دو طرفہ ٹریکنگ سٹاپ لاس مووینگ ایوریج ٹرینڈ سٹریٹیجی

جائزہ

یہ حکمت عملی Super Trend، SSL Hybrid Baseline Channel اور QQE Momentum indicators کو ملا کر دو طرفہ پوزیشنوں کے لیے trailing stop loss کا استعمال کرتی ہے تاکہ درمیانی اور طویل مدتی رجحان کو پکڑا جا سکے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر درج ذیل نکات پر مبنی ہے:

- Super Trend indicator کے ذریعے مجموعی رجحان کی سمت کا تعین کیا جاتا ہے، جو داخلے کے وقت کا تعین کرنے میں مدد دیتا ہے۔

- SSL Hybrid Baseline Channel کی بنیاد پر داخلے کے مخصوص مقامات کا تعین کیا جاتا ہے۔ چینل کا ٹوٹنا بنیادی داخلے کا سگنل ہوتا ہے۔

- QQE indicator کے bullish/bearish crossover کو داخلے کے لیے ثانوی تصدیقی سگنل کے طور پر استعمال کیا جاتا ہے۔

- ATR indicator کی مدد سے stop loss اور take profit کی سطحوں کا حساب لگایا جاتا ہے۔

- فیصد رسک مینجمنٹ اور متحرک stop loss ایڈجسٹمنٹ کا استعمال کرتے ہوئے ہر ٹریڈ کے خطرے کو کنٹرول کیا جاتا ہے۔

داخلے کا منطق یہ ہے کہ جب Super Trend پلٹے اور قیمت Baseline Channel کو توڑے، اور ساتھ ہی QQE indicator اسی سمت میں crossover کرے، تب ہی داخلہ ممکن ہے۔

indicators کا یہ مجموعہ داخلے کے وقت کو مؤثر طریقے سے کنٹرول کرتا ہے اور اتار چڑھاؤ والی مارکیٹ میں بے کار ٹریڈز سے بچاتا ہے۔

باہر نکلنے کا منطق نسبتاً آسان ہے: Super Trend کے پلٹنے کو exit سگنل کے طور پر استعمال کیا جاتا ہے، یا پھر stop loss / take profit ٹرگر ہونے پر باہر نکل جاتے ہیں۔

فوائد کا تجزیہ

اس حکمت عملی کا سب سے بڑا فائدہ یہ ہے کہ متعدد indicators کے مشترکہ استعمال سے جھوٹے بریک آؤٹ کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے، جس سے بے کار ٹریڈز کا امکان کم ہو جاتا ہے۔

اس کے علاوہ، فیصدی stop loss کے ذریعے ہر ٹریڈ کے نقصان کو محدود کرنا اس حکمت عملی کا ایک اہم پہلو ہے۔

ATR کے ذریعے stop loss کی سطح کا حساب لگا کر، اور پھر کنفیگر ایبل stop loss multiplier کے ساتھ، ہم ہر ٹریڈ کے خطرے کو واضح طور پر جان سکتے ہیں۔ یہ رسک مینجمنٹ کے لیے بہت اہم ہے۔

ہم مجموعی نقصان کو محدود کرنے کے لیے زیادہ سے زیادہ قابل برداشت نقصان کا فیصد بھی مقرر کر سکتے ہیں۔

یہ حکمت عملی منافع کو محفوظ بنانے کے لیے trailing stop loss کا بھی استعمال کرتی ہے، جو منافع بڑھانے کے لیے کلیدی حیثیت رکھتا ہے۔

خطرات کا تجزیہ

اس حکمت عملی کا سب سے بڑا خطرہ یہ ہے کہ مشترکہ سگنل غلط ہونے کا امکان ہے۔ اگرچہ ہم نے متعدد indicators کا فلٹر استعمال کیا ہے، لیکن کوئی بھی indicator مکمل طور پر غلطی سے پاک نہیں ہوتا۔

جب Super Trend جھوٹا بریک آؤٹ دکھائے یا QQE غلط سگنل بنائے، تو یہ حکمت عملی آسانی سے ٹریڈ میں داخل ہو جاتی ہے، جس سے stop loss ہونے کا خطرہ بڑھ جاتا ہے۔

اس کے علاوہ، یہ حکمت عملی overfitting کے خطرے سے بھی دوچار ہے۔ پیرامیٹرز کو احتیاط سے سیٹ کرنے کی ضرورت ہے، تاریخی ڈیٹا پر زیادہ انحصار کرنے سے گریز کرنا چاہیے۔

ہمیں اہم پیرامیٹرز جیسے ATR length، stop loss multiplier، percentage risk وغیرہ کی سیٹنگز پر توجہ دینی ہوگی۔ ان پیرامیٹرز کو مختلف مصنوعات کے مطابق انفرادی طور پر ایڈجسٹ کرنے کی ضرورت ہے۔

بہتری کے امکانات

اس حکمت عملی میں مزید بہتری کی گنجائش موجود ہے:

- مزید indicators کے امتزاج کو جانچا جا سکتا ہے، مثلاً KD indicator کو بطور معاون شامل کرنا۔

- مختلف پیرامیٹر سیٹنگز کے تحت استحکام کو آزمایا جا سکتا ہے۔

- مشین لرننگ پر مبنی طریقوں سے پیرامیٹرز کو خودکار طور پر بہتر بنانے کی کوشش کی جا سکتی ہے۔

- ایک خودکار stop loss میکانزم متعارف کرایا جا سکتا ہے جو مارکیٹ کے اتار چڑھاؤ کے مطابق stop loss کی حد کو ایڈجسٹ کرے۔

- دوبارہ داخلے کا منطق شامل کیا جا سکتا ہے تاکہ stop loss کے بعد دوبارہ ٹریڈ میں داخل ہو کر مواقع سے محروم نہ ہونا پڑے۔

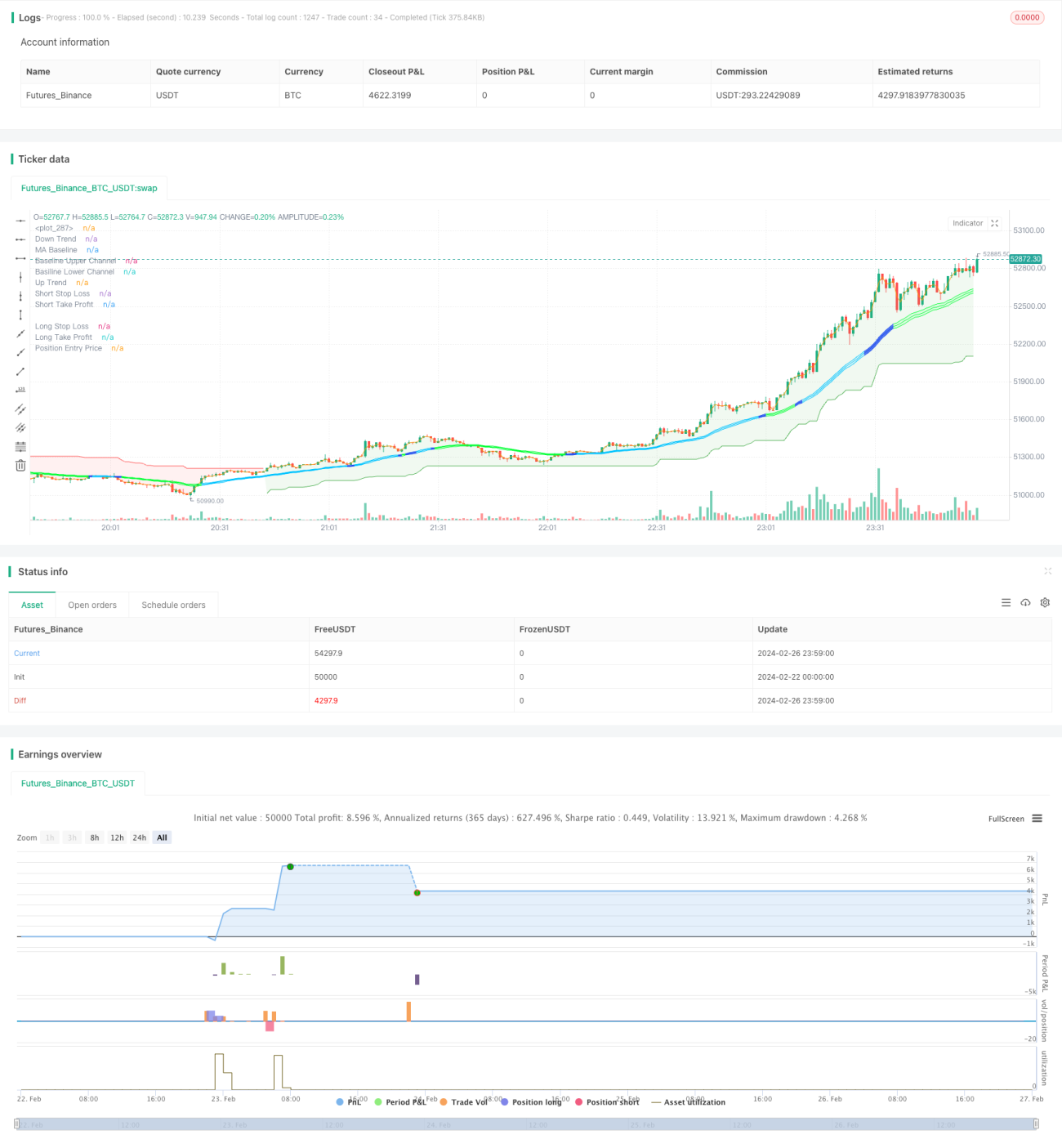

/*backtest

start: 2024-02-22 00:00:00

end: 2024-02-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to W3MCT - @simonFUTURE2 w3mct.com -

// @version=5- 1