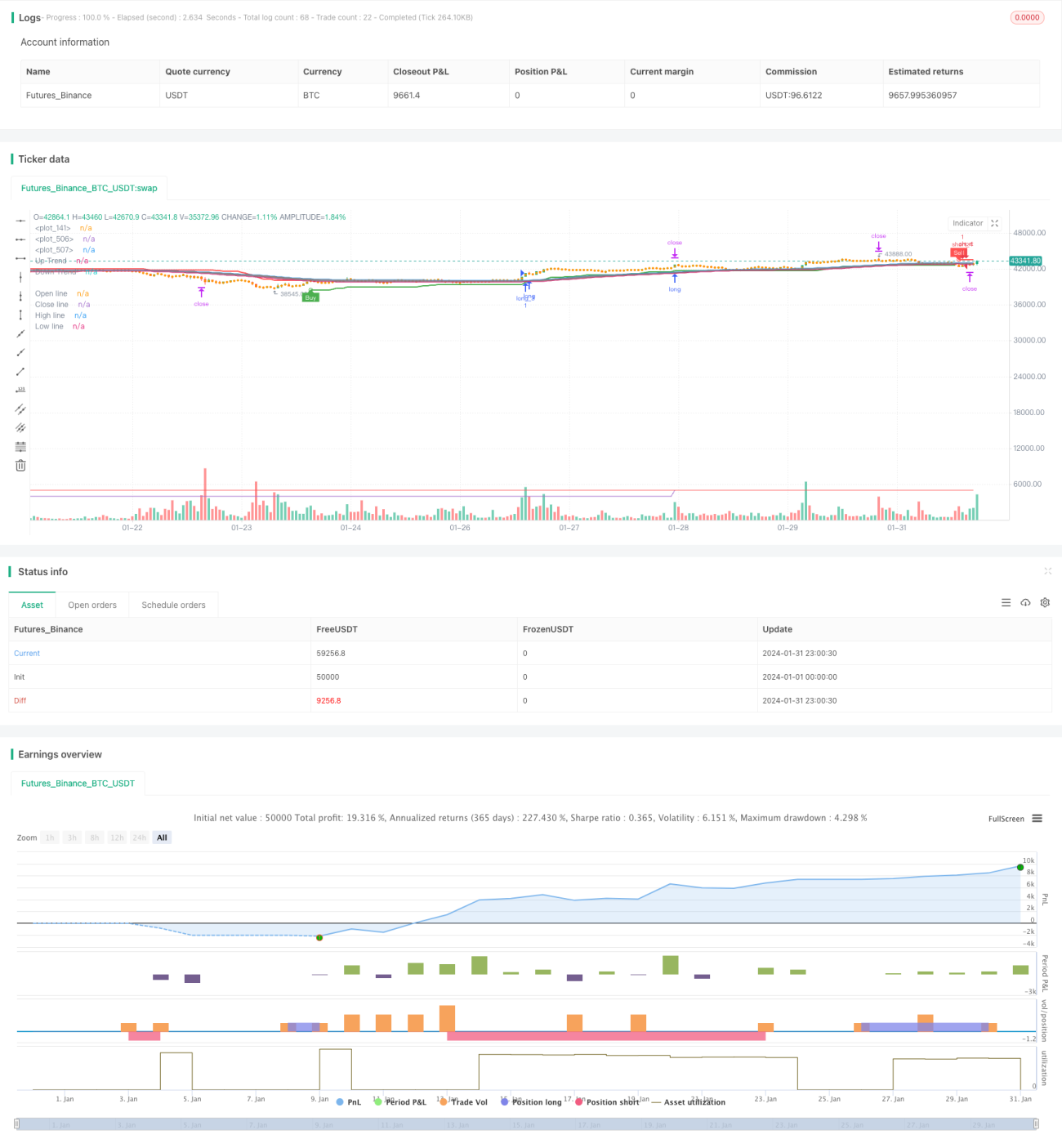

تین گنا تصدیقی رجحان کی پیروی کی حکمت عملی

جائزہ

تین گنا تصدیق شدہ رجحان کی پیروی کی حکمت عملی، موونگ ایوریج، یادداشت کی لکیر اور سپر ٹرینڈ جیسے تین بڑے انڈیکیٹرز کے سگنلز کو ملا کر، رجحان کی اعلیٰ امکانی گرفت کرتی ہے۔ جب تینوں انڈیکیٹرز بیک وقت خرید یا فروخت کا سگنل دیتے ہیں تو حکمت عملی بروقت اندراج کرتی ہے اور رجحان کی پیروی کرتی ہے۔ جب رجحان الٹ جاتا ہے تو حکمت عملی فوری طور پر نقصان روک کر مخالف سمت میں کام کرتی ہے۔

حکمت عملی کے اصول

اوسط لائن کے ذریعے اہم رجحان کا تعین

حکمت عملی 52 ادوار کی لمبائی والی اوسط لائن کا استعمال کرتے ہوئے اہم رجحان کی سمت کا تعین کرتی ہے۔ جب قیمت اوسط لائن کو اوپر سے عبور کرتی ہے تو اسے صعودی رجحان سمجھا جاتا ہے؛ جب قیمت اوسط لائن کو نیچے سے عبور کرتی ہے تو اسے نزولی رجحان سمجھا جاتا ہے۔

یادداشت کی لکیر کے ذریعے ثانوی الٹ پلٹ کی شناخت

حکمت عملی قلیل مدتی ثانوی الٹ پلٹ کی شناخت کے لیے یادداشت کی لکیر بھی استعمال کرتی ہے۔ یادداشت کی لکیر کا حساب کتاب اوسط لائن کی طرح ہے، لیکن بند قیمت کے بجائے افتتاحی قیمت استعمال کی جاتی ہے، جس سے قیمت کے الٹ پلٹ کی معلومات زیادہ تیزی سے ظاہر ہوتی ہیں۔ جب قیمت نیچے جا رہی یادداشت کی لکیر کو اوپر سے عبور کرتی ہے تو یہ قیمت کے قلیل مدتی استحکام اور بحالی کا اشارہ ہوتا ہے؛ جب قیمت اوپر جا رہی یادداشت کی لکیر کو نیچے سے عبور کرتی ہے تو یہ قیمت میں قلیل مدتی کمی کا اشارہ ہوتا ہے۔

سپر ٹرینڈ کے ذریعے الٹ پلٹ کے مقامات کا تعین

حکمت عملی اہم الٹ پلٹ کے مقامات کا تعین کرنے کے لیے سپر ٹرینڈ انڈیکیٹر بھی شامل کرتی ہے۔ سپر ٹرینڈ انڈیکیٹر ATR کے ونڈو پیریڈ اور قیمت کے ڈیٹا کو ملا کر متحرک طور پر چینل کی اوپری اور نچلی حدود کو ایڈجسٹ کرتا ہے، اس طرح الٹ پلٹ کے وقت کا تعین کرتا ہے۔

تین گنا تصدیق شدہ سگنل فلٹرنگ

جب اوسط لائن، یادداشت کی لکیر اور سپر ٹرینڈ تینوں انڈیکیٹرز بیک وقت خرید کا سگنل دیتے ہیں تو حکمت عملی صرف اس وقت طویل پوزیشن لیتی ہے؛ جب تینوں بیک وقت فروخت کا سگنل دیتے ہیں تو حکمت عملی صرف اس وقت مختصر پوزیشن لیتی ہے۔ تین انڈیکیٹرز کی تصدیق سے جھوٹے سگنلز کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے اور اندراج کے امکانات کو بہتر بنایا جا سکتا ہے۔

فوائد کا تجزیہ

کثیر جہتی فیصلہ، اعلیٰ امکانات

حکمت عملی تین انڈیکیٹرز (اوسط لائن، یادداشت کی لکیر اور سپر ٹرینڈ) کو ملا کر مختلف جہتوں سے رجحان اور اہم نکات کا تعین کرتی ہے، جس سے اعلیٰ امکانات پر اندراج یقینی ہوتا ہے۔

تیز رد عمل، حقیقی وقت میں پیروی

یادداشت کی لکیر کا استعمال اس بات کو یقینی بناتا ہے کہ حکمت عملی قیمت کی قلیل مدتی تبدیلیوں پر تیزی سے رد عمل ظاہر کر سکے؛ جبکہ ATR کے خود انطباقی چینل والا سپر ٹرینڈ انڈیکیٹر بھی قیمت کی تبدیلیوں کو حقیقی وقت میں ٹریک کر سکتا ہے۔

خودکار منافع بندی اور نقصان روکنے، مؤثر خطرے کا انتظام

حکمت عملی میں خودکار منافع بندی اور نقصان روکنے کی منطق شامل ہے، جو ATR کی بنیاد پر متحرک طور پر منافع بندی اور نقصان روکنے کے مقامات کو ایڈجسٹ کر سکتی ہے اور ایک ہی تجارت میں ہونے والے نقصان کو مؤثر طریقے سے کنٹرول کر سکتی ہے۔

خطرات اور حل

زیادہ تجارتی تعدد کا خطرہ

حکمت عملی کے سگنلز کثرت سے آتے ہیں جس کی وجہ سے زیادہ تجارت ہو سکتی ہے۔ اوسط لائن کے پیریڈ پیرامیٹر کو مناسب طور پر بڑھا کر تجارتی تعدد کو کم کیا جا سکتا ہے۔

الٹ پلٹ کی غیر یقینی صورتحال کا خطرہ

یادداشت کی لکیر اور سپر ٹرینڈ انڈیکیٹرز کے ذریعے الٹ پلٹ کے مقامات کا تعین غیر یقینی ہو سکتا ہے، جس سے غلط تشخیص کا خطرہ ہو سکتا ہے۔ انڈیکیٹر پیرامیٹرز میں فلٹرنگ کی شرائط شامل کی جا سکتی ہیں تاکہ زیادہ امکانی الٹ پلٹ سگنلز کو یقینی بنایا جا سکے۔

اتار چڑھاؤ والی مارکیٹ میں نقصان کا خطرہ

اتار چڑھاؤ والی مارکیٹ میں بار بار کراس اوور کی وجہ سے حکمت عملی بار بار پوزیشن کھولے گی اور پھر نقصان روکے گی، جس سے نقصان کا خطرہ ہوتا ہے۔ اتار چڑھاؤ والی مارکیٹ کی پہچان کر کے اس مرحلے کے دوران حکمت عملی کو روکا جا سکتا ہے۔

بہتری کے مواقع

اتار چڑھاؤ انڈیکیٹرز کا استعمال

اتار چڑھاؤ والے انڈیکیٹرز جیسے بولنگر بینڈ کو شامل کرنے پر غور کیا جا سکتا ہے۔ جب قیمت بولنگر بینڈ کی اوپری یا نچلی حد کے قریب ہو تو نئی پوزیشن کھولنے سے گریز کیا جا سکتا ہے، اس طرح اتار چڑھاؤ والی مارکیٹ کے خطرے سے بچا جا سکتا ہے۔

اندراج کے فلٹرز میں اضافہ

دوسرے معاون انڈیکیٹرز جیسے KDJ، MACD وغیرہ کو شامل کرنے کی کوشش کی جا سکتی ہے، اور جب وہ بھی بیک وقت سگنل دیں تو اندراج کیا جائے۔ اس سے جھوٹے سگنلز کو مزید فلٹر کیا جا سکتا ہے اور غیر ضروری تجارت کو کم کیا جا سکتا ہے۔

منافع بندی اور نقصان روکنے کی حکمت عملی کو بہتر بنانا

منافع بندی اور نقصان روکنے کی حکمت عملی کو بہتر بنایا جا سکتا ہے، جیسے کہ متحرک منافع بندی، ایکسپونینشل متحرک منافع بندی، آدھی پوزیشن کے وقفے والی منافع بندی وغیرہ، تاکہ منافع زیادہ اور مستحکم ہو سکے۔

خلاصہ

تین گنا تصدیق شدہ رجحان کی پیروی کی حکمت عملی اوسط لائن، یادداشت کی لکیر اور سپر ٹرینڈ جیسے تین بڑے انڈیکیٹرز کے فوائد کو بروئے کار لا کر رجحان کی اعلیٰ امکانی شناخت اور گرفت کرتی ہے۔ ساتھ ہی خودکار منافع بندی اور نقصان روکنے کا طریقہ کار ایک ہی تجارت کے نقصان کو مؤثر طریقے سے کنٹرول کرتا ہے۔ مزید بہتری کے لیے، دیگر معاون انڈیکیٹرز کو شامل کر کے اندراج کو فلٹر کیا جا سکتا ہے، اور منافع بندی اور نقصان روکنے کی حکمت عملی کو بہتر بنایا جا سکتا ہے تاکہ حکمت عملی زیادہ عملی ہو۔

- 1