جائزہ

یہ حکمت عملی ایک مختصر فاریکس ٹریڈنگ حکمت عملی ہے ، جس کا بنیادی خیال یہ ہے کہ پوزیشن کے سائز کو متحرک طور پر ایڈجسٹ کرکے رسک مینجمنٹ کو بڑھانا ہے۔ حکمت عملی ، موجودہ اکاؤنٹ کے حقوق و منافع اور ہر تجارت کے خطرے کے تناسب کے مطابق ، متحرک پوزیشن کے سائز کا حساب لگاتا ہے۔ اس کے علاوہ ، حکمت عملی میں سخت اسٹاپ اور اسٹاپ کی شرائط طے کی گئیں ، قیمت میں منفی تبدیلی کی صورت میں تیزی سے پوزیشن کو صاف کرنا ، خطرہ پر قابو پانا۔ جب قیمت میں فائدہ مند سمت میں تبدیلی آتی ہے تو ، منافع کو بروقت لاک کرنا۔

حکمت عملی کا اصول

- صارف کے ذریعہ درج کردہ پیرامیٹرز جیسے شارٹ لائن پوزیشن رکھنے والے دنوں کی تعداد ، قیمت میں کمی کی فیصد ، ہر تجارت کے خطرے کا تناسب ، اسٹاپ نقصان کی فیصد اور اسٹاپ اسٹاپ فیصد کے مطابق متعلقہ متغیرات کو شروع کریں۔

- جب کوئی پوزیشن نہیں ہوتی ہے تو ، متحرک پوزیشن کا سائز موجودہ اکاؤنٹ میں دلچسپی اور ہر تجارت کے خطرے کے تناسب کے مطابق حساب کیا جاتا ہے ، اور اس کے بعد مارکیٹ کی قیمت پر خالی سر کھول دیا جاتا ہے۔

- پوزیشن کھولنے کی قیمت اور پوزیشن کے متوقع وقت کو ریکارڈ کریں۔

- پوزیشن رکھنے کے دوران ، قیمت کی تبدیلیوں کی اصل وقت میں نگرانی کریں۔ اگر اسٹاپ نقصان کی قیمت ، اسٹاپ اسٹاپ قیمت یا پوزیشن رکھنے کے لئے مقررہ وقت تک پہنچ جاتا ہے تو ، خالی سر کی پوزیشن کو صاف کریں۔

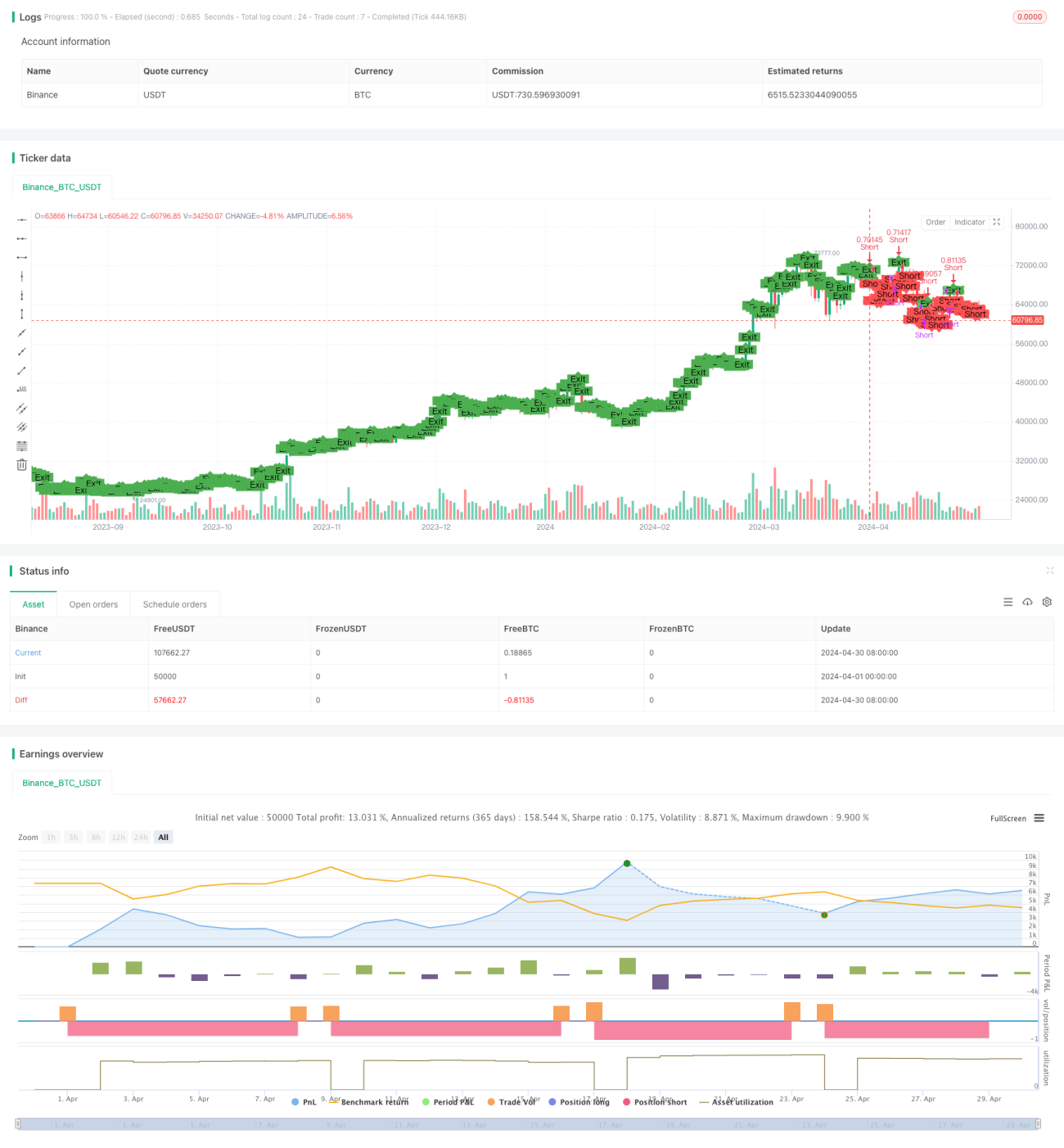

- چارٹ پر کھلے پوزیشن اور پوزیشن پوائنٹس کو نشان زد کریں ، تاکہ تجارت کی صورتحال کو بصری طور پر دکھایا جاسکے۔

طاقت کا تجزیہ

- متحرک پوزیشن کا سائز: اکاؤنٹ کے حقوق اور مفادات اور خطرے کے تناسب کے مطابق ہر تجارت کے لئے پوزیشن کا سائز متحرک طور پر ایڈجسٹ کریں ، خطرے پر قابو پانے کے ساتھ ساتھ فنڈز کے استعمال کی کارکردگی کو بہتر بنائیں۔

- سخت اسٹاپ نقصان کی حد: ایک ہی تجارت کے خطرے کی حد کو مؤثر طریقے سے کنٹرول کرنے کے لئے ایک تنگ اسٹاپ نقصان اور اسٹاپ نقصان کی حد مقرر کریں ، اور منافع کو بروقت لاک کریں۔

- شارٹ لائن ٹریڈنگ: اسٹریٹجی میں شارٹ لائن ٹریڈنگ کے مواقع پر توجہ دی جاتی ہے ، جس میں کم وقت کی پوزیشن ہوتی ہے ، جو مختصر مدت میں قیمتوں میں اتار چڑھاو کو پکڑنے کے لئے مارکیٹ میں ہونے والی تبدیلیوں کو تیزی سے ڈھال سکتی ہے۔

- سادہ اور استعمال میں آسان: حکمت عملی کی منطق واضح ہے ، پیرامیٹرز کی ترتیب آسان ہے ، جو ابتدائی سیکھنے اور استعمال کے لئے موزوں ہے۔

خطرے کا تجزیہ

- مارکیٹ کا خطرہ: غیر ملکی کرنسی کی مارکیٹ میں تیزی سے تبدیلی ، قلیل مدتی قیمتوں میں شدید اتار چڑھاؤ ، جس کی وجہ سے حکمت عملی اکثر اسٹاپ نقصان کا سبب بن سکتی ہے۔

- پیرامیٹرز کی ترتیب کا خطرہ: غیر مناسب پیرامیٹرز کی ترتیب ، جیسے کہ خطرہ کا تناسب بہت زیادہ ہے ، روک تھام کی جگہ بہت تنگ ہے ، اور اسی طرح ، اکاؤنٹ کو تیزی سے پھنس جانے کا سبب بن سکتا ہے۔

- پوزیشن سائز کا خطرہ: اگرچہ حکمت عملی متحرک پوزیشن سائز کا استعمال کرتی ہے ، لیکن ہر تجارت میں خطرہ کا تناسب احتیاط سے طے کیا جانا چاہئے تاکہ کسی ایک تجارت میں زیادہ رقم خرچ نہ ہو۔

اصلاح کی سمت

- مزید تکنیکی اشارے متعارف کروائیں ، جیسے چلتی اوسط ، MACD ، وغیرہ ، جو رجحانات کا تعین کرنے اور پوزیشن کھولنے کے وقت میں معاون ہیں۔

- اسٹریٹجک منافع کے خطرے کے تناسب کو بہتر بنانے کے لئے اسٹاپ نقصانات کو روکنے کے منطق کو بہتر بنائیں ، جیسے ٹریکنگ اسٹاپ ، جزوی اسٹاپ وغیرہ۔

- مختلف کرنسی کے جوڑوں اور مارکیٹ کے حالات کے لئے مختلف پیرامیٹرز کا مجموعہ ترتیب دیں ، حکمت عملی کی موافقت اور استحکام کو بہتر بنائیں۔

- پوزیشن مینجمنٹ منطق میں شامل کریں ، جیسے کیلی فارمولہ جیسے طریقوں کا استعمال کرتے ہوئے ، ہر تجارت کے لئے خطرے کے تناسب کو متحرک طور پر ایڈجسٹ کریں۔

خلاصہ کریں۔

یہ حکمت عملی متحرک پوزیشن اسکیل اور سخت اسٹاپ نقصان کی روک تھام کے ذریعے ، مختصر لائن ٹریڈنگ میں خطرے پر قابو پانے اور منافع کے حصول کا توازن حاصل کرتی ہے۔ حکمت عملی کی منطق آسان اور واضح ہے ، جو ابتدائی سیکھنے کے لئے موزوں ہے۔ تاہم ، عملی طور پر لاگو ہونے پر احتیاط کی ضرورت ہے ، خطرے پر قابو پانے پر توجہ دیں ، اور مارکیٹ میں تبدیلی کے مطابق حکمت عملی کو بہتر بنائیں اور بہتر بنائیں۔ مزید تکنیکی اشارے متعارف کرانے ، اسٹاپ نقصان کی روک تھام کی منطق کو بہتر بنانے ، مختلف مارکیٹ کی صورتحال کے لئے پیرامیٹرز ترتیب دینے ، پوزیشن مینجمنٹ میں شامل ہونے ، وغیرہ کے ذریعہ حکمت عملی کی استحکام اور منافع بخش صلاحیت کو مزید بہتر بنایا جاسکتا ہے۔

- 1