سال کے اندر ایڈجسٹمنٹ پر مبنی RSI آسکیلیشن ٹریڈنگ حکمت عملی

1

Follow

1802

Followers

خلاصہ

یہ حکمت عملی ایک سال کے اندر ایڈجسٹ کردہ RSI اوسیلیٹنگ ٹریڈنگ حکمت عملی ہے جو RSI انڈیکیٹر کے اوپری اور نچلے بینڈز کے درمیان اوسیلیشن کی خصوصیات کو ٹریک کرتی ہے اور جب RSI انڈیکیٹر ان بینڈز کو چھوتا ہے تو ٹریڈنگ سگنل جاری کرتی ہے۔

حکمت عملی کا اصول

- MA اوسط کی لمبائی، RSI پیرامیٹرز، اوپری اور نچلے بینڈز، سٹاپ لاس اور ٹیک پروفیٹ پیرامیٹرز، اور ٹریڈنگ کی مدت کی حد مقرر کریں۔

- RSI انڈیکیٹر کی قیمت کا حساب لگائیں، RSI = (اوسط اضافہ) / (اوسط اضافہ + اوسط کمی) * 100

- RSI انڈیکیٹر اور اوپری/نچلے بینڈز کو ڈرائنگ کریں۔

- RSI انڈیکیٹر کا نچلے بینڈ کو اوپر کرنا لمبی پوزیشن کا سگنل ہے، اور اوپری بینڈ کو نیچے کرنا چھوٹی پوزیشن کا سگنل ہے۔

- پوزیشن کھولنے کے لیے OCO آرڈر سیٹ کریں۔

- مقرر کردہ سٹاپ لاس اور ٹیک پروفیٹ منطق کے مطابق سٹاپ لاس اور ٹیک پروفیٹ کریں۔

حکمت عملی کے فوائد کا تجزیہ

- سال کے اندر ٹریڈنگ کی مدت مقرر کرکے کچھ نامناسب بیرونی ماحول سے بچا جا سکتا ہے۔

- RSI انڈیکیٹر مؤثر طریقے سے زیادہ خریدی یا زیادہ فروخت کی صورتحال ظاہر کر سکتا ہے، اور مناسب حد میں اوسیلیشن ٹریڈنگ کرکے کچھ شور کو فلٹر کیا جا سکتا ہے۔

- OCO آرڈر کو سٹاپ لاس اور ٹیک پروفیٹ کے ساتھ ملا کر مؤثر خطرے کا کنٹرول حاصل کیا جا سکتا ہے۔

حکمت عملی کے خطرات کا تجزیہ

- RSI کی حد کے فیصلے کی درستگی کی ضمانت نہیں دی جا سکتی، غلط فیصلے کا خطرہ موجود ہے۔

- سال کے اندر ٹریڈنگ کی مدت کا غلط تعین بہتر مواقع سے محروم کر سکتا ہے یا نامناسب ٹریڈنگ ماحول میں داخل کر سکتا ہے۔

- سٹاپ لاس پوائنٹ بہت بڑا ہونے پر بڑا نقصان ہو سکتا ہے، اور ٹیک پروفیٹ پوائنٹ بہت چھوٹا ہونے پر منافع بہت کم ہو سکتا ہے۔

RSI پیرامیٹرز، ٹریڈنگ کی مدت کی حد، اور سٹاپ لاس/ٹیک پروفیٹ کے تناسب کو ایڈجسٹ کرکے اصلاح کی جا سکتی ہے۔

حکمت عملی کی اصلاح کی سمت

- مختلف مارکیٹوں اور مختلف ادوار میں RSI پیرامیٹرز کی بہترین قیمتوں کی جانچ کریں۔

- مجموعی مارکیٹ سائیکل کے نمونوں کا تجزیہ کرکے سال کے اندر بہترین ٹریڈنگ ٹائم سیٹ کریں۔

- بیک ٹیسٹنگ کے ذریعے مناسب سٹاپ لاس اور ٹیک پروفیٹ تناسب کا تعین کریں۔

- ٹریڈنگ کے لیے مصنوعات کے انتخاب کو بہتر بنائیں اور پوزیشن کے سائز میں اضافہ کریں۔

- دیگر بہتر ٹریڈنگ تکنیکوں یا انڈیکیٹرز کے ساتھ ملا کر اصلاح کریں۔

خلاصہ

یہ حکمت عملی RSI انڈیکیٹر کے سال کے اندر مخصوص مدت میں اوسیلیشن کی خصوصیات کا استعمال کرتے ہوئے ٹرینڈ فالوونگ ٹریڈنگ کرتی ہے، جس سے ٹریڈنگ کے خطرات کو مؤثر طریقے سے کنٹرول کیا جاتا ہے۔ پیرامیٹر اور قواعد کی اصلاح کے ذریعے بہتر حکمت عملی کے نتائج حاصل کیے جا سکتے ہیں۔

Source

Pine

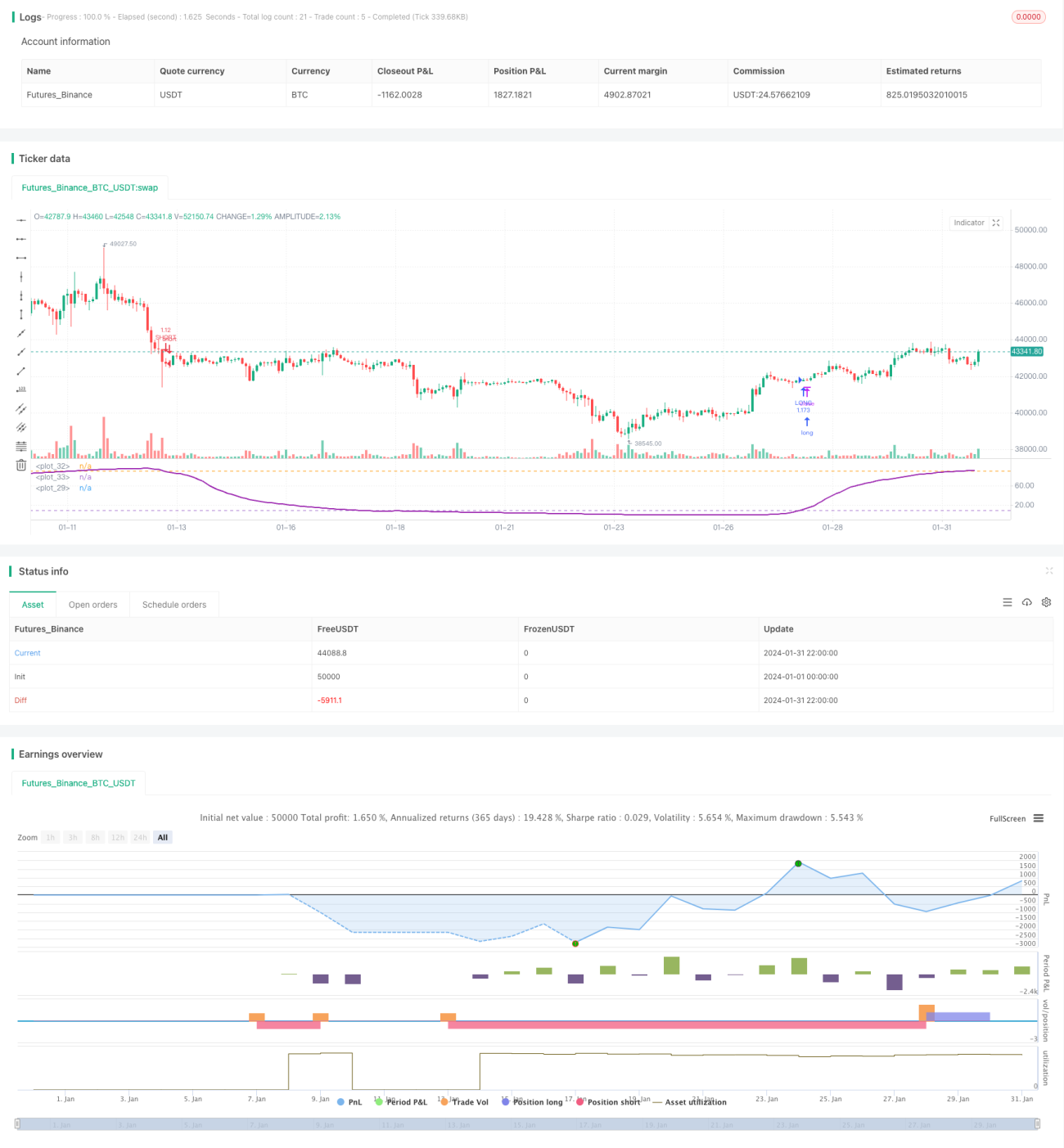

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title = "Bitlinc MARSI Study AST",shorttitle="Bitlinc MARSI Study AST",default_qty_type = strategy.percent_of_equity, default_qty_value = 100,commission_type=strategy.commission.percent,commission_value=0.1,initial_capital=1000,currency="USD",pyramiding=0, calc_on_order_fills=false)

// === General Inputs ===Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1