آر ایس آئی رجحان کی حکمت عملی

خلاصہ

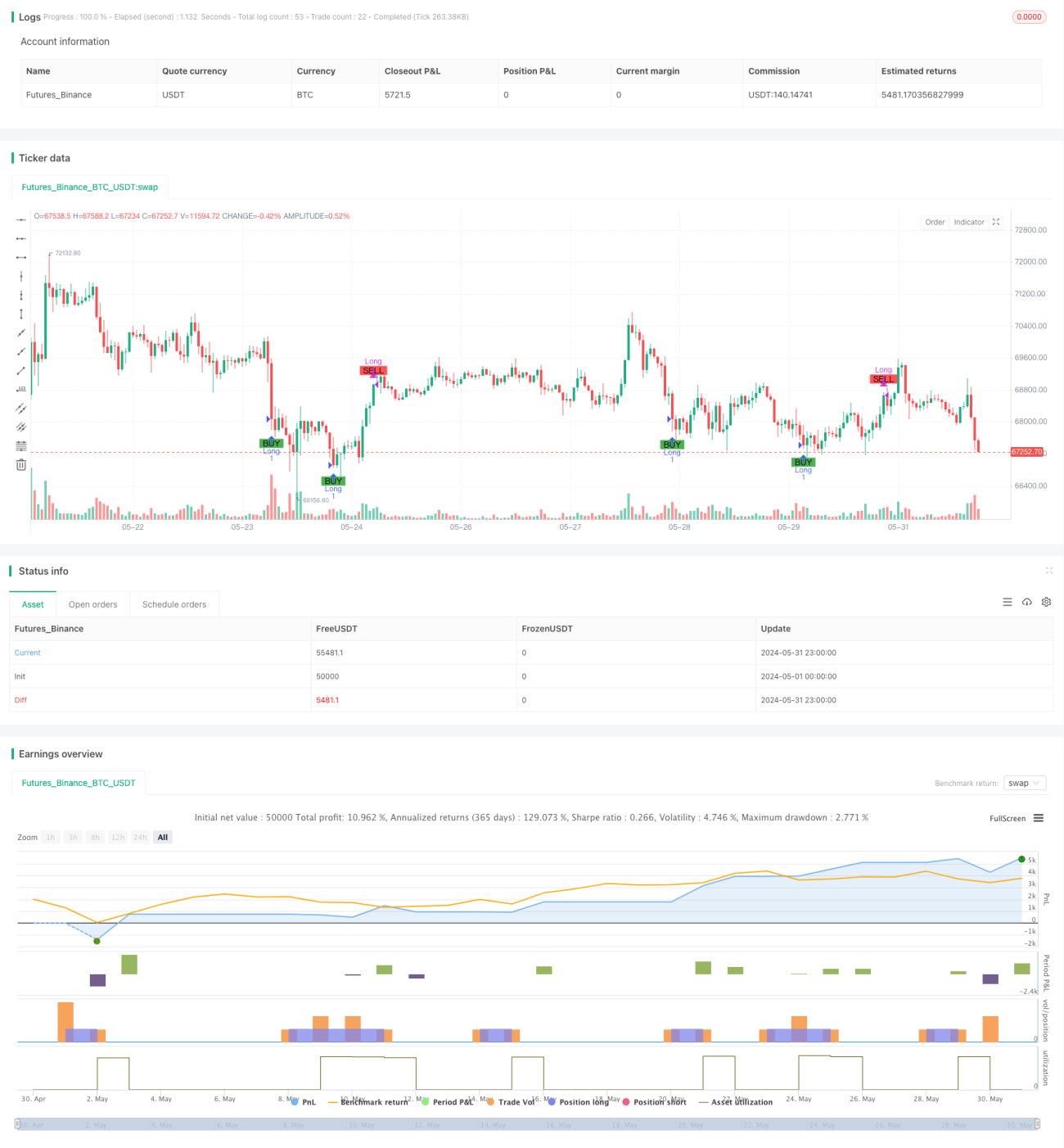

یہ حکمت عملی ریلٹیو سٹرینتھ انڈیکس (RSI) کی بنیاد پر کام کرتی ہے۔ اس میں RSI کی قدر کو پہلے سے طے شدہ بالائی اور زیریں حدود سے موازنہ کرکے خرید و فروخت کے سگنلز کا تعین کیا جاتا ہے۔ نیز، خطرے پر قابو پانے کے لیے سٹاپ لاس اور پوزیشن ہولڈنگ کی مدت کی پابندیاں بھی شامل ہیں۔

حکمت عملی کا اصول

- RSI کی قدر کا حساب لگایا جاتا ہے۔

- جب RSI کی قدر پہلے سے طے شدہ خرید کی حد سے کم ہوتی ہے تو خرید کا سگنل پیدا ہوتا ہے؛ جب RSI کی قدر پہلے سے طے شدہ فروخت کی حد سے زیادہ ہوتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

- خرید کے سگنل کی بنیاد پر موجودہ بند قیمت پر خرید کی مقدار کا حساب لگا کر خرید کا آرڈر دیا جاتا ہے۔

- اگر سٹاپ لاس کا تناسب مقرر کیا گیا ہو تو سٹاپ لاس کی قیمت کا حساب لگا کر سٹاپ لاس کا آرڈر دیا جاتا ہے۔

- فروخت کے سگنل یا سٹاپ لاس کی شرط پر تمام پوزیشنیں بند کر دی جاتی ہیں۔

- اگر زیادہ سے زیادہ ہولڈنگ مدت مقرر کی گئی ہو تو اس مدت سے زیادہ پوزیشن رکھنے پر، منافع یا نقصان سے قطع نظر، تمام پوزیشنیں بند کر دی جاتی ہیں۔

حکمت عملی کے فوائد

- RSI ایک وسیع پیمانے پر استعمال ہونے والا تکنیکی تجزیہ کا اشارہ (Indicator) ہے جو مارکیٹ کی زیادہ خریدی (Overbought) اور زیادہ فروخت (Oversold) کی حالتوں کو مؤثر طریقے سے پکڑ سکتا ہے۔

- اس حکمت عملی میں سٹاپ لاس اور پوزیشن ہولڈنگ کی مدت کی پابندیاں شامل ہیں جو خطرے پر قابو پانے میں مدد دیتی ہیں۔

- حکمت عملی کی منطق واضح ہے جسے سمجھنا اور عمل میں لانا آسان ہے۔

- RSI کے پیرامیٹرز اور حدود کو ایڈجسٹ کرکے مختلف مارکیٹ کے حالات کے مطابق ڈھالا جا سکتا ہے۔

حکمت عملی کے خطرات

- RSI بعض صورتوں میں غلط سگنل دے سکتا ہے جس کی وجہ سے حکمت عملی کو نقصان ہو سکتا ہے۔

- اس حکمت عملی میں تجارتی شے (Trading Instrument) کے بنیادی عوامل (Fundamentals) کو مدنظر نہیں رکھا گیا، صرف تکنیکی اشاروں پر انحصار کیا گیا ہے، جس کی وجہ سے مارکیٹ میں غیر متوقع واقعات کا سامنا ہو سکتا ہے۔

- مقررہ سٹاپ لاس کا تناسب مارکیٹ کے اتار چڑھاؤ (Volatility) کے مطابق ڈھل نہیں سکتا۔

- حکمت عملی کی کارکردگی پیرامیٹرز کی ترتیبات سے متاثر ہو سکتی ہے، نامناسب پیرامیٹرز حکمت عملی کی کارکردگی کو خراب کر سکتے ہیں۔

حکمت عملی کی بہتری کے ممکنہ پہلو

- دیگر تکنیکی اشارے، جیسے مووینگ ایوریج (Moving Average)، شامل کرکے حکمت عملی کی وشوسنییتا (Reliability) میں اضافہ کیا جا سکتا ہے۔

- سٹاپ لاس کی حکمت عملی کو بہتر بنایا جا سکتا ہے، جیسے چلتا ہوا سٹاپ لاس (Trailing Stop) یا اتار چڑھاؤ پر مبنی متحرک سٹاپ لاس (Volatility-based Dynamic Stop) کا استعمال۔

- مارکیٹ کے حالات کے مطابق RSI کے پیرامیٹرز اور حدود کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

- تجارتی شے کے بنیادی عوامل کے تجزیے کو شامل کرکے حکمت عملی کی خطرے پر قابو پانے کی صلاحیت کو بہتر بنایا جا سکتا ہے۔

- حکمت عملی کی بیک ٹیسٹنگ (Backtesting) اور پیرامیٹر آپٹیمائزیشن کرکے بہترین پیرامیٹرز کا مجموعہ تلاش کیا جا سکتا ہے۔

اختتامیہ

یہ حکمت عملی RSI اشارے کا استعمال کرکے مارکیٹ کی زیادہ خریدی اور زیادہ فروخت کی حالتوں کو پکڑتی ہے، اور خطرے پر قابو پانے کے لیے سٹاپ لاس اور پوزیشن ہولڈنگ کی مدت کی پابندیاں بھی شامل کرتی ہے۔ حکمت عملی کی منطق سادہ اور واضح ہے، جسے نافذ کرنا اور بہتر بنانا آسان ہے۔ تاہم، حکمت عملی کی کارکردگی مارکیٹ کے اتار چڑھاؤ اور پیرامیٹرز کی ترتیبات سے متاثر ہو سکتی ہے، لہذا اس کی مضبوطی اور منافع بخشی کو بڑھانے کے لیے دیگر تجزیاتی طریقوں اور رسک مینجمنٹ کے ذرائع کو شامل کرنے کی ضرورت ہے۔

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Simple RSI Strategy", overlay=true, initial_capital=20, commission_value=0.1, commission_type=strategy.commission.percent)

// Define the hardcoded date (Year, Month, Day, Hour, Minute)- 1