیرامیٹرز ترتیب دے کر تاجر کی نفسیات اور تجارتی کارکردگی میں توازن پیدا کرنا ہے تاکہ زیادہ مستحکم منافع حاصل کیا جا سکے۔ یہ مارکیٹ کے رجحان اور اتار چڑھاؤ کا اندازہ لگانے کے لیے موونگ ایوریج، بولنگر بینڈز، کیلٹنر چینل جیسے اشاریے استعمال کرتا ہے، پی ایس اے آر انڈیکیٹر کی مدد سے ریورسل سگنلز کی پہچان کرتا ہے، اور ٹی ٹی ایم اسکوائز انڈیکیٹر کے ذریعے مومینٹم کا جائزہ لیتا ہے۔ تجارتی سگنل ان اشاریوں کے امتزاج سے پیدا ہوتے ہیں۔ اس کے ساتھ ساتھ، حکمت عملی ہائی لو اسٹاپ لاس اور رسک ریوارڈ ریٹیو ٹیک پرافٹ کے طریقوں سے رسک کا انتظام کرتی ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی منطق درج ذیل ہے:

-

رجحان کا تعین: ای ایم اے موونگ ایوریج کے ذریعے قیمت کے رجحان کی سمت کا تعین کیا جاتا ہے۔ قیمت ای ایم اے کے اوپر ہو تو تیزی، نیچے ہو تو مندی کی علامت ہے۔

-

ریورسل کا تعین: پی ایس اے آر کے ذریعے قیمت کے ریورسل پوائنٹ کا تعین کیا جاتا ہے۔ پی ایس اے آر پوائنٹ کا قیمت کے اوپر ہونا تیزی کا سگنل، جبکہ نیچے ہونا مندی کا سگنل ہے۔

-

مومینٹم کا تعین: ٹی ٹی ایم اسکوائز انڈیکیٹر کے ذریعے مارکیٹ کے اتار چڑھاؤ اور مومینٹم کا جائزہ لیا جاتا ہے۔ یہ انڈیکیٹر بولنگر بینڈز اور کیلٹنر چینل کی چوڑائی کا موازنہ کر کے اتار چڑھاؤ کی پیمائش کرتا ہے، اسکوائز کا مطلب انتہائی کم اتار چڑھاؤ ہے۔ اسکوائز کا ختم ہونا اتار چڑھاؤ میں اضافے اور قیمت کی بڑی سمت میں حرکت کے امکان کی نشاندہی کرتا ہے۔

-

تجارتی سگنل کی تخلیق: جب قیمت ای ایم اے اور پی ایس اے آر پوائنٹ کو اوپر سے عبور کرے اور ٹی ٹی ایم اسکوائز انڈیکیٹر اسکوائز سے نکلے تو تیزی کا سگنل پیدا ہوتا ہے۔ جب قیمت ای ایم اے اور پی ایس اے آر پوائنٹ کو نیچے سے عبور کرے اور ٹی ٹی ایم اسکوائز انڈیکیٹر اسکوائز میں داخل ہو تو مندی کا سگنل پیدا ہوتا ہے۔

-

اسٹاپ لاس کا طریقہ: ہائی لو اسٹاپ لاس استعمال کیا جاتا ہے۔ حالیہ مخصوص مدت کی بلند ترین یا پست ترین قیمت کو مقررہ ایک سے ضرب دے کر اسٹاپ پوائنٹ طے کیا جاتا ہے۔

-

ٹیک پرافٹ کا طریقہ: رسک ریوارڈ ریٹیو کے ذریعے خودکار ٹیک پرافٹ لیا جاتا ہے۔ اسٹاپ پوائنٹ سے موجودہ قیمت کے فاصلے کے تناسب کو مقررہ رسک ریوارڈ ریٹیو پیرامیٹر سے ضرب دے کر ٹیک پرافٹ پوائنٹ حاصل کیا جاتا ہے۔

پیرامیٹرز کی ترتیب کے ذریعے تجارتی فریکوئنسی، پوزیشن مینجمنٹ، اسٹاپ لاس اور ٹیک پرافٹ پوائنٹس کو کنٹرول کیا جا سکتا ہے، جس سے تجارتی نفسیات میں توازن پیدا ہوتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

-

متعدد اشاریوں کا استعمال، جس سے سگنل کی درستگی میں اضافہ ہوتا ہے۔

-

ریورسل پر زور، رجحان کو معاون کی حیثیت سے استعمال کرتے ہوئے ریورسل پوائنٹس کو پکڑتا ہے اور تیزی میں فروخت اور مندی میں خرید کے امکان کو کم کرتا ہے۔

-

ٹی ٹی ایم اسکوائز انڈیکیٹر رجحان میں ایڈجسٹمنٹ کو مؤثر طریقے سے پہچانتا ہے، ایڈجسٹمنٹ کے دوران غیر مؤثر ٹریڈنگ سے بچاتا ہے۔

-

ہائی لو اسٹاپ لاس کا آسان اور عملی طریقہ، مارکیٹ کے مطابق اسٹاپ لاس کے فاصلے کو ایڈجسٹ کیا جا سکتا ہے۔

-

رسک ریوارڈ ریٹیو ٹیک پرافٹ کا طریقہ منافع اور نقصان کے تناسب کو عددی شکل میں پیش کرتا ہے، جس سے ایڈجسٹمنٹ آسان ہو جاتی ہے۔

-

مختلف پیرامیٹرز کی لچکدار ترتیب، ذاتی رسک برداشت کے مطابق عمدہ ایڈجسٹمنٹ کی اجازت دیتی ہے۔

رسک کا تجزیہ

اس حکمت عملی کے درج ذیل رسک بھی ہیں:

-

متعدد اشاریوں کا مشترکہ استعمال، اگرچہ سگنل کی درستگی بڑھاتا ہے، لیکن انٹری پوائنٹس کو چھوڑنے کے امکانات بھی بڑھ جاتے ہیں۔

-

ریورسل پر مبنی حکمت عملی، مضبوط رجحانی مارکیٹ میں شاید اچھی کارکردگی نہ دکھائے۔

-

ہائی لو اسٹاپ لاس بعض اوقات ٹوٹ سکتا ہے، رسک سے مکمل بچاؤ ممکن نہیں۔

-

رسک ریوارڈ ریٹیو ٹیک پرافٹ قیمت میں اچانک چھلانگ یا ایڈجسٹمنٹ کی وجہ سے بھی ناکام ہو سکتا ہے۔

-

پیرامیٹرز کی غلط ترتیب نقصان یا بار بار اسٹاپ لاس کا سبب بن سکتی ہے۔

بہتری کے ممکنہ پہلو

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

-

اشاریوں کے وزن میں اضافہ یا ایڈجسٹمنٹ تاکہ سگنل زیادہ درست ہوں۔

-

ریورسل اور رجحان کے تعین کے لیے اشاریوں کے پیرامیٹرز کو بہتر بنا کر منافع کے امکانات بڑھانا۔

-

ہائی لو اسٹاپ لاس کے پیرامیٹرز کو بہتر بنا کر اسٹاپ لاس کو مزید معقول بنانا۔

-

مختلف رسک ریوارڈ تناسبوں کا تجربہ کر کے بہترین نتائج حاصل کرنا۔

-

پوزیشن نمبر کے پیرامیٹرز میں ایڈجسٹمنٹ کر کے ایک ہی نقصان کے اثرات کو کم کرنا۔

خلاصہ

یہ حکمت عملی مجموعی طور پر اشاریوں کے مجموعے اور پیرامیٹر ایڈجسٹمنٹ کے ذریعے تجارتی نفسیات میں توازن پیدا کرنے اور مستحکم مثبت منافع حاصل کرنے میں مؤثر ہے۔ اگرچہ اس میں ابھی بہتری کی گنجائش موجود ہے، لیکن یہ عملی مارکیٹ میں استعمال کے لیے قابل قدر ہے۔ مارکیٹ فیڈ بیک اور پیرامیٹرز کی عمدہ ایڈجسٹمنٹ کے ذریعے یہ حکمت عملی تجارتی نفسیات پر قابو پانے اور طویل مدتی مستحکم منافع حاصل کرنے کا ایک مؤثر ذریعہ بن سکتی ہے۔

- 1