Williams %R کی بنیاد پر منافع اور نقصان کو روکنے کے لئے متحرک ایڈجسٹمنٹ کی حکمت عملی

جائزہ

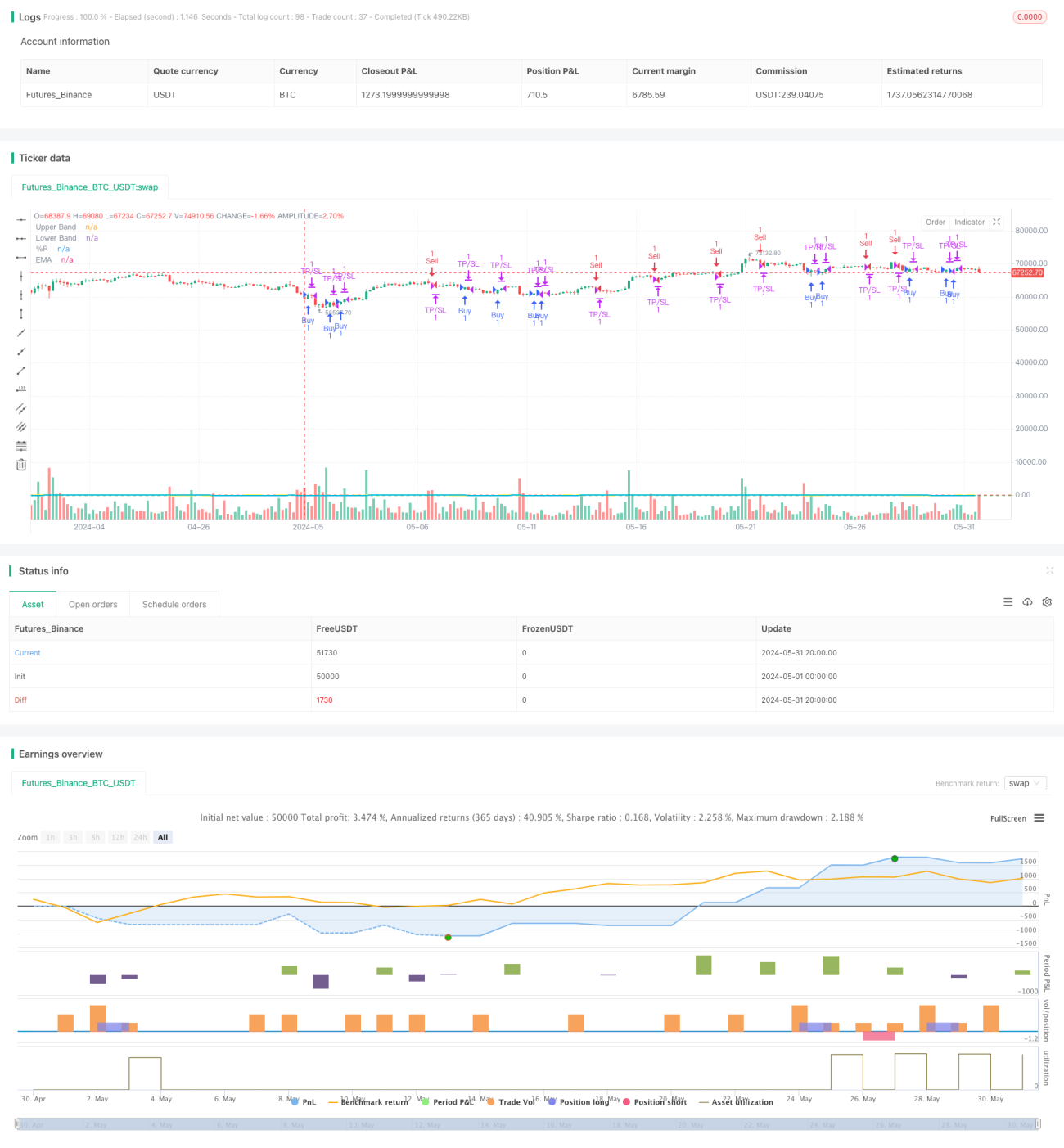

یہ حکمت عملی Williams %R انڈیکیٹر پر مبنی ہے، اور منافع روکنے (Take Profit) اور نقصان روکنے (Stop Loss) کی سطحوں کو متحرک طور پر ایڈجسٹ کرکے تجارتی کارکردگی کو بہتر بناتی ہے۔ جب Williams %R اوور سیلڈ زون (-80) کو عبور کرتا ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب اوور باؤٹ زون (-20) کو عبور کرتا ہے تو فروخت کا سگنل پیدا ہوتا ہے۔ اسی کے ساتھ، Williams %R کی قدروں کو ہموار کرنے اور شور کو کم کرنے کے لیے ایکسپونینشل موونگ ایوریج (EMA) استعمال کیا جاتا ہے۔ یہ حکمت عملی مختلف مارکیٹ حالات اور تاجروں کی ترجیحات کے مطابق ڈھلنے کے لیے لچکدار پیرامیٹر سیٹنگز فراہم کرتی ہے، بشمول انڈیکیٹر پیریڈ، منافع روکنے/نقصان روکنے (TP/SL) کی سطحیں، تجارتی اوقات اور تجارتی سمت کا انتخاب۔

حکمت عملی کا اصول

- مخصوص پیریڈ کے لیے Williams %R انڈیکیٹر کی قدر کا حساب لگایا جاتا ہے۔

- Williams %R کی ایکسپونینشل موونگ ایوریج (EMA) کا حساب لگایا جاتا ہے۔

- جب Williams %R نیچے سے اوپر جا کر -80 کی سطح کو عبور کرتا ہے تو خرید کا سگنل متحرک ہوتا ہے؛ جب اوپر سے نیچے جا کر -20 کی سطح کو عبور کرتا ہے تو فروخت کا سگنل متحرک ہوتا ہے۔

- خریدنے کے بعد، منافع روکنے اور نقصان روکنے کی سطحیں طے کی جاتی ہیں، اور تب تک پوزیشن بند نہیں کی جاتی جب تک کہ منافع/نقصان کی سطح نہ پہنچ جائے یا Williams %R مخالف سگنل نہ دے دے۔

- فروخت کرنے کے بعد، منافع روکنے اور نقصان روکنے کی سطحیں طے کی جاتی ہیں، اور تب تک پوزیشن بند نہیں کی جاتی جب تک کہ منافع/نقصان کی سطح نہ پہنچ جائے یا Williams %R مخالف سگنل نہ دے دے۔

- مخصوص وقت کی حد (جیسے 9:00-11:00) میں تجارت کرنے کا انتخاب کیا جا سکتا ہے نیز یہ بھی طے کیا جا سکتا ہے کہ آیا گھنٹے کے قریب (پہلے X منٹ سے بعد کے Y منٹ تک) تجارت کی جائے۔

- تجارتی سمت صرف خرید، صرف فروخت یا دونوں جانب تجارت کے طور پر منتخب کی جا سکتی ہے۔

فوائد کا تجزیہ

- متحرک منافع/نقصان روک: صارف کی سیٹنگ کے مطابق منافع اور نقصان روکنے کی سطحوں کو متحرک طور پر ایڈجسٹ کیا جاتا ہے، جس سے منافع کی حفاظت اور خطرے پر قابو بہتر ہوتا ہے۔

- لچکدار پیرامیٹرز: صارف اپنی ترجیحات کے مطابق مختلف پیرامیٹرز جیسے انڈیکیٹر پیریڈ، منافع/نقصان روکنے کی سطحیں، تجارتی اوقات وغیرہ طے کر سکتا ہے تاکہ مختلف مارکیٹ حالات سے نمٹا جا سکے۔

- ہموار انڈیکیٹر: EMA کے ذریعے Williams %R کی قدروں کو ہموار کرنے سے انڈیکیٹر میں شور کم ہوتا ہے اور سگنل کی اعتباریت بڑھتی ہے۔

- تجارتی وقت کی پابندی: مخصوص وقت کی حدود میں تجارت کرنے کا انتخاب کیا جا سکتا ہے، جس سے مارکیٹ کے زیادہ اتار چڑھاؤ والے اوقات سے بچا جا سکتا ہے اور خطرہ کم ہوتا ہے۔

- حسب ضرورت تجارتی سمت: مارکیٹ کے رجحان اور ذاتی فیصلے کی بنیاد پر صرف خرید، صرف فروخت یا دونوں جانب تجارت کا انتخاب کیا جا سکتا ہے۔

خطرات کا تجزیہ

- نامناسب پیرامیٹر سیٹنگ: اگر منافع/نقصان روکنے کی سطحیں بہت ڈھیلی یا بہت سخت رکھی جائیں تو منافع ضائع ہو سکتا ہے یا بار بار نقصان روک لگ سکتا ہے۔

- رجحان کی غلط شناخت: Williams %R انڈیکیٹر سائیڈ وے مارکیٹ میں کم کارگر ہوتا ہے اور غلط سگنل پیدا کر سکتا ہے۔

- وقت کی پابندی کا محدود اثر: تجارتی وقت کی پابندی کی وجہ سے حکمت عملی کچھ اچھے تجارتی مواقع سے محروم ہو سکتی ہے۔

- حد سے زیادہ بہتر بنانا: پیرامیٹرز کو حد سے زیادہ بہتر بنانے سے مستقبل میں حقیقی تجارت میں حکمت عملی کی کارکردگی خراب ہو سکتی ہے۔

بہتری کے رخ

- دیگر انڈیکیٹرز کے ساتھ انضمام: جیسے رجحان کے انڈیکیٹرز، اتار چڑھاؤ کے انڈیکیٹرز وغیرہ، تاکہ سگنل کی تصدیق کی درستگی بڑھے۔

- متحرک پیرامیٹر آپٹیمائزیشن: مارکیٹ کی صورتحال کے مطابق پیرامیٹرز کو حقیقی وقت میں ایڈجسٹ کرنا، جیسے رجحانی مارکیٹ اور سائیڈ وے مارکیٹ میں مختلف سیٹنگز استعمال کرنا۔

- منافع/نقصان روکنے کے طریقوں میں بہتری: جیسے ٹریلنگ اسٹاپ، جزوی منافع روک وغیرہ، تاکہ منافع کی بہتر حفاظت اور خطرے پر قابو پایا جا سکے۔

- سرمائے کے انتظام کا اضافہ: اکاؤنٹ بیلنس اور خطرے کی برداشت کی بنیاد پر ہر تجارت کے حجم کو متحرک طور پر ایڈجسٹ کرنا۔

خلاصہ

Williams %R متحرک منافع/نقصان روکنے کی حکمت عملی قیمت کی اوور باؤٹ اور اوور سیلڈ حالت کو سادہ اور مؤثر طریقے سے پکڑتی ہے، اور مختلف مارکیٹ حالات اور تجارتی انداز کے مطابق ڈھلنے کے لیے لچکدار پیرامیٹر سیٹنگز فراہم کرتی ہے۔ یہ حکمت عملی منافع/نقصان روکنے کی سطحوں کو متحرک طور پر ایڈجسٹ کرتی ہے، جس سے خطرے پر بہتر قابو اور منافع کی حفاظت ممکن ہوتی ہے۔ تاہم، عملی اطلاق میں پیرامیٹر سیٹنگ، سگنل کی تصدیق، تجارتی وقت کا انتخاب وغیرہ جیسے عوامل پر توجہ دینا ضروری ہے تاکہ حکمت عملی کی مضبوطی اور منافع بخشی کو مزید بہتر بنایا جا سکے۔

- 1