دوہری رجحان پیروی کی مقداری حکمت عملی

خلاصہ

اس حکمت عملی کا بنیادی خیال 123 ریورسل سٹریٹیجی اور رینبو آسیلیٹر انڈیکیٹر کو یکجا کرنا ہے تاکہ دوہری ٹرینڈ ٹریکنگ کی جا سکے، جس سے حکمت عملی کی جیت کی شرح میں اضافہ ہو۔ یہ حکمت عملی مختصر اور درمیانی مدت کے قیمت کے رجحانات کو ٹریک کرکے اور پوزیشن کو متحرک طور پر ایڈجسٹ کرکے مارکیٹ سے زیادہ ریٹرن حاصل کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی دو حصوں پر مشتمل ہے:

-

123 ریورسل سٹریٹیجی: اگر پچھلے دو دنوں کی بند قیمتوں میں کمی ہو اور آج کی بند قیمت میں اضافہ ہو، اور 9 دن کا Slow K 50 سے نیچے ہو، تو لمبی پوزیشن لی جائے گی۔ اگر پچھلے دو دنوں کی بند قیمتوں میں اضافہ ہو اور آج کی بند قیمت میں کمی ہو، اور 9 دن کا Fast K 50 سے اوپر ہو، تو چھوٹی پوزیشن لی جائے گی۔

-

رینبو آسیلیٹر انڈیکیٹر: یہ انڈیکیٹر متحرک اوسط کے نسبت قیمت کے انحراف کو ظاہر کرتا ہے۔ جب انڈیکیٹر 80 سے اوپر ہو تو مارکیٹ غیر مستحکم ہوتی ہے۔ جب انڈیکیٹر 20 سے نیچے ہو تو مارکیٹ میں تبدیلی کا امکان ہوتا ہے۔

یہ حکمت عملی دونوں کو یکجا کرتی ہے۔ جب لمبی اور چھوٹی دونوں سگنل ظاہر ہوں تو پوزیشن کھولی جائے گی، ورنہ پوزیشن بند کر دی جائے گی۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- دوہری فلٹریشن سگنل کے معیار کو بہتر بناتی ہے اور غلطی کی شرح کو کم کرتی ہے۔

- متحرک پوزیشن ایڈجسٹمنٹ یک طرفہ حرکت کے نقصان کو کم کرتی ہے۔

- مختصر اور درمیانی مدت کے انڈیکیٹرز کا انضمام حکمت عملی کے استحکام کو بڑھاتا ہے۔

خطرات کا تجزیہ

اس حکمت عملی میں درج ذیل خطرات بھی ہیں:

- پیرامیٹر کی غلط اصلاح اوور فٹنگ کا سبب بن سکتی ہے۔

- دوہری پوزیشن کھولنے سے ٹریڈنگ میں لاگت بڑھ جاتی ہے۔

- جب مارکیٹ میں شدید اتار چڑھاؤ ہو تو سٹاپ لاس آسانی سے ٹوٹ سکتا ہے۔

ان خطرات کو پیرامیٹرز کو ایڈجسٹ کرکے، پوزیشن مینجمنٹ کو بہتر بنا کر اور سٹاپ لاس کو مناسب طریقے سے سیٹ کرکے کم کیا جا سکتا ہے۔

بہتری کے امکانات

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- پیرامیٹرز کو بہتر بنانا اور بہترین کمبینیشن تلاش کرنا۔

- پوزیشن مینجمنٹ کا ماڈیول شامل کرنا تاکہ وولیٹیلیٹی اور ڈرا ڈاؤن کی بنیاد پر پوزیشن کو متحرک طور پر ایڈجسٹ کیا جا سکے۔

- سٹاپ لاس کا ماڈیول شامل کرنا اور متحرک سٹاپ لاس کو مناسب طریقے سے سیٹ کرنا۔

- مشین لرننگ الگورتھم شامل کرنا تاکہ رجحان کے موڑ کے مقامات کا تعین کرنے میں مدد ملے۔

نتیجہ

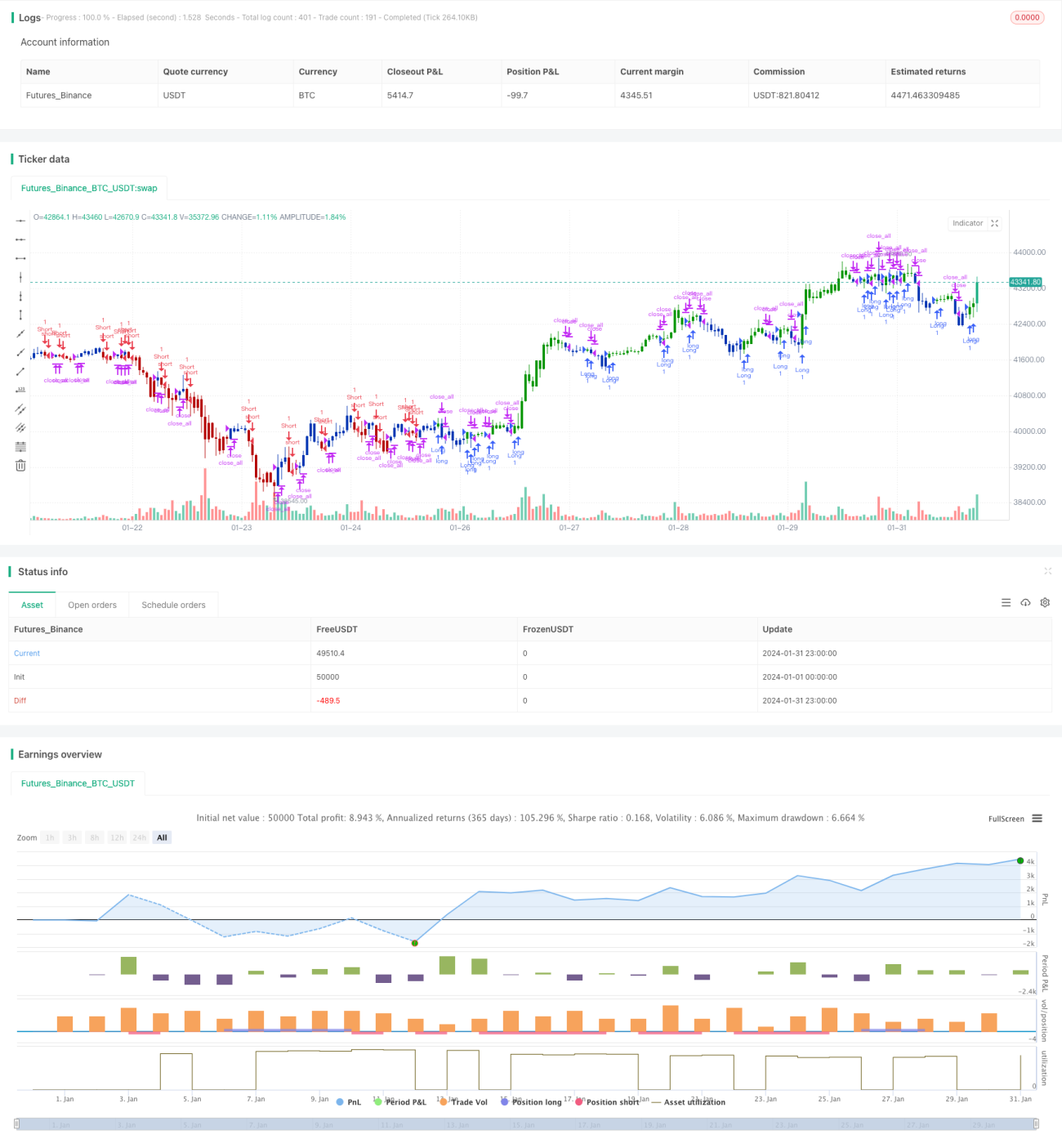

یہ حکمت عملی 123 ریورسل سٹریٹیجی اور رینبو آسیلیٹر انڈیکیٹر کو یکجا کرکے دوہری ٹرینڈ ٹریکنگ فراہم کرتی ہے، جو نسبتاً زیادہ استحکام کے ساتھ اضافی ریٹرن کی گنجائش رکھتی ہے۔ مسلسل بہتری کے ذریعے حکمت عملی کی منافع کی شرح میں مزید اضافہ کیا جا سکتا ہے۔

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/05/2021

// This is combo strategies for get a cumulative signal. - 1